Can MicroStrategy keep funding its Bitcoin strategy if its own capital machine is starting to break down?

What’s Driving MicroStrategy Funding Pressure?

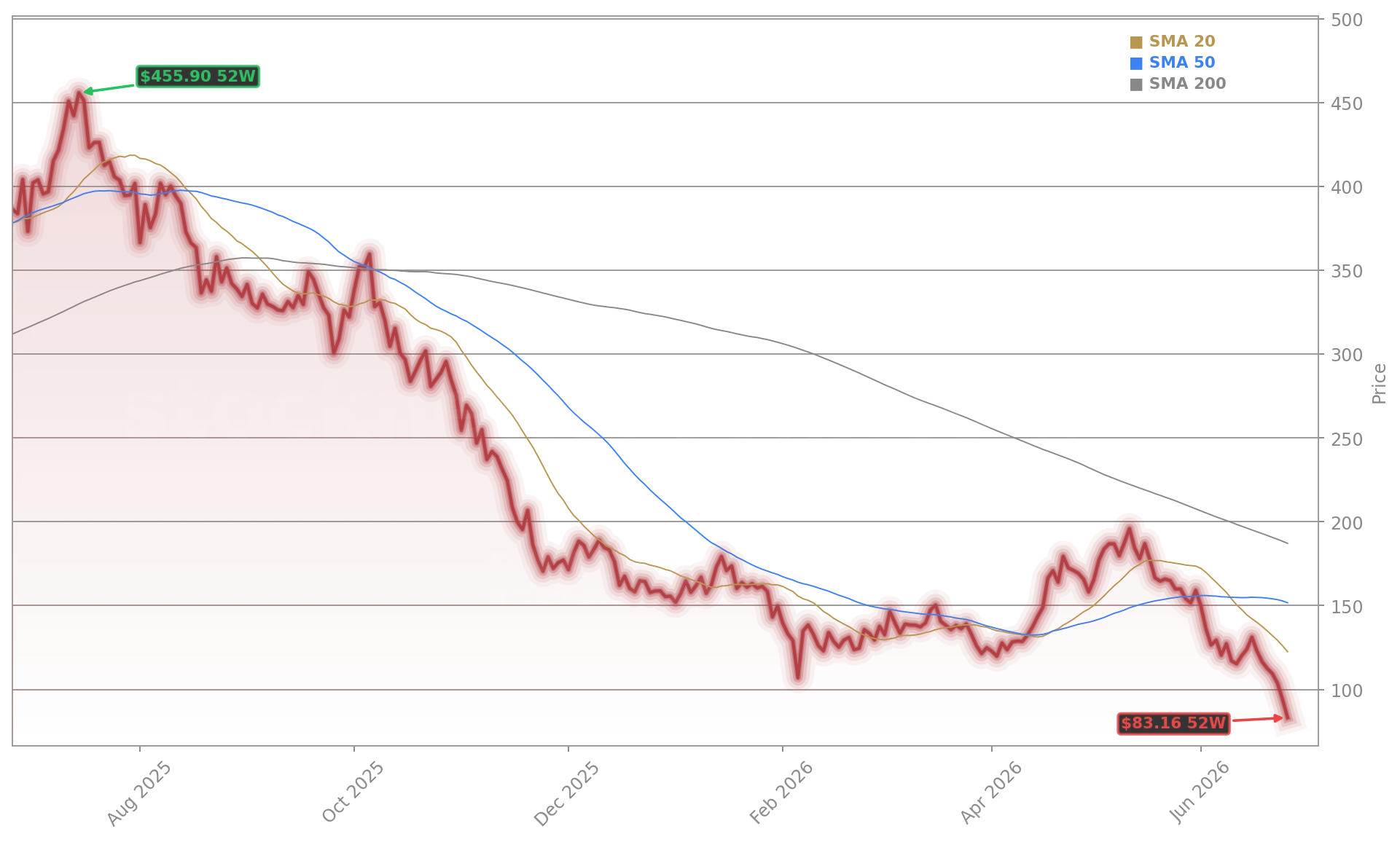

MicroStrategy Incorporated’s funding model — built on selling equity, preferred shares, and debt to buy Bitcoin — is breaking down. The company holds 847,363 BTC acquired at an average $75,651, now worth roughly $52 billion at $61,500 — a $12.6 billion paper loss. That loss erodes the premium MSTR once commanded over its Bitcoin net asset value, making common stock sales increasingly dilutive. With MSTR trading at $82.64 — down nearly 50% month-to-date and 83% from its all-time high — the equity funding channel is near-critical. Meanwhile, STRC, the variable-rate perpetual preferred stock designed to trade at $100, has collapsed to $76.62, a record low that cripples MicroStrategy’s primary capital-raising vehicle. This isn’t theoretical: STRC’s $10.5 billion outstanding carries an annual dividend cost of $1.2 billion — now consuming just 14 months of cash reserves, down from over 7 years at the start of 2026.

