Can MicroStrategy keep funding its Bitcoin buying spree without turning its new $1.4 billion reserve into a market stress test?

What Does the $1.4 Billion USD Reserve Mean for MSTR?

MicroStrategy Incorporated announced a $1.4 billion USD Reserve as of June 21, 2026 — a management-designated liquidity buffer aimed squarely at supporting dividend payments on its STRC and other preferred securities. This reserve, built from unsettled ATM proceeds and existing cash, directly addresses investor concerns raised after STRC slipped below $89 and its dividend rate climbed to 11.5%. Unlike collateralized instruments, STRC carries only a residual claim on assets, making the USD Reserve a critical signal of credit discipline. For Wall Street, this isn’t just balance sheet hygiene — it’s a stress-tested liquidity mechanism that could stabilize MSTR’s equity volatility relative to Bitcoin, a key differentiator versus pure-play crypto ETFs like IBIT or GBTC.

How Is the MicroStrategy Bitcoin Purchase Engine Still Running?

Despite STRC trading 11% below its $100 target and MSTR shares down 42% from May highs, the MicroStrategy Bitcoin Purchase machine remains operational — fueled by $335.5 million in Class A common stock sold via ATM between June 15–21. The $34.9 million purchase of 520 BTC — at an average price of $67,068 — marks the company’s 174,345th BTC acquisition in 2026 alone. That pace implies a $24 billion annualized Bitcoin acquisition run rate, more than double global miner output. This aggressive capital deployment contrasts sharply with the broader S&P 500’s 2026 capital return focus and positions MSTR as a unique, high-beta proxy for institutional Bitcoin demand — especially as BlackRock and Vanguard collectively added $1.344 billion in MSTR shares this spring, per TradingView.

Why Is STRC Under Pressure — And What Does It Mean for MSTR?

STRC’s record low of $88.20 reflects not just Bitcoin’s near-$64,000 pullback, but a structural mismatch: the instrument’s dividend resets monthly to defend $100, yet its uncollateralized nature leaves it exposed to credit sentiment and Fed policy. With the Federal Reserve signaling rate hikes and two-year Treasury yields surging, STRC’s effective yield now exceeds 13% — a red flag for risk-averse income investors. Critics, including Peter Schiff, have labeled STRC a ‘Ponzi’; supporters like Michaël van de Poppe argue a Bitcoin crash below $10,000 would be required to break the cycle. For MSTR common shareholders, the stakes are clear: if Bitcoin appreciates less than 10% annually, the equity may underperform the S&P 500 — but if it hits 20%, MSTR’s 70-volatility ‘rocket ship’ profile, per Saylor, could deliver outsized returns relative to Apple or NVIDIA.

How Does MSTR Compare to Broader Market Risks?

