Can Target keep growing sales if shrinking margins keep eating away at the real earnings story?

Is Target Earnings Growth Sustainable?

Target Corporation delivered $25.4 billion in net sales for the quarter ended May 2 — a 6.9% increase year-over-year. That outpaces Walmart’s recent comparable sales growth and marks the first time since 2022 that Target posted positive comp sales across all six core categories. Traffic rose 4.4%, and CEO Michael Fiddelke called the performance “stronger than expected.” Yet this top-line lift masks deeper structural challenges: apparel, home furnishings, and hardlines — which together account for over $10.6 billion in quarterly revenue — face severe headwinds from rising goods inflation (4.78% YoY in May 2026) and a shrinking personal savings rate (3.9% in Q1 2026, down from 6.2% two years prior). Unlike Target Back-to-School +3.7% as TGT Gains Q2 Momentum, this quarter’s growth reflects easier comparisons, not broad-based demand expansion.

Why Did Operating Margins Collapse?

Operating income fell 22.89% year-over-year — a stark contrast to the 17.03% EPS beat reported after earnings. The disconnect stems from persistent cost inflation, elevated inventory carrying costs, and promotional intensity in discretionary categories. After-tax ROIC slid to 12.4% from 15.1%, signaling deteriorating capital efficiency. By comparison, Target Mizrahi Return Powers Target’s Design-Led Comeback highlights a strategic pivot toward premium private brands — but those initiatives haven’t yet offset margin erosion in mass-market categories. Costco (NASDAQ:COST), meanwhile, posted 11.6% revenue growth fueled by $1.37 billion in membership fees and an 89.7% renewal rate — a structural advantage Target lacks.

