Is Intel’s AI comeback finally real, or is the market racing ahead of what the company can actually deliver?

Why Is Intel Outpacing AMD Today?

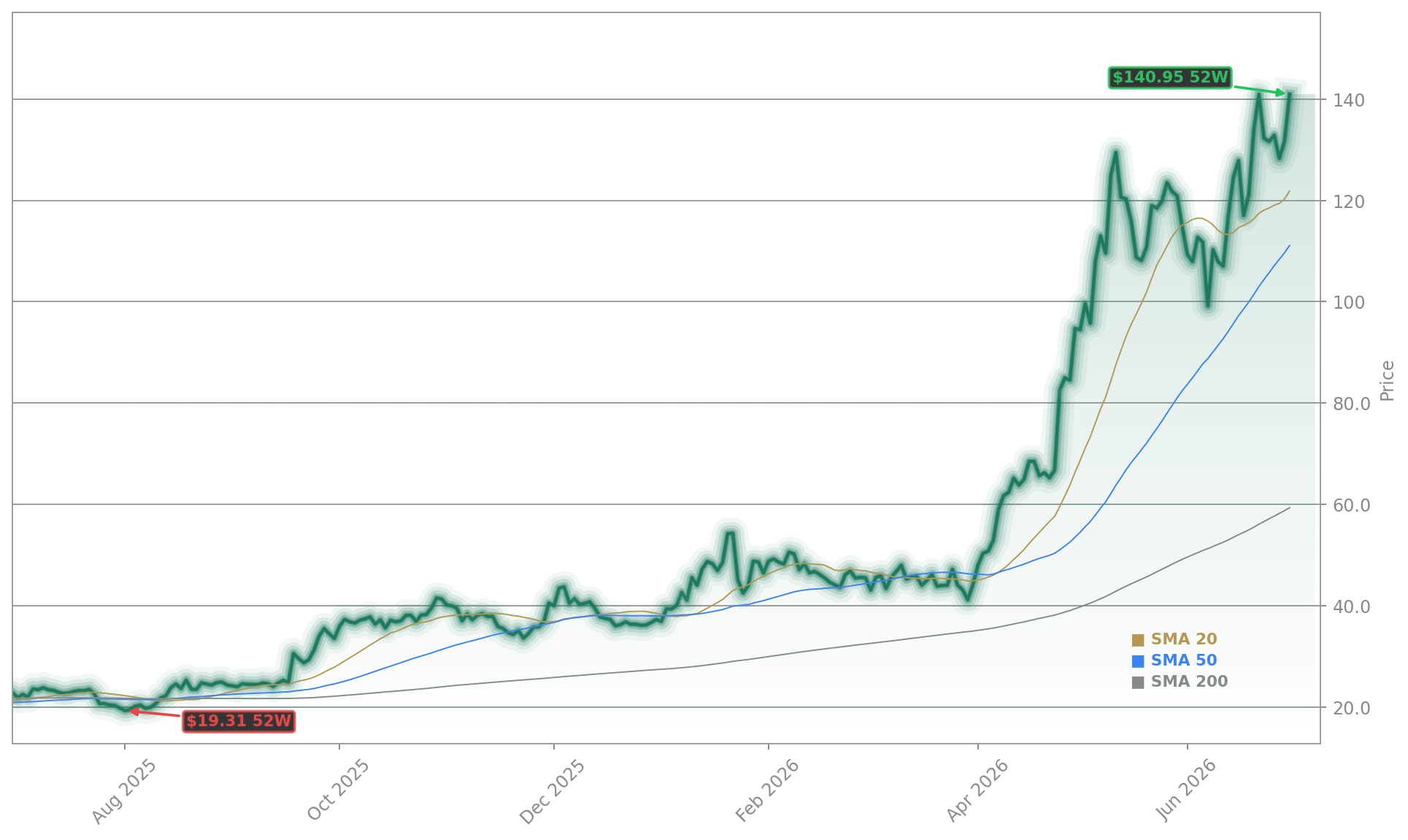

Intel Corporation and Advanced Micro Devices both rose 7% on Tuesday, but Intel’s 277% year-to-date gain dwarfs AMD’s 163% — making it the top-performing semiconductor stock in the S&P 500 this year. Unlike AMD, whose valuation sits at 172x earnings, Intel trades at over 900x forward earnings, signaling aggressive pricing of future AI monetization. The surge isn’t driven by new product announcements, but by a structural shift in investor perception: CPU-centric AI inference is gaining credibility as a growth vector. Wells Fargo analyst Aaron Rakers’ recent upgrade of AMD to $615 — citing 68% CPU revenue growth in 2026 — indirectly bolstered Intel’s narrative, given its dominant position in server CPUs and Xeon 6’s designation as the host CPU for NVIDIA’s DGX Rubin NVL8 platform.

What Does the Intel AI Forecast Say About Valuation?

The Intel AI Forecast now incorporates accelerating demand for AI-optimized CPUs in edge inference, cloud-scale reasoning, and enterprise LLM deployment — segments where power efficiency, latency, and software stack maturity matter more than raw GPU throughput. While NVIDIA remains the undisputed leader in training, Intel’s ecosystem alignment with Microsoft, Meta, and major cloud providers is strengthening. RBC Capital Markets recently reaffirmed its ‘Sector Perform’ rating on Intel Corporation, citing ‘improved foundry execution and growing AI inference tailwinds,’ though it maintains a $96 price target — well below current levels. Citigroup, meanwhile, raised its 12-month target to $132, noting ‘material progress in Intel Foundry’s customer wins and AI-optimized chiplet adoption.’ The Intel AI Forecast suggests revenue from AI-adjacent CPU and infrastructure solutions could reach $12.4 billion by 2027 — up from $5.05 billion in Q1 2026.

How Does Intel Compare to Broader Chip Leaders?