How Is STRC’s Collapse Impacting Wall Street?

STRC’s discount isn’t just a MicroStrategy problem — it’s a market signal. Traders are pricing in rising default risk, with options volume spiking 167% above average and a put-call ratio of 1.35 indicating strong defensive positioning. The $95–$100 strike zone remains the focal point for recovery bets, but sustained weakness threatens broader confidence in crypto-treasury vehicles. Unlike traditional financials, MicroStrategy Incorporated has no earnings diversification — its valuation is entirely tied to Bitcoin’s path and its ability to finance that exposure. That makes it a volatility amplifier for the NASDAQ, especially amid broader tech selloffs triggered by AI hardware cost concerns — a dynamic that recently pulled NVIDIA and Apple lower. Analysts at RBC Capital Markets have downgraded STRC-linked instruments to ‘Underperform’, citing ‘unsustainable cash burn relative to reserve coverage.’

Can MicroStrategy Incorporated Rebuild Liquidity?

Yes — but at steep cost. MicroStrategy Incorporated recently raised $300 million in cash, boosting reserves to $1.4 billion. But that’s only enough to cover STRC dividends for 14 months — far short of the 24-month buffer analysts at Citigroup say is required for stability. The firm could hike STRC’s 11.5% dividend to attract buyers, but that would increase annual cash outflow by hundreds of millions. Alternatively, it could issue new common shares — a path already underway, diluting existing holders. A recent $101 million Bitcoin purchase was funded partly by equity sales, confirming the model’s pivot from ‘buy and hold’ to ‘sell and buy.’ That shift undermines Michael Saylor’s long-standing narrative and raises red flags for U.S. institutional investors increasingly scrutinizing governance and capital discipline.

Is Legal Risk Amplifying MicroStrategy Funding Pressure?

Yes. Rosen Law Firm is investigating potential securities law violations related to disclosures around STRC guarantees and convertible debt terms. The probe follows a sharp drop in MSTR’s market net asset value (MNAV) — from 3.0 to 0.54 — signaling a collapse in investor confidence in the company’s stated $100 per-share backing. With insiders like Jarrod M. Patten and Phong Le selling Class A shares across March–May 2026, the disconnect between leadership actions and public messaging is widening. This isn’t isolated: Peter Schiff has publicly criticized the STRC structure as ‘predatory’ to common shareholders. For U.S. portfolios, this adds regulatory and litigation risk — a factor absent in pure-play crypto ETFs like BlackRock’s IBIT, which now holds more Bitcoin than MicroStrategy Incorporated.

What’s Next for MicroStrategy Incorporated and Bitcoin?

Short term, MicroStrategy Funding Pressure will persist unless Bitcoin rallies decisively above $70,000 — a level needed to restore MSTR’s premium and lift STRC toward $90. Longer term, the company must pivot from opportunistic accumulation to systematic capital allocation — a shift analysts at Morgan Stanley describe as ‘non-negotiable for S&P 500 eligibility.’ With institutions like Vanguard and BlackRock now holding over $1.3 billion in MSTR shares, the stakes for U.S. index inclusion are high. But until cash reserves double and STRC stabilizes, MicroStrategy Incorporated remains a high-beta, high-risk proxy — not a ‘digital gold’ hedge.

Our objective is to maximize Bitcoin per share over the next seven years.— Michael Saylor, Executive Chairman, MicroStrategy Incorporated

Related Coverage: MicroStrategy Liquidity Warning: $1.2B Strain on MSTR explores how STRC’s dividend burden now dominates near-term price action. Bitcoin Plunge Warning: Is BTC Setting Up Its Next Big Move? analyzes whether current weakness signals a deeper capitulation or a stealth accumulation phase.