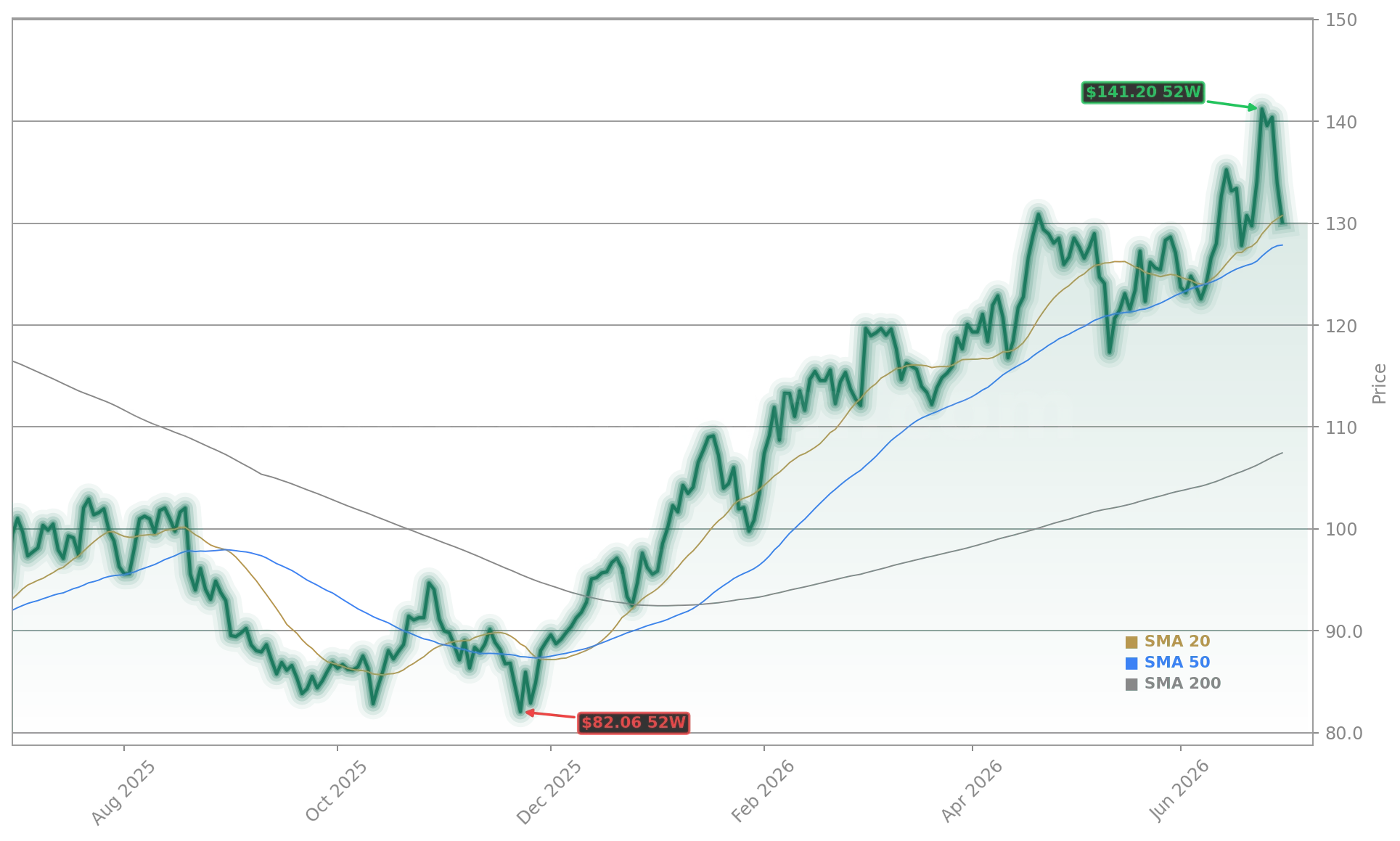

How Does Target Earnings Compare to Rivals?

Target Corporation trades at just 17x trailing earnings — dramatically cheaper than Walmart (40x) and far below the S&P 500’s 22x median. That valuation gap explains much of Target’s 40% YTD stock gain, even as its growth trajectory remains less predictable than that of defensive compounders like Apple or capital-light platforms like Meta. Citigroup recently reaffirmed its “Neutral” rating on Target Corporation but raised its 12-month price target to $142, citing “improved traffic metrics and inventory normalization.” RBC Capital Markets, however, maintains an “Underperform” rating, warning that “margin recovery remains uncertain amid sticky inflation and softening consumer confidence.” The divergence among analysts reflects Wall Street’s split view: Is Target a value play waiting for macro tailwinds — or a cyclical stock vulnerable to further earnings revisions?

What Does This Mean for U.S. Portfolios?

For U.S. investors, Target Corporation represents both opportunity and risk. Its 17x P/E offers a buffer against downside — unlike many tech names trading at premium multiples — but its exposure to discretionary spending makes it sensitive to Fed policy shifts and labor market softening. With the NASDAQ up 14% YTD and the S&P 500 flat, Target’s outperformance has provided diversification benefits to growth-heavy portfolios. Yet its lack of earnings consistency — with revenue barely above its $25.3 billion level from three years ago — suggests the recent rally may be front-running rather than fundamentals-driven. Institutional buyers are watching closely: if Q2 2026 Target Earnings show margin stabilization alongside continued comp growth, the stock could retest its 52-week high. If not, the valuation gap with Walmart may narrow sharply.

Can Design and Discipline Deliver a Real Turnaround?

“Stronger than expected” — but there is much more work in front of us.— Michael Fiddelke, CEO of Target Corporation

Target’s return of designer Isaac Mizrahi — now spearheading a new home and apparel line — signals a long-term bet on brand-led margin expansion. But design alone won’t fix logistics costs or shrink promotional drag. The company’s 2026 capital allocation plan includes $2.1 billion in store remodels and supply chain automation — investments aimed at improving gross margin by 50–75 basis points by year-end. Still, with gross margin down 110 bps year-over-year and SG&A costs rising 4.2%, investors need proof that operational discipline can catch up to marketing momentum. The next quarterly report — due in August — will test whether Target’s Target Earnings story is shifting from recovery to resilience.