Can Intel justify its turnaround hype before earnings, or is the latest sell-off a warning that Wall Street got ahead of itself?

Is the Intel Forecast Too Optimistic?

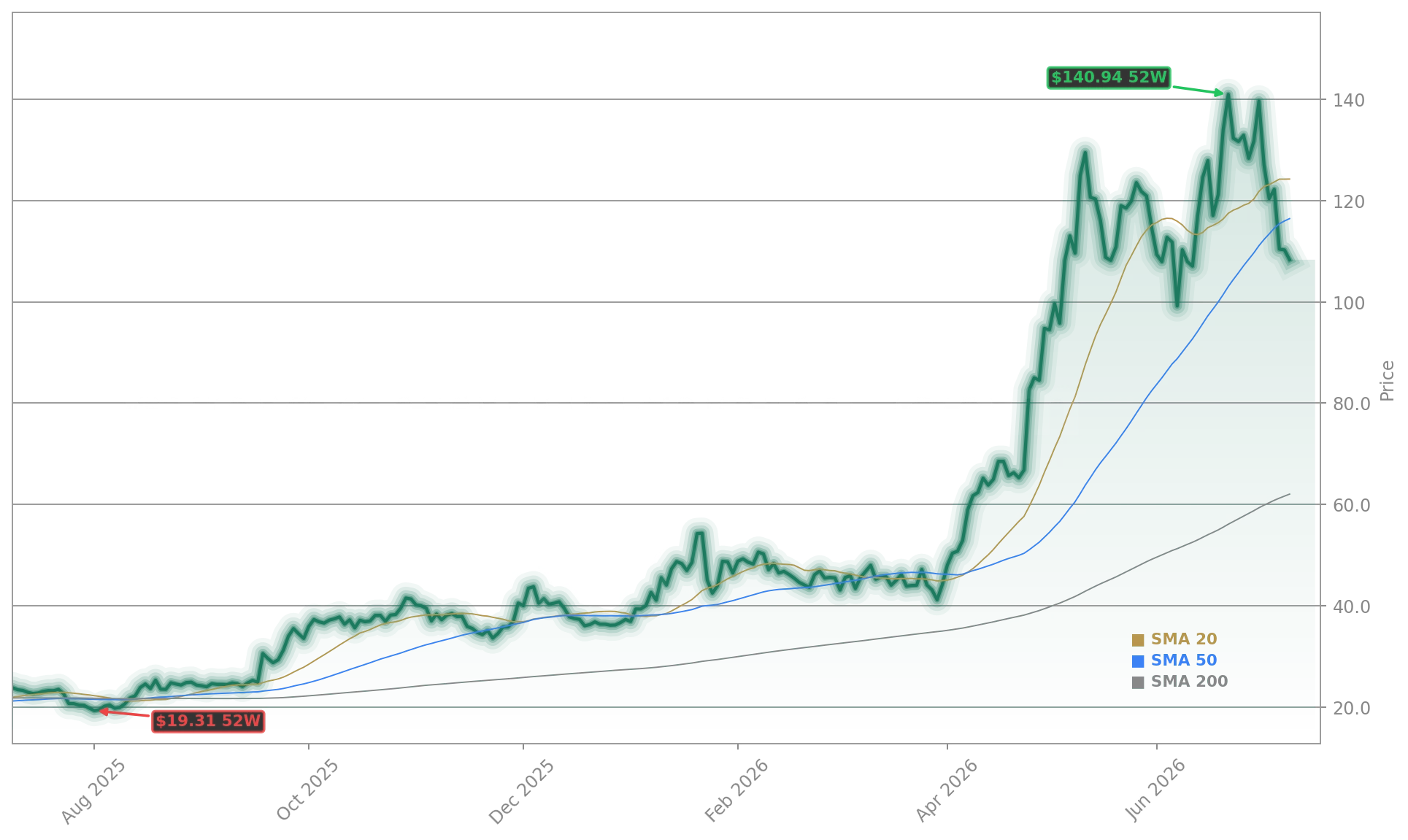

Intel Corporation shares are testing key near-term support at $102.50 after falling 3.99% from Thursday’s close — a retreat amplified by broader semiconductor volatility and Nasdaq futures slipping 0.36% premarket. The pullback follows a 372% 12-month rally, now under scrutiny as the Q2 earnings report looms. Consensus forecasts project $14.40 billion in revenue and $0.19 EPS — modest growth, but critical as a barometer for the foundry turnaround and data-center rebound. The Intel Forecast isn’t just about numbers; it’s about whether Wall Street’s $200 price target from HSBC or JPMorgan’s structural short thesis better reflects reality. With RSI at 45.25 — neutral but trending lower — momentum is fading just as expectations peak.