Intel Corporation’s 277% YTD gain exceeds not only AMD but also Apple (+6.99%), Tesla (+3.05%), and Micron Technology (+5.3%). It trails only NVIDIA (+7.83%) in the NASDAQ-100 semiconductor subgroup — yet trades at a valuation multiple nearly 30x higher than NVIDIA’s 30x P/E. This disconnect reflects both optimism and risk: Intel’s AI execution remains unproven at scale, and its foundry division reported $2.1 billion in Q1 operating losses. Still, the company’s inclusion in the Direxion Daily Semiconductor Bull 3X Shares (SOXL) — where Intel holds a 3.57% weight — confirms its centrality to the AI chip trade. Broadcom and AMD each hold ~4.5% weights, underscoring Intel’s equal footing in institutional AI infrastructure exposure.

What’s Next for Intel’s AI Infrastructure Play?

Intel’s Q1 2026 results confirmed $5.05 billion in Data Center and AI revenue — a 22% year-over-year increase — with CEO Lip-Bu Tan explicitly naming Intel Xeon 6 as the foundational CPU for NVIDIA’s next-gen DGX Rubin systems. That partnership, combined with Microsoft’s Azure AI inference deployments and Meta’s custom AI chip co-development, forms the backbone of the Intel AI Forecast. Looking ahead, Intel’s 18A process node — scheduled for volume production in Q4 2026 — will determine whether it can deliver competitive AI accelerators alongside its CPU roadmap. Analysts at Goldman Sachs warn that ‘foundry profitability remains the largest overhang,’ but affirm that ‘AI inference demand could accelerate gross margin expansion by 2027.’ The Intel AI Forecast now assumes 35% gross margin improvement in the Data Center segment by Q2 2027 — up from 28% in Q1.

Intel Xeon 6 is the host CPU for NVIDIA DGX Rubin NVL8 systems — a critical validation of our AI infrastructure roadmap.— Lip-Bu Tan, CEO of Intel Corporation

Related Coverage: For deeper analysis on Wall Street’s conflicting views on Intel’s valuation, read Intel Goldman Sachs Coverage: $150 Target Meets Caution. To understand how AMD’s rising AI targets are reshaping competitive dynamics, see AMD Forecast +3.4% as AI Target Hikes Fuel Fresh Optimism.