Is the Rocket Lab Upgrade a real long-term turning point, or is RKLB still racing ahead of execution?

What Does the Rocket Lab Upgrade Mean for NASDAQ?

Rocket Lab USA, Inc. is emerging as a structural beneficiary of the U.S. government’s push to onshore space infrastructure — a trend that’s reshaping aerospace allocations across the NASDAQ. Unlike NVIDIA or Apple, which dominate AI and consumer tech, RKLB offers pure-play exposure to the $220 billion defense space budget and commercial satellite launch acceleration. With $1.4 billion in cash and a $2.1 billion backlog (70% tied to U.S. government contracts), the company’s balance sheet is among the strongest in the sector — especially compared to peers like Redwire (RDW) and AST SpaceMobile (ASTS), both of which trade at negative EV/EBITDA. Stifel recently raised its price target to $132 and maintained a Buy rating, citing Rocket Lab’s record launch cadence and Photon platform adoption by NASA and the Space Development Agency. The Rocket Lab Upgrade isn’t just about valuation — it’s about recalibrating RKLB’s role from launch provider to national security infrastructure partner.

How Does Rocket Lab Compare to SpaceX?

Rocket Lab USA, Inc. isn’t competing head-to-head with SpaceX — it’s filling a deliberate niche. While SpaceX dominates heavy-lift and Starlink, Rocket Lab owns the dedicated small-sat launch market with its Electron rocket and is expanding into medium-lift with Neutron, now targeting its first orbital test in Q4 2026. Its Space Systems division — manufacturing solar panels, avionics, and on-orbit software — generates 70% of revenue, insulating it from launch-cycle volatility. This contrasts sharply with SpaceX’s AI- and Starlink-driven valuation model. Analysts at RBC Capital Markets note that RKLB’s defense integration via Geost acquisition has accelerated Golden Dome program timelines, boosting near-term visibility. Meanwhile, shares of Tesla and other Musk-linked equities saw muted retail flows last week — yet RKLB ranked among Vanda’s top 10 most-bought stocks, signaling divergent investor sentiment.

Is Profitability Finally Within Reach?

Yes — and Wall Street is pricing it in. Rocket Lab USA, Inc. is expected to deliver its first GAAP profit in 2025: $0.01 per share, per consensus estimates, marking a critical inflection point after years of heavy R&D. Revenue is projected to nearly double to $1.3 billion — up from $680 million in 2024 — driven by increased Neutron tooling orders and Photon satellite deployments for U.S. Air Force and NRO missions. KGI Securities initiated coverage on June 11 with a Neutral rating and $105 price target, acknowledging execution risk but affirming the company’s “uniquely defensible position in responsive space access.” The Rocket Lab Upgrade from KeyBank reinforces that view, especially as RKLB’s free cash flow turns positive in Q3 — a milestone analysts say could trigger renewed institutional buying ahead of NASDAQ-100 rebalancing in July.

