Can SanDisk’s AI-fueled NAND rally keep running, or is this storage boom already pricing in perfection?

Is SanDisk Storage Boom Sustainable?

The SanDisk Storage Boom is rooted in AI’s insatiable appetite for high-bandwidth, low-latency storage. Unlike traditional data centers, AI training clusters require petabytes of NAND flash for model weights, inference caching, and real-time data ingestion. SanDisk (Western Digital), now fully independent, has leveraged its joint venture with Kioxia to scale NAND production faster than rivals Samsung and SK Hynix — while securing five multiyear supply agreements with top-tier cloud providers last quarter. CEO David Goeckeler called these deals ‘a fundamental evolution of our business,’ citing ‘enhanced visibility and long-term value creation.’ NAND prices have tripled in the past year, and SanDisk’s gross margin hit 78% in Q3 — validating the AI-storage thesis. Still, supply constraints are temporary: new fabs take 18–24 months to ramp, meaning the current tightness may persist through 2027 but likely eases by 2028.

How Does SanDisk Compare to Micron and Western Digital?

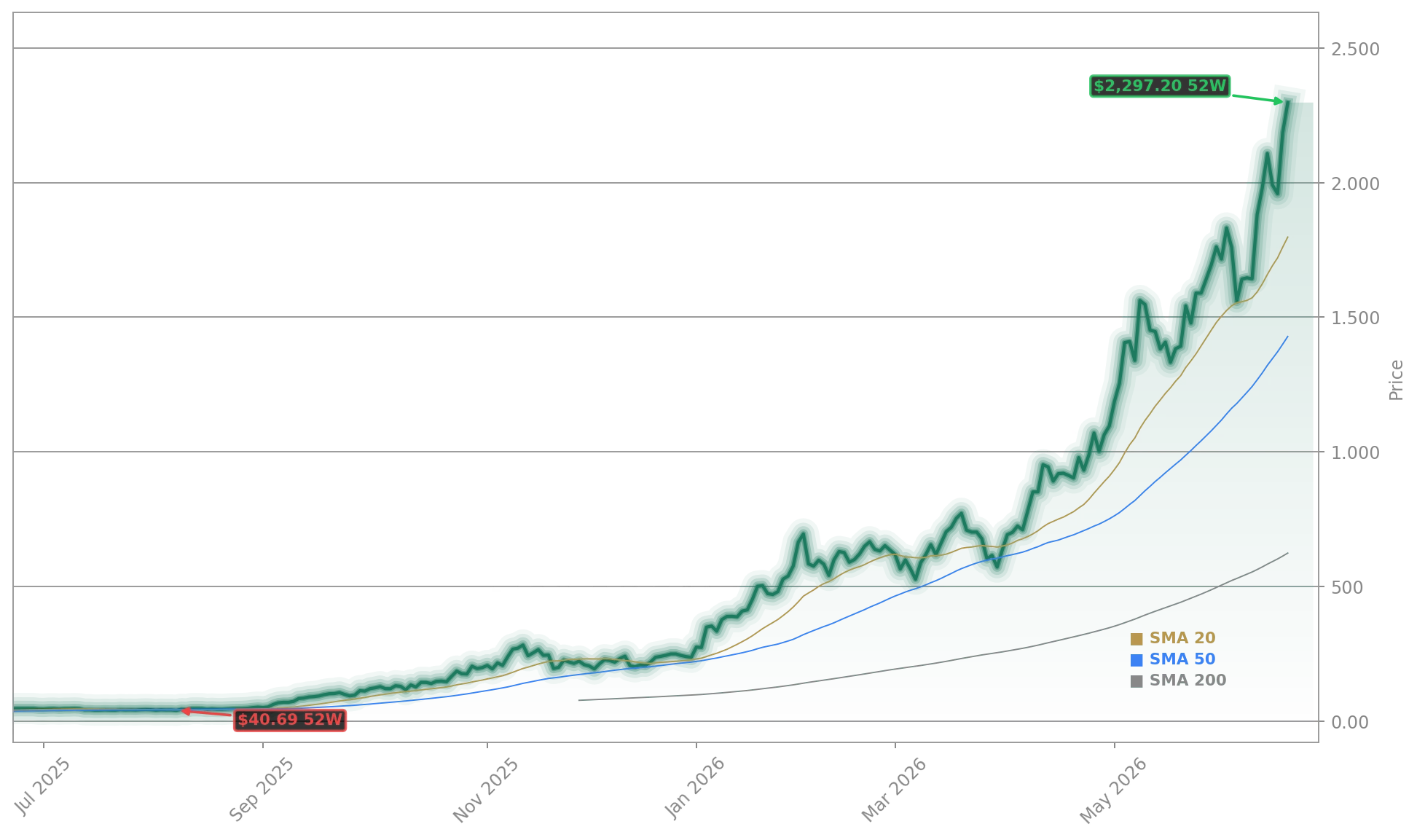

SanDisk (Western Digital) trades in lockstep with Micron Technology (MU) and Western Digital (WDC), both up over 6% following Needham’s $1,550 Micron price target hike. Yet SanDisk’s focus on high-margin enterprise SSDs and ‘high-bandwidth flash’ — positioned as a DRAM alternative — gives it a sharper AI infrastructure moat than Western Digital’s broader HDD/SSD mix. Micron remains the DRAM leader, but SanDisk’s NAND specialization has delivered 251% YoY revenue growth — dwarfing Micron’s 85% and Western Digital’s 42% in the same period. That divergence has made SanDisk the top-performing stock in the S&P 500 year-to-date, up 820%, versus Micron’s 280% and Western Digital’s 140%.

Why Are Analysts So Divided on Valuation?

