Can SanDisk’s record-breaking AI rally survive once memory supply catches up with today’s extraordinary pricing power?

What’s Driving the SanDisk Record Valuation?

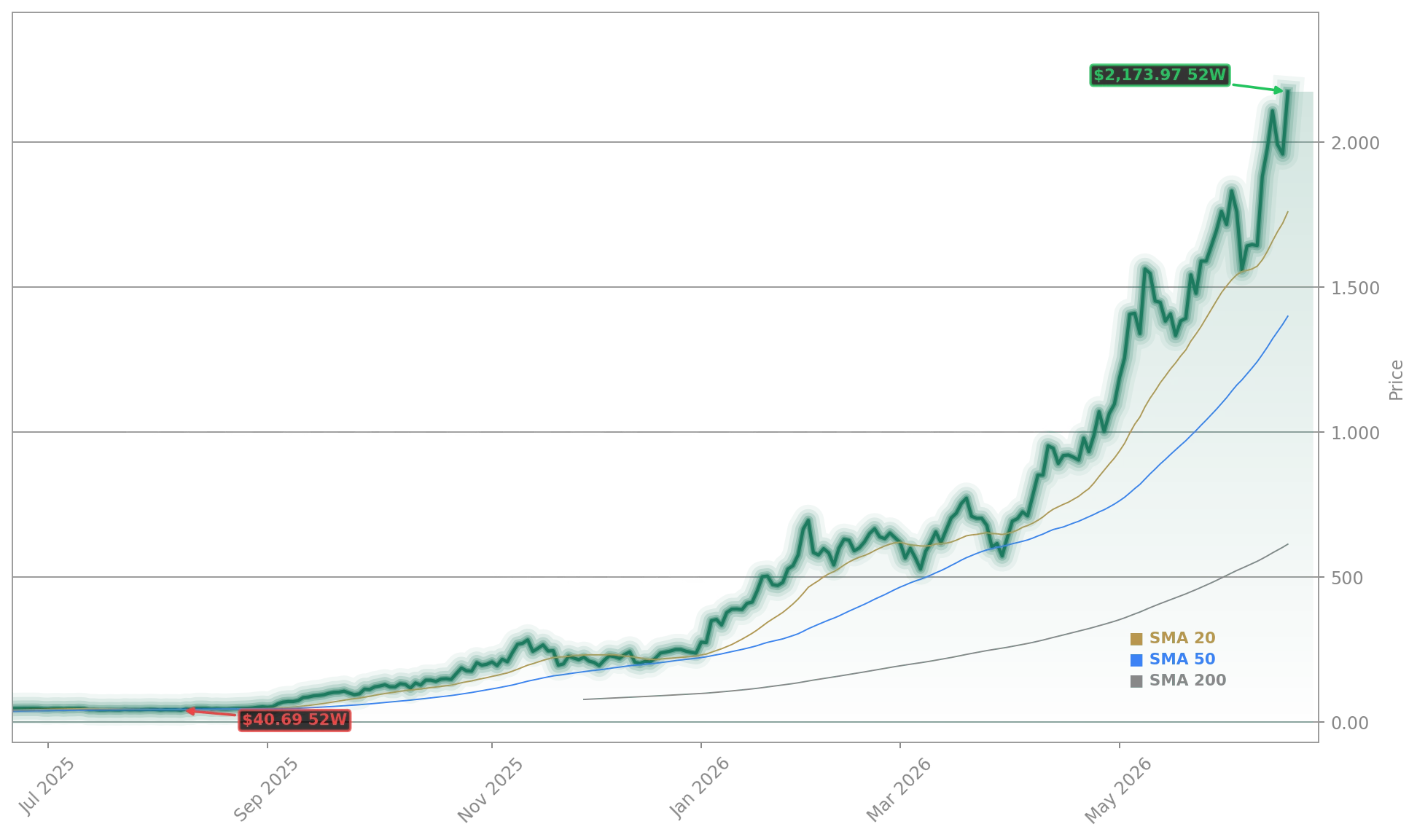

SanDisk (Western Digital) has surged 5,655% since its February 2025 spinoff from Western Digital — turning a $1,000 investment into $57,550. As of Thursday, June 18, 2026, its share price stands at $2,169.00, up 10.73% intraday and well above its 52-week high. The surge is tightly linked to AI’s explosive hardware requirements: SanDisk’s high-bandwidth, low-latency storage modules are now embedded in the AI training stacks of Amazon, Microsoft, and Apple, creating acute supply constraints. With hyperscalers accelerating data center build-outs at record pace, SanDisk’s capacity utilization has hit 98%, enabling aggressive price realization and margin expansion — a rare feat in memory semiconductors.