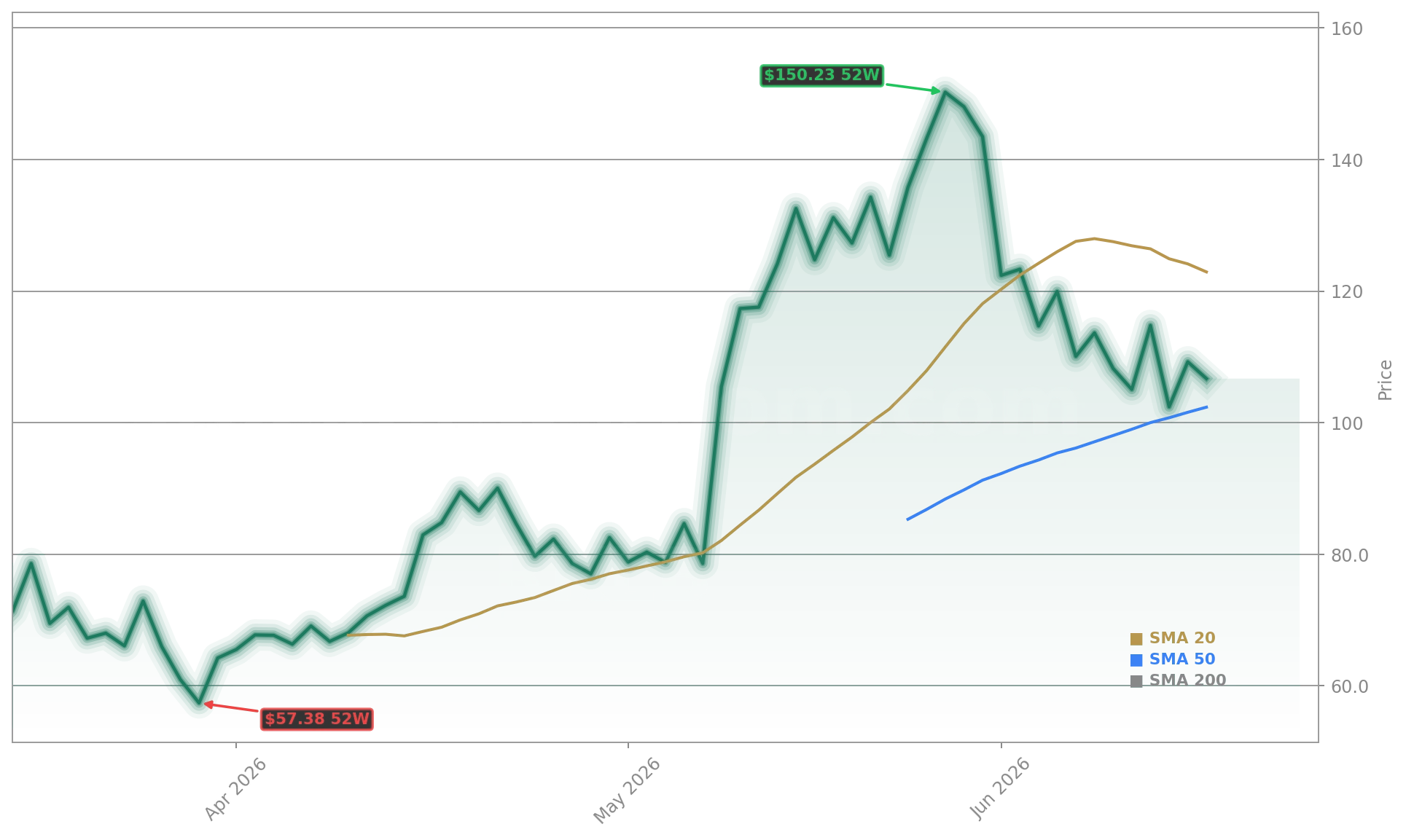

What’s Next for the Stock?

With support holding near $100 and resistance at $115, the path to $135 hinges on two catalysts: Neutron’s successful orbital flight and a formal contract award for the Space Development Agency’s Tranche 3 transport layer. Rocket Lab USA, Inc. has already secured $412 million in firm orders for Neutron — more than double its nearest small-launch peer. And unlike many growth names facing tighter credit conditions, RKLB’s $1.4 billion cash pile insulates it from financing risk. Citigroup analysts recently highlighted RKLB’s “best-in-class vertical integration” as a key differentiator versus legacy defense contractors. The Rocket Lab Upgrade is more than a rating change — it’s a signal that aerospace is no longer just about defense primes. It’s about speed, scalability, and sovereign launch capacity — all core RKLB strengths.

Rocket Lab’s execution on Photon and Neutron has been exceptional — this is the inflection point where scale meets profitability.— Erik Rasmussen, Stifel

Related Coverage: The Rocket Lab Upgrade +6.7% as Nasdaq-100 Entry Lifts Shares explores how RKLB’s recent inclusion in the Nasdaq-100 index is reshaping ETF flows and institutional positioning. Meanwhile, SpaceX Acquisition Jumps 19.6% on $60B Cursor Deal provides critical context on how AI-driven space infrastructure deals are redefining competitive boundaries — and why Rocket Lab USA, Inc. remains the only pure-play launch-and-systems platform positioned across both commercial and national security orbits.