Wall Street’s split reflects SanDisk’s dual identity: a high-growth AI enabler trading at a forward P/E above 33 — and a cyclical memory commodity business with no pricing power. Among 28 analysts, the median 12-month price target is $1,702 — implying 22% downside from current levels. RBC Capital Markets and Morningstar both set $1,000 targets, citing ‘no economic moat’ and ‘commodity-driven pricing.’ In contrast, Susquehanna’s Mehdi Hosseini raised his target to $3,250 — a 49% upside — while Barclays and Mizuho have issued targets above $2,200. Citigroup notes SanDisk’s ‘durable multiyear contracts’ support ‘structurally higher earnings,’ but warns the stock’s RSI of 70.9 signals overbought conditions.

What Do Institutional Investors See?

Stanley Druckenmiller’s Q1 2026 portfolio shift — exiting Alphabet entirely to add SanDisk (Western Digital), Seagate, Micron, Broadcom, and Arm — underscores institutional conviction in the SanDisk Storage Boom. Polen Capital’s Small-Mid Growth Strategy credited SanDisk as its top Q1 contributor, citing ‘tightening supply, strengthening demand, and margin recovery.’ Yet even bullish funds urge caution: Polen notes ‘improving fundamentals’ but flags ‘narrative-driven volatility’ across SMID-cap tech. Technical indicators reinforce caution — with SanDisk’s RSI at 70.9, Western Digital at 78, and Seagate at 74 — all above the 70 overbought threshold. Still, the NASDAQ-listed stock has held above $2,000 for 11 consecutive trading days — a sign of institutional accumulation.

Related Coverage

These partnerships support durable, structurally higher earnings and a significantly more predictable and less cyclical business for SanDisk.— David Goeckeler, CEO of SanDisk (Western Digital)

For deeper context on SanDisk’s valuation extremes, see SanDisk Record Valuation +10.7% as AI Demand Lifts SNDK, which explores whether current pricing power can survive NAND supply normalization. On the broader AI infrastructure front, Dell AI Infrastructure +2.6% as Rubin AI Factory Ignites shows how hardware partners are capitalizing on the same storage surge — reinforcing SanDisk’s role in the AI stack.