Could Broadcom’s expanded Apple deal turn a supplier risk into one of the clearest long-term revenue stories in semiconductors?

What Does This Mean for Broadcom’s Revenue Visibility?

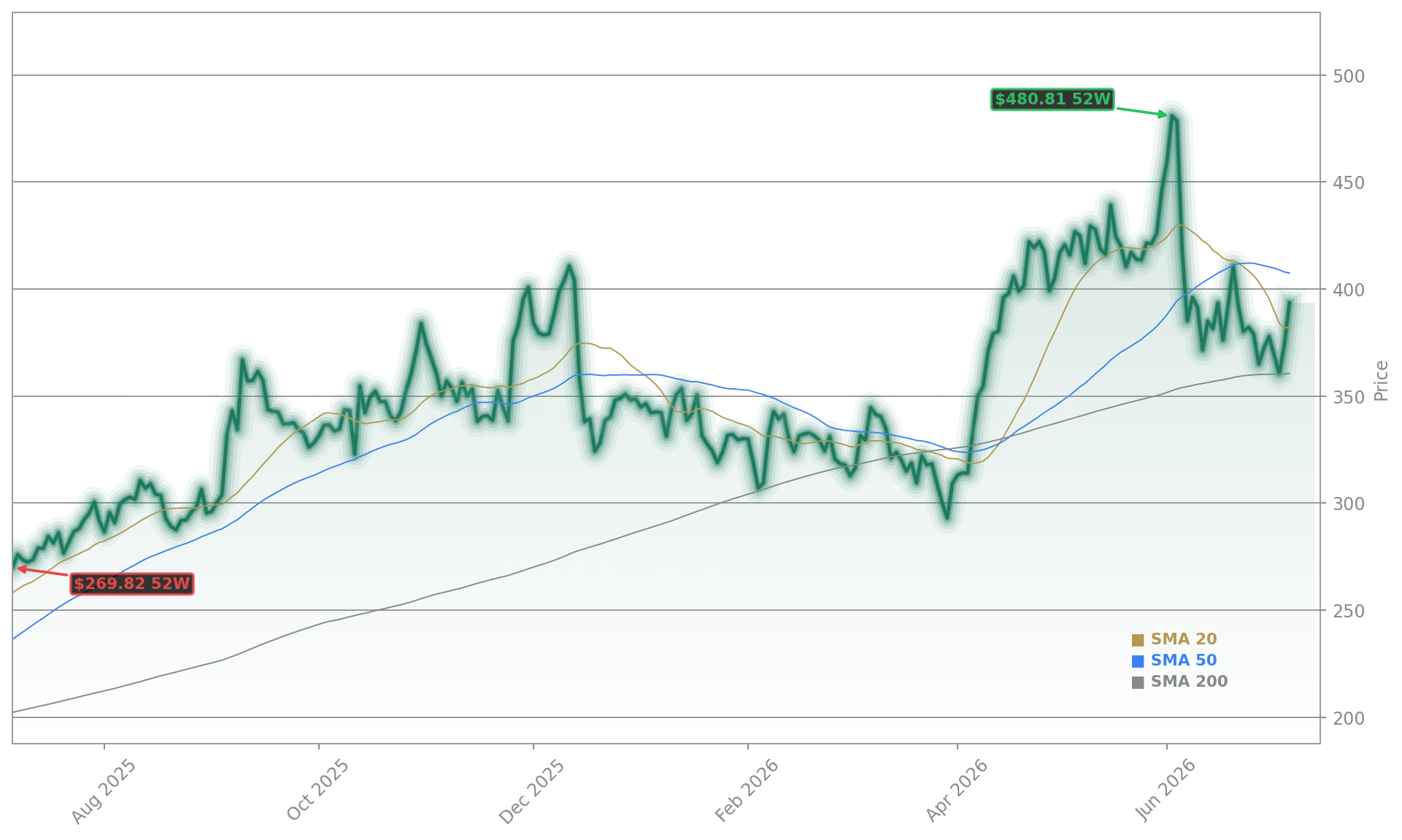

Broadcom Inc. surged 3.9% premarket and closed up 4.5% on Wednesday — a stark contrast to the broader semiconductor selloff, where the Philadelphia Semiconductor Index dropped 5.5% and peers like Intel (INTC) and AMD fell sharply. The rally underscores investor relief over de-risking Broadcom’s Apple exposure: Apple accounts for roughly 20% of Broadcom’s revenue, and concerns had mounted about Apple’s internal chip development displacing suppliers. This Broadcom Apple Partnership locks in scale, duration, and geographic specificity — with Apple committing to U.S.-manufactured FBAR filters, RF components, and custom ASICs for cellular, Wi-Fi, Bluetooth, and GPS connectivity. According to Briefing.com Analyst Insight, the $30 billion figure implies over $6 billion in average annual revenue — though exact cadence, margins, and incremental volume remain undisclosed.

