Is MicroStrategy’s growing cash pile a smart defense move, or an early warning that its Bitcoin machine is under real stress?

Why did Strategy prioritize cash over Bitcoin?

Strategy sold 2.7 million shares of its Class A common stock via its at-the-market (ATM) program last week, raising $335.5 million. Of that, only $34.9 million funded the acquisition of 520 BTC at an average price of $67,068 — the smallest weekly purchase in months. The remaining $300 million was allocated to its USD Reserve, lifting the total to $1.4 billion. This marks a clear departure from its historic ‘buy-first’ playbook and reflects mounting pressure on STRC, which fell to a record intraday low of $82.53 — a 17% discount to its $100 par value. As Benchmark analyst Mark Palmer noted, STRC’s decline ‘created a major headache’ for Strategy’s primary Bitcoin-funding engine, forcing a temporary pause in preferred-stock issuance and a pivot to equity-based balance sheet defense.

How does the MicroStrategy Bitcoin Reserve compare to peers?

With 847,363 BTC valued at $54.8 billion, Strategy remains the largest corporate holder — far outpacing the iShares Bitcoin Trust (NASDAQ:IBIT), which holds $48.1 billion in BTC. Its MicroStrategy Bitcoin Reserve now represents roughly 4% of all Bitcoin ever to be mined. Competitors like Strive have gained traction, acquiring 750 BTC last week — more than Strategy’s own purchase — and pushing its SATA preferred stock back toward $98. Meanwhile, Marathon Digital (MARA) continues to underperform, posting a $1.3 billion Q1 2026 net loss as mining margins collapsed. Strategy’s model remains uniquely leveraged: its $60 billion equity base means Bitcoin needs only 2.6% annual appreciation to cover STRC’s $1.7 billion annual dividend obligations — a far lower hurdle than the 10%+ needed for meaningful common equity upside.

Is STRC’s $100 ‘peg’ still credible?

STRC’s slide below $90 triggered alarm across retail and institutional channels. Bloomberg senior ETF analyst Eric Balchunas called the instrument ‘an ongoing thorn,’ while Barron’s Andrew Bary highlighted that 80% of STRC is held by retail investors — making it unusually sensitive to sentiment shifts. Strategy’s response — raising cash and having CEO Le Phong personally buy $1 million of STRC at $90.80 — underscores management’s commitment to restoring confidence. Still, the security’s effective yield now exceeds 13%, pricing in junk-rated risk. As Palmer clarified, STRC has ‘no obligation’ to trade at $100 — only an objective to ‘support’ it. That distinction matters: unlike stablecoins, STRC is a credit instrument, not a collateralized asset. Its resilience now hinges on Bitcoin’s ability to stabilize above $60,000 and on Strategy’s capacity to rebuild investor trust without further dilution.

What does this mean for MSTR shareholders and the S&P 500?

When I gave this speech in October 2022, Bitcoin traded near $20,000… Today, our BTC and USD reserves exceed debt by ~$48 billion.— Michael Saylor, Executive Chairman of Strategy

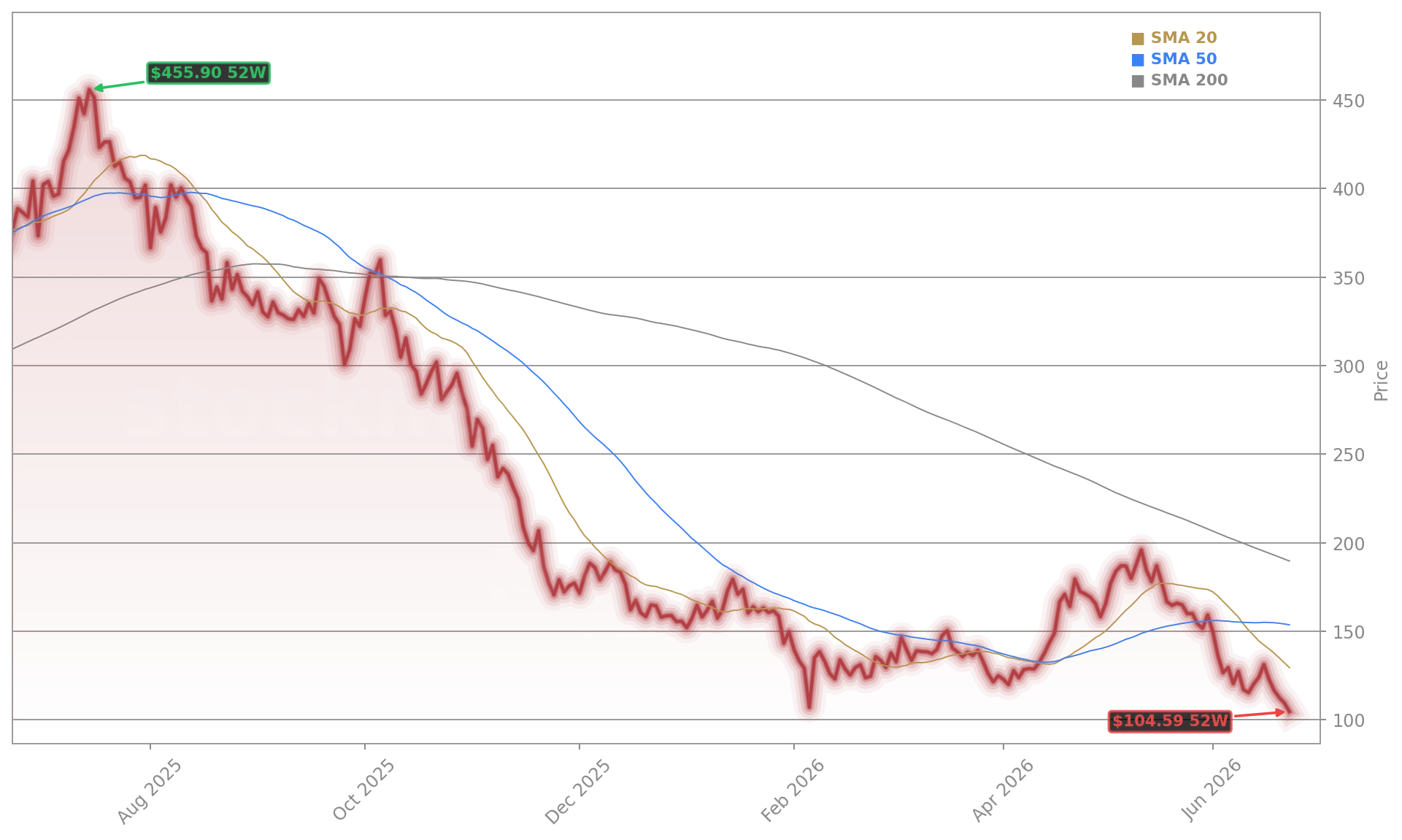

MicroStrategy Incorporated stock has plunged 72% from its 52-week high and is now trading at $104.88 — down 5% today and nearing its lowest close since May 2024. The dilution from last week’s ATM sale lifted the diluted share count to 388.6 million, reducing BTC-per-share growth to 11.8% year-to-date. For U.S. portfolios, MSTR’s 70-volatility profile makes it a high-beta satellite holding — more correlated with Bitcoin than the broader NASDAQ. RBC Capital Markets recently downgraded the stock to ‘Underperform,’ citing ‘increasing capital structure fragility.’ Yet long-term bulls point to Strategy’s $48 billion BTC-and-cash buffer over debt — a dramatic reversal from the $300 million deficit it faced in late 2022. That endurance remains its strongest argument in a market increasingly skeptical of leveraged crypto exposure.