Can MicroStrategy STRC still function as a stable funding tool, or is it becoming the biggest threat to MSTR’s Bitcoin play?

What’s breaking the STRC peg?

MicroStrategy STRC — the variable-rate preferred stock designed to stay anchored at $100 — has collapsed to $86.20, its lowest level ever. Unlike traditional preferreds, STRC’s dividend resets semi-monthly based on short-term Treasury yields and Bitcoin’s market value, making it a hybrid instrument tethered to both monetary policy and crypto volatility. As the Federal Reserve signaled a hawkish pivot — with nine FOMC members now forecasting a 2026 rate hike — two-year Treasury yields surged, widening STRC’s yield spread and triggering forced selling. Kraken’s chief economist estimates 86% of STRC’s price swings now track Bitcoin directly, undermining its stated stability. This erosion transforms STRC from a funding tool into a risk amplifier — especially as Bitcoin itself dipped below $63,000 amid broad risk-asset repricing.

How is MicroStrategy STRC impacting MSTR’s technical outlook?

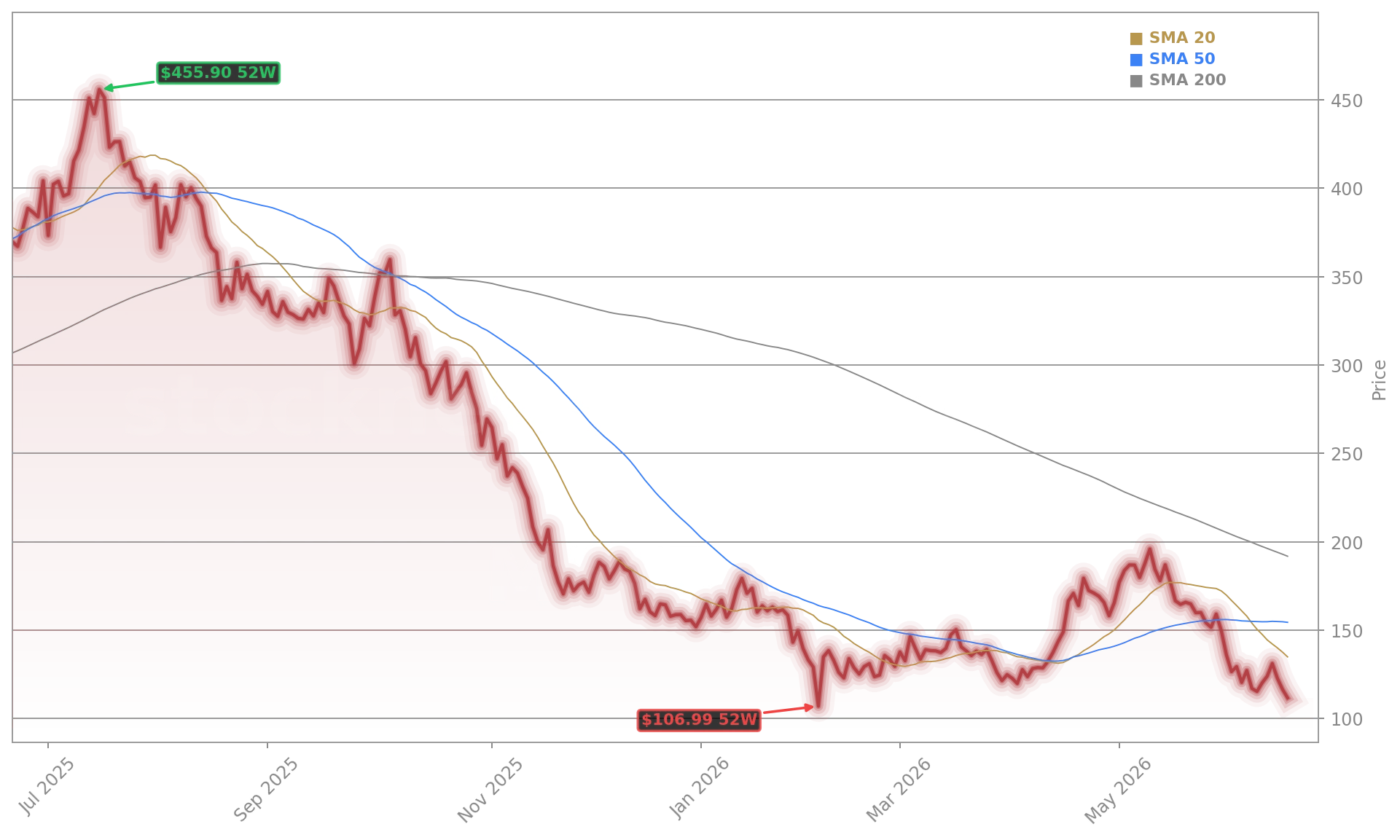

MSTR is now trading 43.3% below its 200-day moving average at $192.98 and 29.3% below its 50-day average — confirming a persistent bearish trend structure. The death cross, formed in October 2025, remains intact. Momentum indicators are flashing red: MACD is below its signal line, and the Benzinga Edge Scorecard rates MSTR’s momentum at just 3.2 out of 10. With key support at $104.00 — just above the 52-week low — any break below that level could trigger algorithmic selling and margin calls. The stock’s 70.35% one-year decline places it among the worst performers in the NASDAQ Composite, dragging down sector-weighted ETFs that hold MicroStrategy Incorporated as a thematic crypto proxy.

Is the Bitcoin treasury model still sustainable?

