Can AMD’s AI-driven data center momentum really justify a $670 target, or is Wall Street getting ahead of itself again?

Why Is UBS So Bullish on AMD Forecast?

UBS analyst Timothy Arcuri led the $215 target hike, citing a decisive inflection in AI infrastructure architecture. Rather than relying solely on GPU parallelism for training, agentic AI systems — which orchestrate dynamic, multi-step reasoning — demand high-core-count, low-latency CPUs for real-time inference, memory management, and workload coordination. Arcuri emphasized AMD’s leadership in core density, x86 software compatibility, and multi-threading efficiency — advantages that position EPYC processors as indispensable in next-gen data centers. This isn’t incremental growth; it’s a structural tailwind, with Gartner naming AMD the top vendor for enterprise AI server CPUs in its latest report.

How Does AMD Compare to NVIDIA and Intel?

While NVIDIA dominates GPU-accelerated training with an ~80% market share, its absence in the high-performance CPU server market creates a strategic opening — one AMD is aggressively filling. Unlike Intel, which continues to grapple with manufacturing execution and market share erosion, AMD’s EPYC has captured ~41% of server CPU revenue. And unlike Apple or Qualcomm, AMD ships both CPUs and GPUs optimized for co-deployment — a key differentiator in rack-scale AI systems like Oracle’s 50,000-GPU Helios cluster and Meta Platforms’ 6-gigawatt Instinct rollout. Intel remains a distant third in AI server CPUs, while Arm Holdings (ARM) competes on architecture licensing — not silicon — making AMD’s fabless, full-stack execution uniquely scalable.

What Does the Q1 2026 Earnings Say About AMD Forecast?

Advanced Micro Devices, Inc. reported Q1 FY2026 revenue of $10.25 billion — up 38% year over year — with Data Center revenue surging 57% to $5.78 billion. Gross margin expanded to 49.5%, and free cash flow more than tripled to $2.57 billion. Management’s Q2 FY2026 guidance calls for $11.2 billion in revenue (46% YoY growth) and non-GAAP gross margin approaching 56%. These numbers validate the AMD Forecast upgrade: customer demand for MI450 GPUs and 6th Gen EPYC is outpacing initial expectations, with Meta, OpenAI, and Oracle anchoring a $120 billion agentic AI CPU opportunity over the next three years.

Are Valuation and Policy Risks Overlooked?

