Can AMD’s massive AI infrastructure growth offset the short-term margin dilution that is currently spooking Wall Street?

Why is AMD experiencing a sharp pre-market pullback?

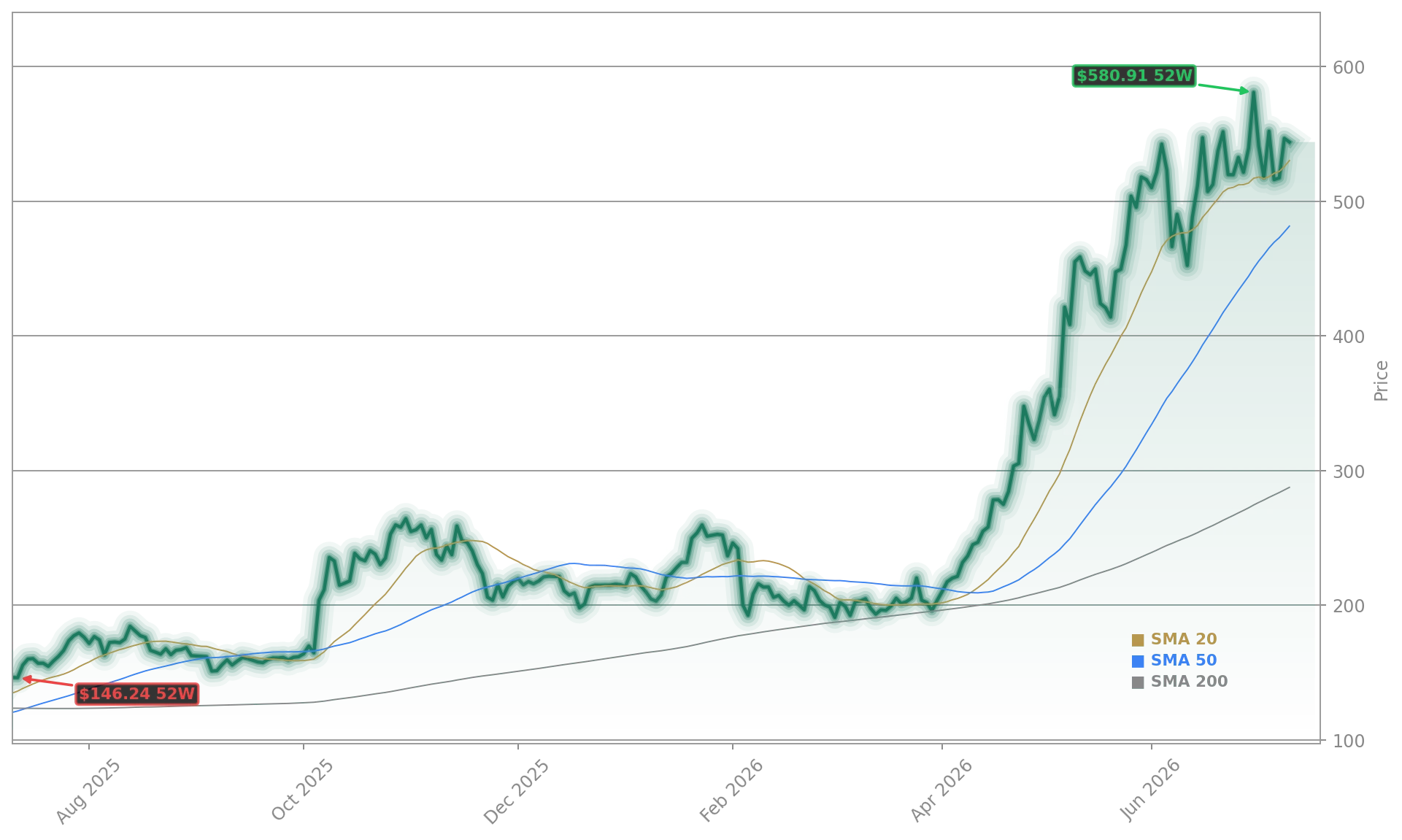

Tech stocks faced heavy pressure on Monday morning as investors questioned the sustainability of aggressive artificial intelligence infrastructure spending. Advanced Micro Devices, Inc. slipped 4.63% to $532.26, down from its previous close of $557.89. The decline was part of a broader industry-wide retreat triggered by profit-taking in Asian markets. South Korea’s SK Hynix fell sharply following its stellar U.S. trading debut, dragging down rival memory and hardware manufacturers like Micron and SanDisk.

This market-wide pressure has complicated the technical outlook for the chipmaker. Traders are closely watching whether the stock can maintain its 10-day and 20-day moving averages. If these key technical levels fail to hold, further downward momentum could be on the horizon. Upcoming earnings reports from major industry players like ASML and TSMC later this week are expected to serve as critical indicators for the momentum of the global AI trade.

How does the AMD Analysis view the competitive landscape?

Despite the immediate market volatility, institutional support for the semiconductor pioneer remains robust. In a recent AMD Analysis, investment bank Stifel raised its price target on the stock to $635 from $450 while maintaining a Buy rating. The firm pointed to sustained strength in AI infrastructure spending, a healthy order backlog, and multi-year capacity commitments as primary drivers. However, some analysts view this aggressive target adjustment as playing catch-up to the stock’s massive 303% gain over the trailing twelve months.

Competition in the high-performance computing sector is intensifying rapidly. While NVIDIA remains the dominant force in AI training and inferencing, other players are making strategic moves. For example, autonomous driving startup Turing Inc., backed by AMD Ventures, recently began integrating these AI accelerators into its systems to ensure cost competitiveness for its planned 2028 robotaxi launch. While Turing has historically relied on rival hardware, it now handles approximately 10% of its training needs using graphics processors from Advanced Micro Devices, Inc.

What are the main risks facing the company’s margins?

The core of the current debate lies in the balance between rapid growth and corporate profitability. Management has significantly revised its long-term forecast for the server CPU market, projecting annual growth of over 35% to reach $120 billion by 2030, driven by the rise of Agentic AI. Server CPU revenue is expected to surge by more than 70% year-over-year in the second quarter alone.

However, this rapid expansion brings unique challenges. The company’s highly anticipated new AI accelerators carry gross margins that are currently below the corporate average. This means the fastest-growing segment could dilute overall corporate profitability in the short term. Additionally, rising memory costs and declining gaming revenues—expected to drop by more than 20% in the second half of the year—add further pressure. Investors are advised to closely monitor the Data Center segment’s operating margin, which stood at 28% last quarter, to evaluate if scaling is translating into profitable growth.

Related Coverage

To better understand the broader market dynamics and how they impact your portfolio, explore our detailed coverage of the semiconductor sector. Read our analysis on the AMD Forecast +7.4% Surge as AI Demand Lifts Q2 Outlook to see how the company’s revenue projections are holding up. Additionally, compare these developments with its main x86 rival by reading about the Intel Investment Ireland: Stock Drops -3.2% Despite Massive Expansion to understand the wider European manufacturing landscape.