Arca’s Chief Investment Officer Jeff Dorman sees three scenarios — and only one is bullish. With 70% probability, he expects MicroStrategy Incorporated to continue its current path: selling small tranches of MSTR equity monthly to fund Bitcoin purchases, further diluting common shareholders and pressuring the stock toward 0.70x mNAV. A 25% chance exists that Michael Saylor sells $3–4 billion in Bitcoin to retire STRC debt — a move that would stabilize STRC but briefly suppress BTC prices. The remaining 5% reflects a forced dividend suspension, which Peter Schiff has labeled the ‘most obvious Ponzi ever built.’ Notably, STRC’s design involved AI assistance — a detail Saylor confirmed — highlighting how experimental this capital structure truly is.

How do competitors compare on Wall Street?

While MicroStrategy Incorporated wrestles with STRC’s instability, rival crypto-treasury vehicles are gaining traction. Strive’s SATA preferred shares — offering daily dividends, no debt, and no Bitcoin correlation — saw volume jump 215% to $53 million as STRC sold off. Meanwhile, institutional demand for pure-play crypto exposure remains strong: NVIDIA and Tesla continue drawing investor capital, with both up over 12% year-to-date versus MSTR’s 68% decline. Even Apple’s recent $5 billion crypto infrastructure investment signals a more diversified, less leveraged approach to digital asset integration — contrasting sharply with MicroStrategy Incorporated’s all-in Bitcoin bet.

What do analysts say about MicroStrategy STRC’s role?

We have a break even level. We calculate it’s about 2.6 percent. We have such a mountain of equity, $60 billion of equity capital, that Bitcoin only needs to go up 2.5 percent for us to pay those dividends forever.— Michael Saylor, Executive Chairman of MicroStrategy Incorporated

Citigroup analysts recently downgraded their outlook on MicroStrategy Incorporated, citing ‘increasing fragility in the STRC financing loop’ and lowering their 12-month price target to $125 from $150. RBC Capital Markets maintains a ‘Sector Perform’ rating but warns that STRC’s yield spread volatility ‘exposes MSTR to asymmetric downside risk during Fed tightening cycles.’ Goldman Sachs notes that ‘if STRC remains below $90 for three consecutive months, the math shifts decisively toward BTC liquidation — a scenario that would materially reset institutional confidence in crypto-treasury models.’