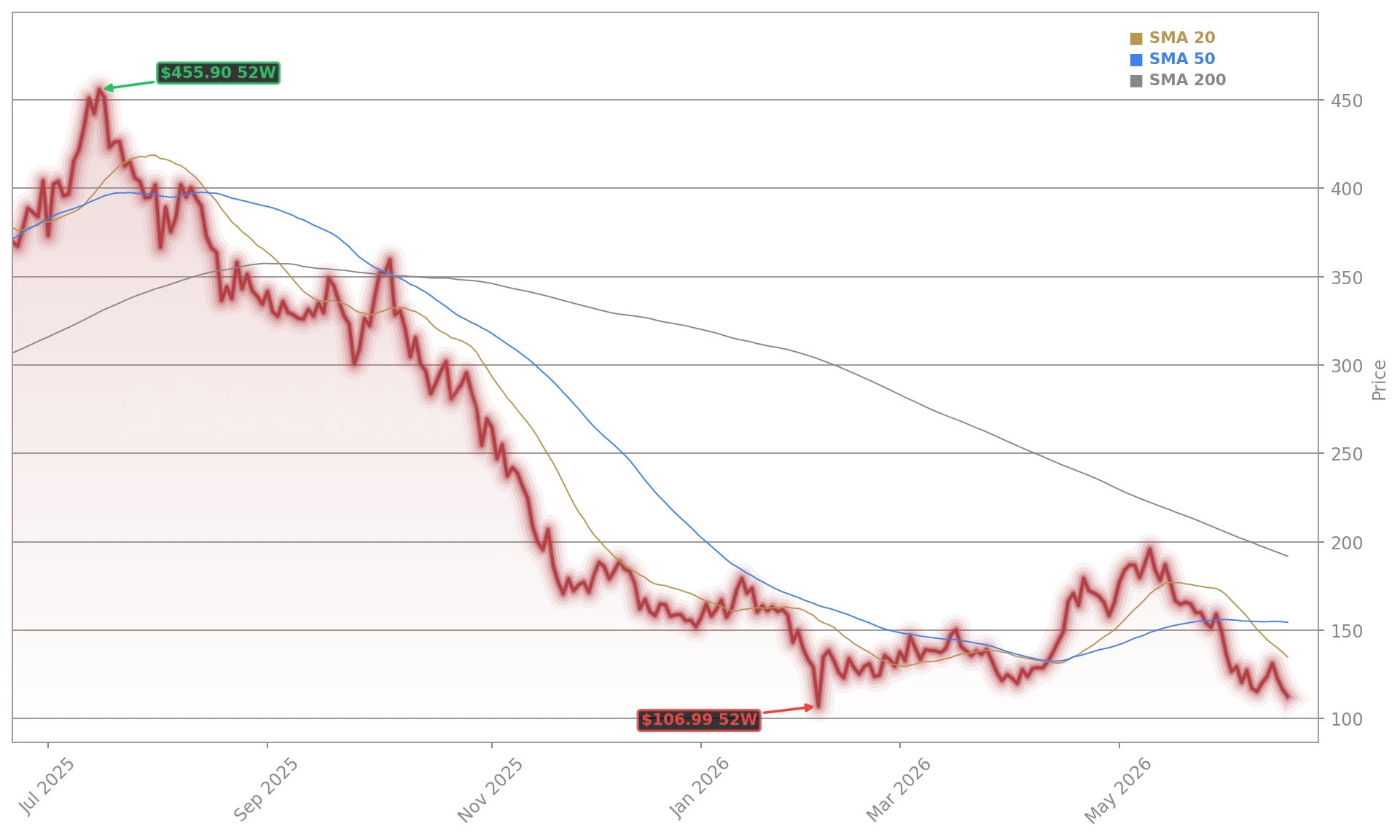

At $117.23, MSTR trades 43% below its 200-day moving average — a bearish technical signal shared by few NASDAQ giants outside of high-flying AI plays. Yet unlike cyclical tech stocks, MSTR’s valuation hinges on Bitcoin’s mNAV (multiple of net asset value), now at 1.0 — meaning its market cap roughly equals its Bitcoin + cash value. That’s a stark contrast to Tesla, which trades at 65x forward earnings, or Meta, which commands a 25x P/E on ad-driven cash flow. Morgan Stanley analysts recently noted that MSTR’s beta to Bitcoin has spiked to 1.8 in Q2 2026, up from 1.3 in Q4 2025 — reinforcing its role as Wall Street’s most leveraged, liquid Bitcoin exposure. With Bitcoin forming a bearish flag pattern and testing $59,000 support, MSTR’s near-$104 technical floor could trigger algorithmic buying — or accelerate outflows if the $60,000 BTC threshold breaks.

What’s Next for the MicroStrategy Bitcoin Purchase Strategy?

When I gave this speech in October 2022, Bitcoin traded near $20,000… Today, our BTC and USD reserves exceed debt by ~$48 billion.— Michael Saylor, Executive Chairman, MicroStrategy Incorporated

MicroStrategy Bitcoin Purchase activity shows no signs of slowing: the company holds 847,363 BTC — 4% of all Bitcoin ever mined — and has raised over $60 billion since 2022. Its $21 billion expanded ATM capacity, disclosed March 23, ensures continued funding flexibility. With STRC’s next dividend reset due June 30 and Bitcoin’s Polymarket odds of hitting $55,000 at 73%, the next 30 days will test whether Saylor’s model remains resilient — or whether rising debt service costs force a strategic pivot. For U.S. investors, MSTR remains a binary bet: a hedge against fiat devaluation or a volatility amplifier in a hawkish Fed regime.