Can Tesla Robotaxi expansion and smarter FSD features outweigh investor doubts as the stock slides on bigger AI expectations?

What’s Driving Tesla Robotaxi Expansion?

Tesla Robotaxi operations are now live in Miami — a strategic leap beyond Austin and Dallas — according to The Information. Unlike earlier limited pilots, this rollout follows a new ‘scaling fast’ blueprint designed for rapid geographic replication. Tesla has planned additional Florida launches this summer, targeting high-density urban corridors with strong infrastructure support. Crucially, the Miami service remains geofenced — covering only select neighborhoods — underscoring the cautious, iterative approach regulators demand. Still, the expansion signals accelerating real-world validation: Electrek reports Tesla now operates over 20 unsupervised robotaxis across its three-state footprint, up from just 14 in Austin last quarter. That’s a 43% increase in fleet capacity — a tangible step toward the capital-light, asset-light model Wall Street increasingly demands.

How Is FSD Voice Control Changing the Game?

Tesla’s Full Self-Driving system is undergoing its most consequential upgrade since V12: natural-language voice control powered by Grok. Ashok Elluswamy, Tesla’s vice president of AI software, confirmed on X that the team is actively developing neighborhood-level navigation commands — such as ‘It’s the white house on the left, just past that SUV’ — enabling FSD to interpret contextual cues like driveways, storefronts, and parked vehicles. This isn’t just convenience: it solves the critical ‘last 100 feet’ problem that has stalled adoption of supervised autonomy. With Elon Musk targeting a September rollout, the feature could materially improve user engagement and retention — especially as FSD active subscriptions hit 1.28 million, up 51% year over year. For investors, this represents a direct path to recurring revenue: higher FSD usage drives stronger data flywheel effects, improving model accuracy and widening Tesla’s AI moat against rivals like Apple and NVIDIA.

Why Is the Model Y L Launch Not Moving the Stock?

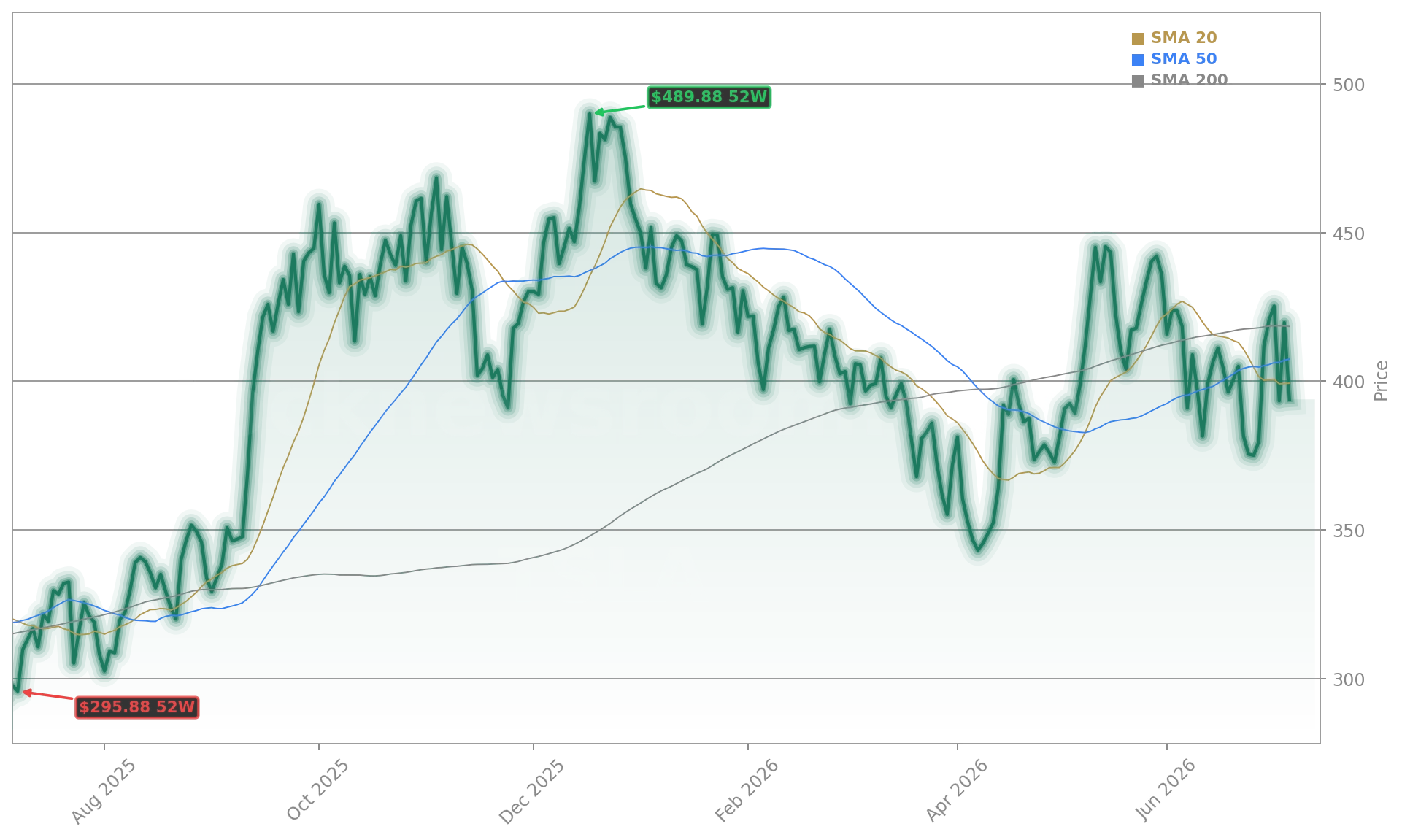

Tesla’s new three-row, six-seat Model Y L — now in U.S. production — should boost average selling price and family-market penetration. At $62,000, it sits $4,000 above the Model Y Performance, yet remains $23,000 below the base Model X. Yet the stock fell 2.74% to $392.94 on Wednesday — down 10% year to date — because Wall Street no longer trades Tesla on vehicle volume alone. The S&P 500’s consumer discretionary sector is under pressure, and Tesla’s 382x trailing P/E reflects pure optionality on AI and robotics, not hardware margins. As Barron’s noted, ‘Robo-taxis and robots will move the stock more than EVs in the coming months.’ That sentiment is reinforced by prediction markets, which assign just a 10.5% probability to California robotaxi launch by year-end — a stark contrast to Tesla’s aggressive capital allocation: $25 billion in 2026 CapEx, pushing free cash flow negative despite $22.39 billion in Q1 revenue.

How Do Analysts View the Q2 Catalyst?

Working on it.— Ashok Elluswamy, Tesla Vice President of AI Software

With Q2 earnings just two weeks away, analyst positioning is tightening. Citigroup maintains a ‘Neutral’ rating on Tesla but raised its price target to $425, citing ‘accelerated FSD monetization visibility and robotaxi unit economics nearing inflection.’ RBC Capital Markets upgraded Tesla to ‘Outperform,’ highlighting ‘compelling margin upside in energy storage and FSD subscription ARPU growth.’ However, Morgan Stanley warns that ‘continued AI capex without near-term revenue visibility could pressure sentiment,’ especially if guidance implies further dilution from stock-based compensation — which totaled $2.8 billion in FY2025. The divergence underscores Tesla’s dual identity: a profitable automaker trading like a pre-revenue AI startup. For NASDAQ investors, that volatility is structural — not temporary.