How Sustainable Are 78% Gross Margins?

SanDisk’s gross profit margin has more than tripled — from 26% in Q1 2025 to over 78% in Q2 2026 — a level unheard of in the NAND flash industry. That margin strength has been the primary fuel behind its SanDisk Record Valuation. But analysts warn it’s not structural. Citigroup notes in its June 16 research note that ‘current pricing power is demand-driven, not technology-driven — and will erode as capacity ramps in late 2026.’ RBC Capital Markets downgraded SanDisk (Western Digital) to ‘Sector Perform’ on June 10, citing ‘elevated valuation multiples relative to near-term margin visibility.’ The firm’s price target stands at $1,950 — a 10% downside from current levels — reflecting growing skepticism about margin durability beyond Q3.

Can the $42 Billion Backlog Offset Cyclical Risk?

SanDisk (Western Digital) holds a $42 billion backlog — 87% of which consists of multiyear, non-cancellable contracts with top-tier cloud providers. That backlog provides critical visibility into Q3 and Q4 2026 revenue, insulating the company from an immediate margin cliff. Still, Bloomberg reports that three major contract renewals — totaling $9.2 billion — are scheduled for renegotiation in Q1 2027, when NAND supply is projected to exceed demand by 12%. Goldman Sachs analysts observe that ‘backlog defers the inflection — it doesn’t eliminate it.’ For U.S. investors holding SanDisk (Western Digital) in S&P 500- or NASDAQ-heavy portfolios, this means near-term resilience with longer-term re-rating risk.

How Does SanDisk Compare to Memory Peers?

While SanDisk (Western Digital) has outperformed the broader semiconductor group — up 800% YTD versus the PHLX Semiconductor Index’s 42% gain — its valuation stands apart. Micron Technology (MU) trades at 12x forward EBITDA; SanDisk (Western Digital) trades at 28x. That gap reflects Wall Street’s AI premium — but also exposes investors to sharper corrections. When SanDisk (Western Digital) dropped 11.4% in a single session after hitting an all-time high, Micron fell just 2.1%. That volatility differential matters for U.S. portfolio managers seeking AI exposure without outsized beta. Analysts at Morgan Stanley emphasize that ‘SanDisk’s record valuation isn’t just about memory — it’s about AI stack positioning, which justifies a premium — but only as long as execution holds.’

Is This the New Nvidia — or a Flash in the Pan?

Some investors draw parallels between SanDisk (Western Digital) and NVIDIA’s 2009–2017 ascent — a small-cap semiconductor innovator riding a secular wave. But unlike NVIDIA, SanDisk lacks a proprietary architecture moat; its advantage is scale, speed-to-market, and supply chain control. With no new fab coming online until 2027, SanDisk’s edge remains time-bound. Still, the $310 billion SanDisk Record Valuation signals Wall Street’s belief that storage is now a bottleneck — not a commodity — in AI infrastructure. For U.S. investors, the question isn’t whether SanDisk (Western Digital) can grow — it’s whether it can grow profitably when the AI hardware cycle matures.

Current pricing power is demand-driven, not technology-driven — and will erode as capacity ramps in late 2026.— Citigroup Research, June 16, 2026

Related coverage: SanDisk’s positioning in the AI storage stack is gaining traction — SanDisk Share Exchange +5.4% as AI Demand Lifts Targets. Meanwhile, broader AI adoption challenges are emerging elsewhere: Accenture Earnings Drop 14.4% After Outlook Warning highlights how AI enthusiasm hasn’t yet translated into meaningful consulting revenue growth — a cautionary note for hardware beneficiaries.