How Does This Compare to Apple’s Other Chip Partners?

Unlike its deepening ties with NVIDIA for AI data center accelerators or its long-standing collaboration with Tesla on automotive silicon, the Broadcom Apple Partnership focuses squarely on connectivity — a high-margin, mission-critical franchise Broadcom dominates. While Apple has in-sourced modems and application processors, it continues to rely on Broadcom for RF front-end modules where integration complexity and performance demands remain prohibitive for internal development. This strategic division of labor mirrors Apple’s approach with Qualcomm — but with a decisive U.S. manufacturing twist. The $1.5 billion Colorado investment directly aligns with Trump administration industrial policy, contrasting with Biden-era CHIPS Act subsidies and accelerating the shift away from Asian semiconductor assembly. Notably, Broadcom’s recent co-development of the ‘Jalapeño’ AI inference processor with OpenAI confirms its dual-track capability — serving both hyperscalers and device OEMs like Apple.

Is This Deal More Than Just Connectivity?

Yes — and the implications extend beyond wireless. The SEC filing explicitly references ‘custom ASIC silicon products’ for ‘multiple generations of Apple products’ through 2031, opening the door to AI-optimized chips for future iPhones, Macs, and even server-class hardware. Bloomberg confirmed the pact expands Broadcom’s role in AI silicon, not just legacy connectivity. That’s critical context for investors watching Broadcom’s $16 billion AI semiconductor revenue guide for Q3 FY2026 — a 200% year-over-year jump that analysts at JPMorgan see as the most reliable leading indicator for the broader NASDAQ-100. As one AI Investor Podcast panelist noted, ‘NVIDIA, Micron, and Broadcom together drive nearly half of NASDAQ-100 profit growth’ — and Broadcom’s ability to compound AI revenue off a diversified base makes it uniquely positioned for sustained upside.

How Are Analysts Reacting to the Broadcom Apple Partnership?

Citigroup raised its price target on Broadcom Inc. to $435, citing ‘enhanced visibility, reduced supply chain risk, and accelerated U.S. manufacturing tailwinds.’ RBC Capital Markets upgraded the stock to ‘Outperform,’ emphasizing that the deal ‘de-risks near-term revenue concentration concerns while validating Broadcom’s leadership in custom silicon beyond AI accelerators.’ Goldman Sachs reiterated its ‘Buy’ rating, noting the $30+ billion commitment ‘materially de-risks the 2027–2031 revenue trajectory’ and strengthens Broadcom’s position relative to peers like Marvell Technology and Qualcomm. Importantly, the deal arrives just as Broadcom’s valuation has normalized: its forward P/E now sits at 19 — down from 40 just six weeks ago — making the stock significantly more accessible for long-term portfolios.

What’s Next for the Broadcom Apple Partnership?

With the Colorado facility expansion expected to begin construction in late 2026 and ramp through 2027, the first wave of U.S.-made chips will likely debut in Apple’s 2028 product cycle. The partnership also sets a precedent for other U.S. tech giants — particularly as Washington tightens export controls and incentivizes domestic chip production. Broadcom’s $200 billion AI opportunity — referenced on its Q2 FY2026 earnings call — now has a tangible, non-hyperscaler anchor. For investors in the S&P 500 and NASDAQ, this isn’t just about one stock: it’s a signal that U.S. semiconductor leadership is shifting from pure-play AI to integrated, sovereign, and application-specific silicon — with Broadcom Inc. at the center.

Apple and Broadcom have a long history together, and this new phase of our partnership further accelerates our commitment to American manufacturing and innovation.— Tim Cook, CEO of Apple

Related Coverage: Can a major Apple deal lock in Broadcom’s future growth even as AVGO stock slides on Wall Street nerves? Broadcom Apple Partnership: AVGO Falls 2.1% on Deal News explores how market sentiment diverged from fundamentals just one day before the full financial details emerged — a reminder that short-term volatility often obscures long-term strategic wins.