Can Intel justify a $150 target when foundry momentum is rising but losses and AI execution risks still loom?

What Does Intel Goldman Sachs Coverage Mean for NASDAQ?

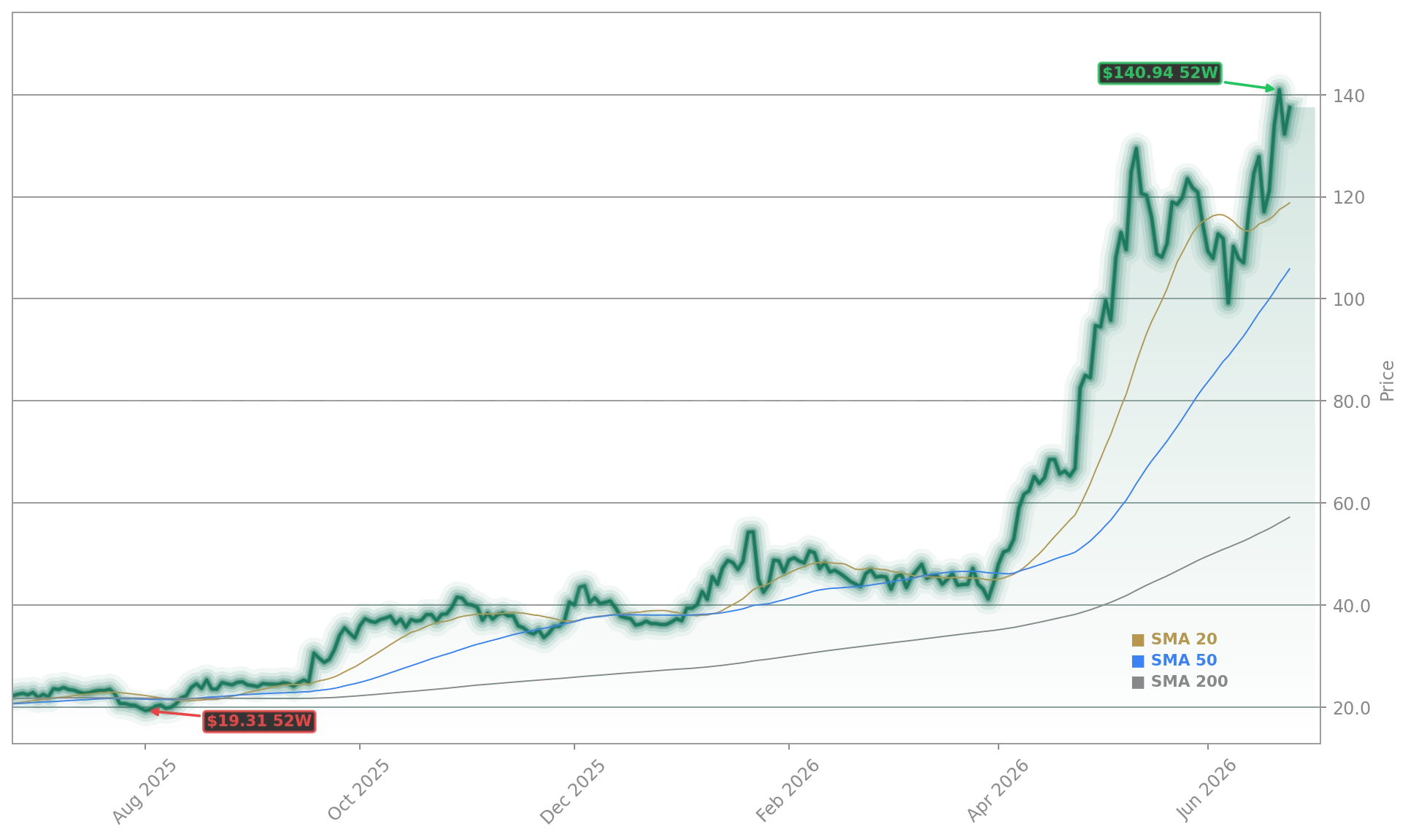

Goldman Sachs analyst James Schneider initiated coverage on Intel Corporation with a Neutral rating and $150 price target on June 25, 2026 — a move that adds institutional weight to the stock’s recent rally but also signals caution. The $150 target implies just 8.6% upside from current levels, far below the 259% year-to-date gain. This contrasts sharply with Bank of America’s $160 target — raised from $135 — citing expanding AI server demand and foundry growth. For S&P 500 and NASDAQ investors, the divergence underscores a broader tension: Is Intel a value play in U.S. chip sovereignty, or a momentum stock priced for perfection? With its P/E ratio exceeding 900, Intel remains one of the most expensive names in the index — a red flag for long-term allocators wary of overexposure to policy-driven narratives.

How Does Intel Stack Up Against AMD and NVIDIA?

While NVIDIA continues to dominate AI accelerator revenue and AMD gains share in server CPUs — projecting a $120 billion market by 2030 — Intel’s resurgence is anchored in manufacturing, not just design. Its $5.4 billion in Q1 foundry revenue marks a 16% year-over-year jump, yet the segment posted a $2.4 billion operating loss. Meanwhile, AMD’s pricing power and manufacturing discipline have widened its margin advantage. Crucially, Intel’s recent wins — including a 3-million-unit Tensor Processing Unit (TPU) order from Google and rumored collaboration with Apple — remain pre-revenue. As BNN Bloomberg notes, volume production for Apple chips isn’t expected until late 2027 or early 2028. That timeline tempers near-term earnings visibility, even as sovereign AI demand boosts Intel Xeon 6 and Arc Pro B60 adoption across government and enterprise sectors.

Is the Government Backing Enough to Justify Valuation?

The U.S. government’s $8.9 billion investment — giving it a ~10% stake — has become Intel’s most potent catalyst, reinforcing its role as a national security asset and domestic foundry anchor. This aligns with Masayoshi Son’s recent defense of Intel as essential to reducing reliance on Taiwan Semiconductor Manufacturing Co. Yet, government support doesn’t erase execution risk: Intel’s Q1 2026 net loss of $3.7 billion and negative $2.54 billion cash flow reveal a company still in heavy reinvestment mode. While the Terafab project with Tesla and SpaceX promises long-term upside, it adds complexity — not near-term earnings. For U.S. investors, the question isn’t whether Intel matters, but whether today’s price already prices in five years of flawless execution.

What’s the Real Risk for Intel Goldman Sachs Coverage Holders?

Intel’s turnaround is impressive — but its valuation is pricing in perfection. If the U.S. government continues to favor Intel, the stock’s premium could be justified. If not, the correction could be steep.— James Schneider, Goldman Sachs

The biggest risk isn’t competition — it’s valuation compression. Intel Goldman Sachs Coverage arrives amid rising skepticism toward semiconductor momentum stocks. A recent broad-based tech sell-off triggered an 8% pre-market dip, reflecting profit-taking after the stock’s staggering run. With its PEG ratio below 1, growth potential remains credible — but only if Intel converts pipeline wins into GAAP profitability. Micron’s success as a memory enabler for NVIDIA and Google shows how supplier leverage can drive earnings — yet Intel’s foundry business remains unprofitable despite rising sales. Until operating leverage materializes, Intel Goldman Sachs Coverage will remain a story of promise, not proof.