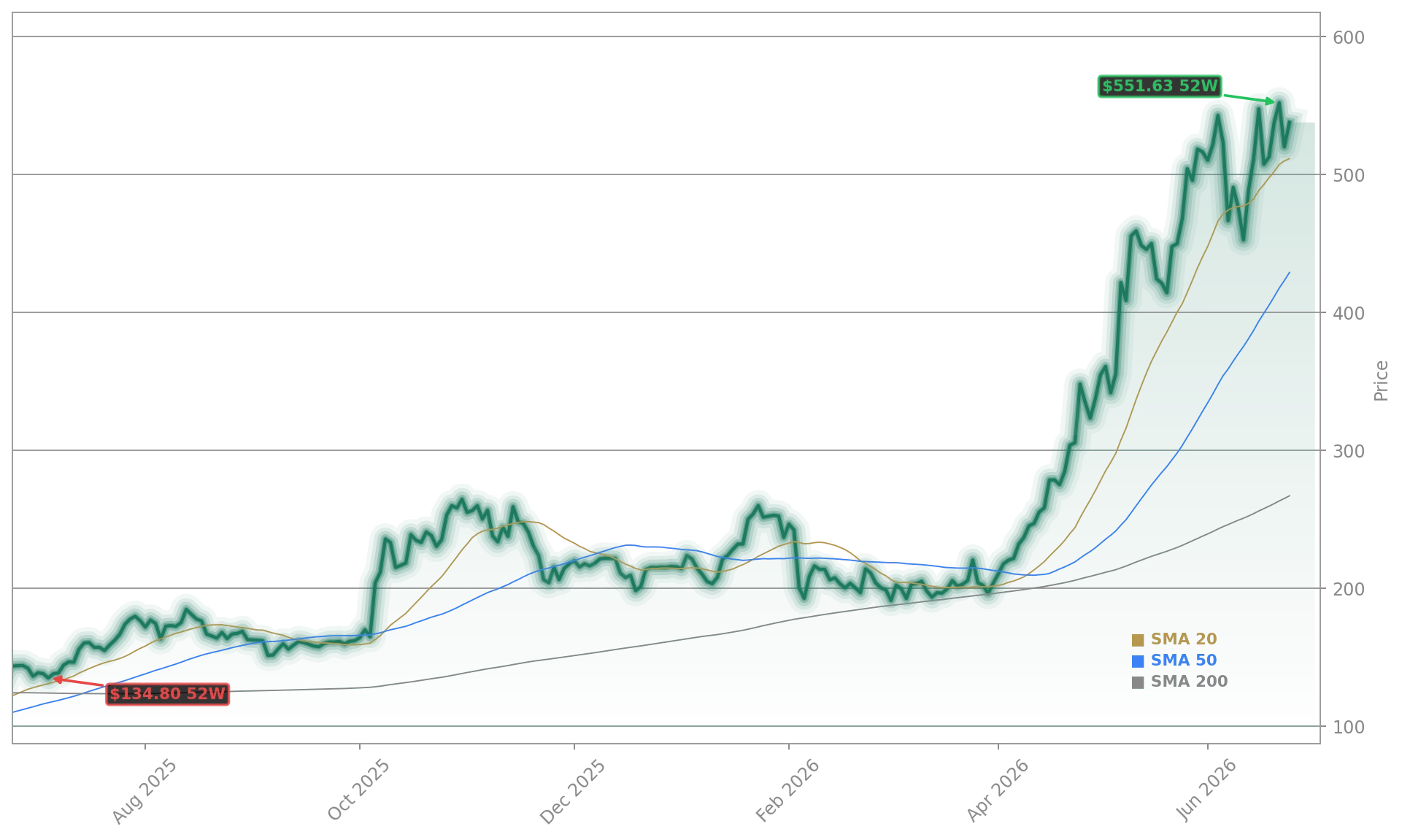

Yes — and that’s the bear case. AMD trades at a trailing P/E of 172x, leaving virtually no margin for error. A prior $800 million export-control charge highlights persistent China policy risk, and insider selling — including by CEO Lisa Su — totaled over $161 million in the last 90 days, though much appears tied to routine portfolio diversification. Meanwhile, Micron (MU), with which AMD shares a 0.97 correlation over three months, recently cratered 11%, dragging AMD down 4.77% in sympathy. With the stock still below its 52-week high of $562.99, the $670 target implies both flawless execution and continued multiple expansion — a high bar in a rising-rate environment.

What’s Next for AMD Forecast and Investor Strategy?

Three catalysts will define the near-term AMD Forecast trajectory: the MI450 ramp velocity through Q3, HBM4 supply timing from Samsung, and any U.S. policy updates on China export controls. Investors should monitor whether AMD holds above $520 in after-hours trading — a key technical support level — and watch for commentary on Vera Rubin (NVIDIA’s upcoming CPU-GPU integrated platform), which could further validate CPU demand. With 80% of Wall Street analysts rating AMD a Buy or Strong Buy, the consensus is clear — but the real test is whether fundamentals sustain the valuation. The next quarterly earnings report will be decisive.

Standalone CPU racks are gaining adoption, supported by AMD’s lead in core density, multithreading, and the established x86 software ecosystem.— Timothy Arcuri, UBS analyst

Related coverage: AMD’s recent acquisition of MEXT — a memory optimization software firm — is expanding its AI infrastructure stack beyond silicon, as detailed in AMD Acquisition -5.2% as AI Infrastructure Strategy Expands. Meanwhile, investors weighing AMD against Arm Holdings should consider how Arm Holdings Forecast +3.7% as AI CPU Demand Surges reflects divergent paths in the AI CPU race — licensing versus silicon.