Can MicroStrategy keep turning share issuance into Bitcoin upside without pushing dilution fears too far for common shareholders?

What Does the Latest MicroStrategy Bitcoin Purchase Mean for MSTR Equity?

Strategy’s most recent $100 million Bitcoin acquisition — executed between June 8 and June 14 at an average price of $63,024 per coin — brings its total holdings to 846,842 BTC, valued at roughly $56.1 billion at current market rates. The purchase lowered the company’s average cost basis slightly to $75,656 per BTC, reflecting disciplined buying below its long-term average. Crucially, the transaction was funded by selling 1.73 million Class A shares for $209 million — $100 million allocated to Bitcoin, $100 million to cash reserves (now at $1.1 billion), and the balance to expenses. This capital recycling underscores Strategy’s hybrid treasury model: not just holding Bitcoin, but actively managing liquidity, leverage, and senior claims to amplify common equity exposure.

Is MSTR Still Accretive for Common Shareholders?

Critics point to falling BTC Yield — a proprietary metric tracking Bitcoin per diluted share — which dropped from 13.0% on June 1 to 12.5% post-purchase. That decline, despite growing holdings, signals dilution. Analysts at 24/7 Wall St. maintain a $391.97 price target (216% upside), but flag $8.17 billion in long-term debt and $229.53 million in quarterly preferred dividends as structural headwinds. Meanwhile, Strategy’s executive chairman Michael Saylor defends the model using Common Equity Bitcoin Exposure (CEBE), arguing that cash reserves and senior claims must be weighed alongside raw BTC count. The gap between BTC-per-share and CEBE-per-share — which Saylor calls ‘amplification’ — is widening as STRC preferred stock ($5.6 billion raised YTD) and STRK programs scale.

How Are Institutions Positioning on Strategy?

Vanguard and BlackRock added a combined $1.344 billion to their MSTR positions in May, per TradingView. This institutional momentum coincides with growing STRC adoption: the Bitcoin-secured preferred stock now trades at $94.80, down 1% week-over-week but still anchored by 5x over-collateralization. STRC’s 11.5% dividend yield — structured as tax-advantaged capital return — offers low-volatility exposure (volatility ~3 vs. Bitcoin’s ~40), attracting fixed-income investors. Yet, STRC has traded below par for four straight weeks, signaling softness in the preferred market. The S&P 500 inclusion conversation remains alive, with traders assigning a 58% Polymarket probability — a catalyst that could materially compress MSTR’s valuation discount relative to its Bitcoin holdings.

What’s Next for Strategy’s Capital Structure?

Adoption of Bitcoin continues to grow in 2026. Digital Credit, highlighted by STRC, has been a big success.— Phong Le, CEO of Strategy

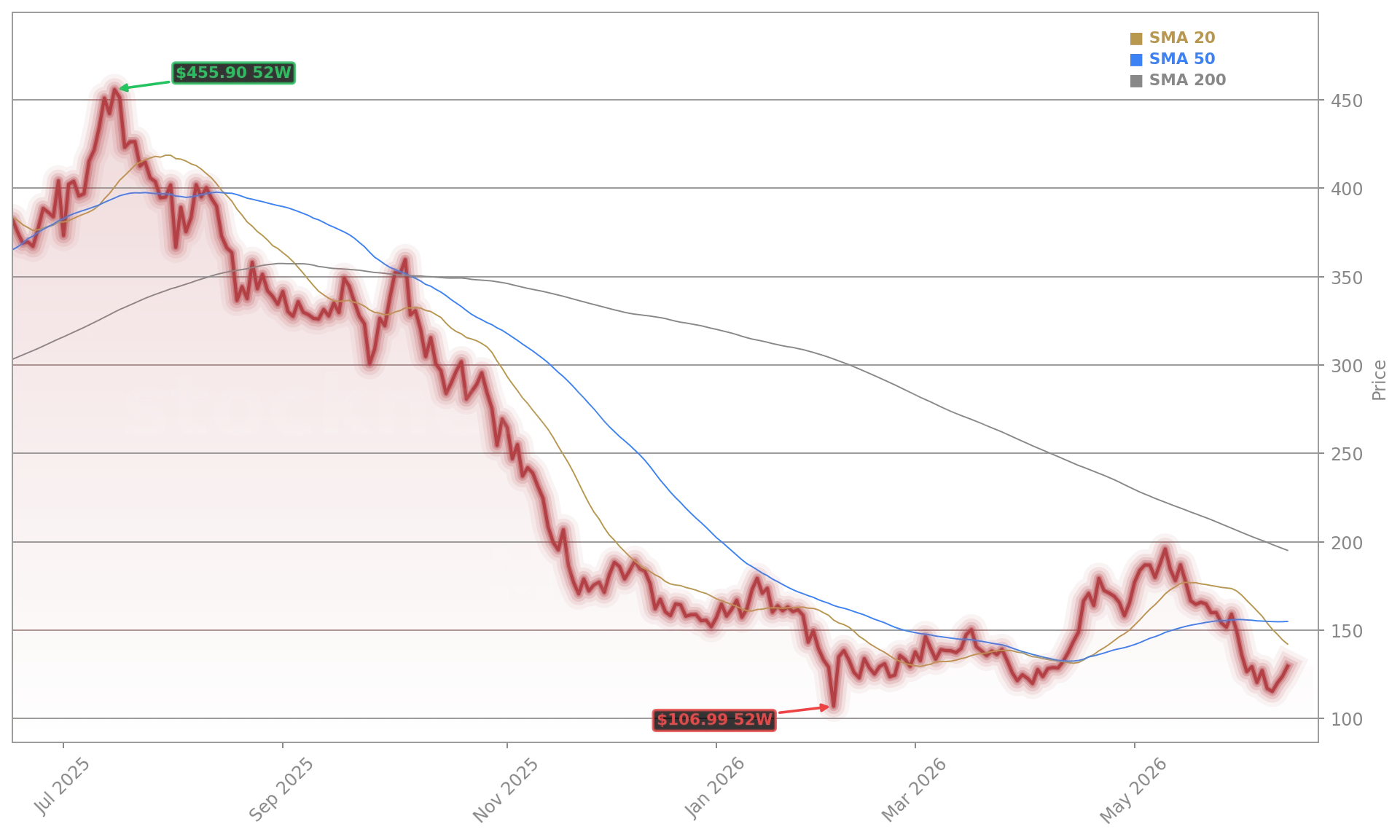

Strategy still has $25.75 billion of Class A shares available under its at-the-market program and has authorized up to $21 billion more in common stock, $21 billion in STRC, and $2.1 billion in STRK. That firepower supports continued Bitcoin buying — but also raises dilution risk. CEO Phong Le and CFO Andrew Kang collectively sold over 146,000 shares in early June, mostly tied to vesting events, while director Jarrod M. Patten registered another 1,500 shares for sale on June 15. With MSTR’s 200-day moving average at $196.21 — still 31.9% above current price — technical resistance remains steep. Yet a recent Power Inflow signal at $131.47 triggered a 3.1% intraday rally, suggesting institutional buyers are stepping in at key support levels near $118.50.