How Does AMD Reshape the Intel Forecast?

Advanced Micro Devices (AMD) posted $5.8 billion in data-center revenue in Q1 2026 — surpassing Intel’s $5.1 billion in the same segment for the third consecutive quarter. That shift isn’t just symbolic: AMD’s EPYC processors and Instinct AI accelerators now power hyperscalers like Microsoft and Oracle at scale, while Intel’s 18A manufacturing process remains delayed to 2027 for profitable yields. Crucially, AMD’s gross margin exceeds 50%, and its forward P/E sits at 59 — rich, but justified by execution. Intel, by contrast, trades at over 100x forward earnings despite unprofitability in its foundry unit. The Intel Forecast must now reconcile accelerating share loss in server CPUs with promises of AI-driven foundry wins — a tension that’s pricing in success before proof.

What Do Analyst Upgrades Really Signal?

Stifel analyst Ruben Roy maintains a Hold rating on Intel Corporation while lifting the price target from $75 to $120 — a 12% upside from current levels. HSBC goes further, reiterating Buy with a $200 target, citing server CPU momentum and foundry potential as a TSMC alternative. Yet JPMorgan semiconductor analyst Harlan Sur counters with a top-tier short call, arguing the stock reflects a turnaround already complete — when in fact external foundry revenue remains under $200 million and margins deeply negative. Jay Goldberg of Seaport adds a bullish voice, calling Intel a ‘fundamentally re-rating’ story under new leadership. This analyst split isn’t noise — it’s a market-wide warning that the Intel Forecast hinges on milestones still in development, not delivered.

Where Does the Intel Forecast Fit in the AI Chip Stack?

Intel’s relevance in AI infrastructure is no longer about GPUs — it’s about CPUs, packaging, and memory. SK Hynix’s reported interest in expanding its packaging relationship with Intel adds tangible validation, while a newly filed cross-batch memory (XBM) patent targets AI’s memory bandwidth bottleneck — though commercialization remains beyond 2030. Meanwhile, Cathie Wood’s ARK Invest notes AMD chips are now ‘more performant per dollar’ than NVIDIA in select AI workloads, reinforcing CPU-centric agentic AI as a growth vector. For U.S. portfolios, the Intel Forecast must weigh these long-term bets against near-term execution: Micron Technology’s $250 billion U.S. investment plan and Apple’s reported AI hardware partnerships signal sector-wide confidence — but Intel’s lag in 18A yields and server share erosion remain structural headwinds the Intel Forecast can’t ignore.

Intel Forecast: What’s Next for Wall Street?

With Q2 earnings due July 23, the Intel Forecast will pivot from narrative to numbers — specifically, foundry revenue growth, gross margin trajectory, and data-center order visibility. A beat could validate HSBC’s $200 thesis; a miss may trigger further short-covering pressure. Technically, Intel Corporation must reclaim $110.96 (50-day EMA) to signal the pullback is a pause — not a reversal. For S&P 500 and NASDAQ investors, Intel remains a barometer: if its turnaround stalls, the broader AI infrastructure trade — including peers like Tesla and NVIDIA — faces renewed valuation discipline. The Intel Forecast isn’t just about one stock — it’s about how much future profit investors are willing to pay for today.

Related coverage: The sharp 10.1% Intel chip selloff last week has raised questions about AI spending sustainability — Intel Chip Selloff -10.1%: Warning Sign for AI Bulls. Meanwhile, broader AI governance concerns — highlighted by Anthropic’s appointment of former Fed Chair Ben Bernanke — are reshaping how investors assess risk across the sector — Anthropic Bernanke Appointment Signals AI Governance Warning.

Intel is a company we’d left for dead two years ago and has a new CEO and a new lease on life.— Jay Goldberg, Seaport

Intel Corporation remains a pivotal test of AI infrastructure valuation discipline. The Intel Forecast reflects both extraordinary potential and unresolved execution risk. For U.S. investors, the next earnings report isn’t just a data point — it’s a stress test for the entire semiconductor bull case. The Intel Forecast matters most not as a prediction, but as a lens into what Wall Street demands before rewarding transformation.