Can Coinbase survive a brutal crypto downturn long enough for its subscription pivot to change the market’s mind?

What’s Driving the Coinbase Crypto Crash?

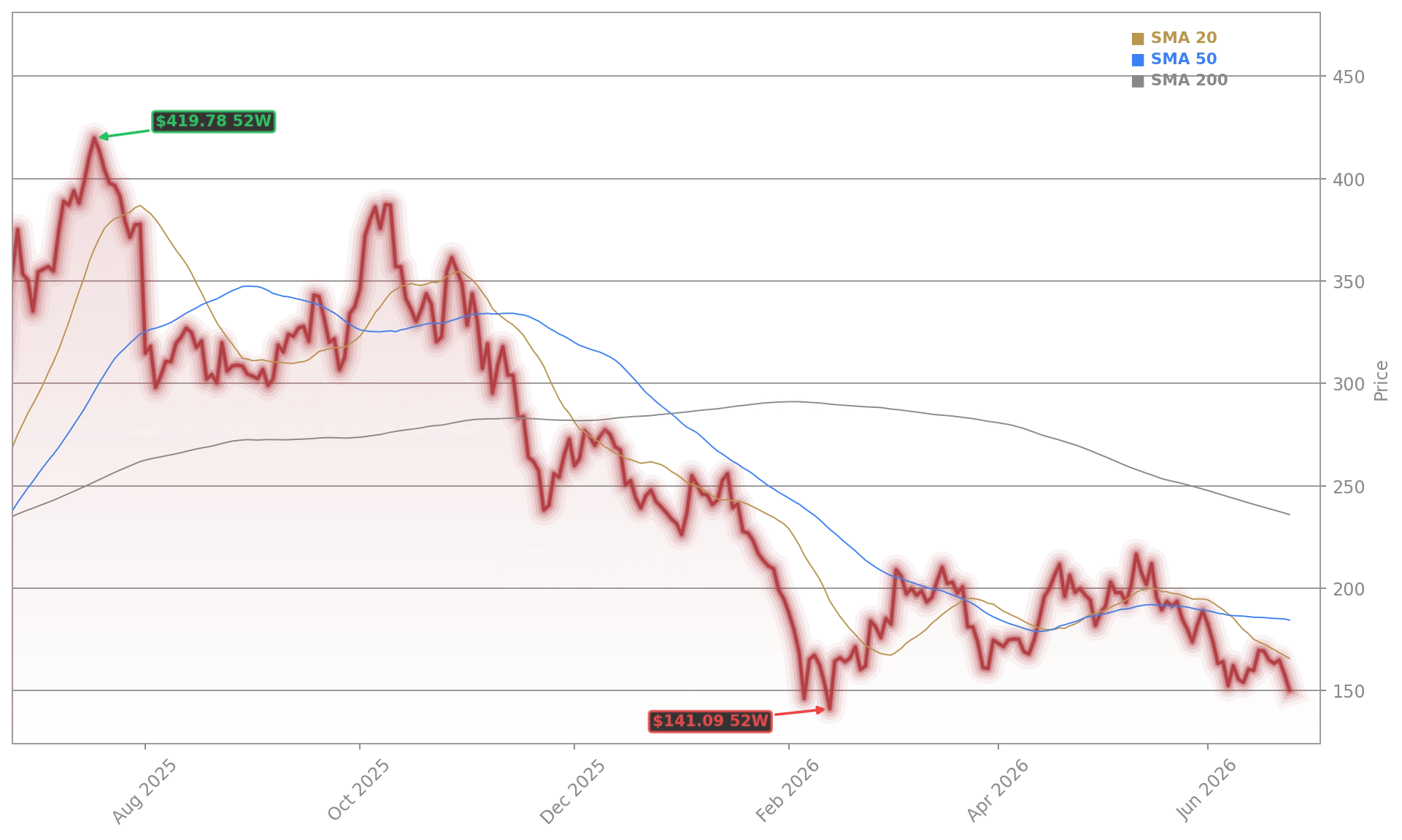

Bitcoin’s 32% year-to-date decline — and 53% drop from its October 2025 intraday high — has triggered a cascade across digital asset equities. On Wednesday alone, Coinbase Global, Inc. fell 4.3%, Robinhood Markets slid 5.2%, and Bitcoin miners MARA and Riot Platforms dropped 5.9% and 4.5%, respectively. The Coinbase Crypto Crash isn’t isolated: it mirrors a broader rotation out of speculative assets, including AI chip stocks like NVIDIA, as macro uncertainty and rising bond yields erode risk appetite. Notably, Bitcoin’s 52-week intraday low coincided with a 0.4% rise in the Dow Jones Industrial Average — underscoring its increasing divergence from traditional market leadership.

How Bad Is COIN’s Q1 2026 Earnings Damage?

Released May 7, 2026, Coinbase Global, Inc.’s Q1 results revealed a sharp contraction: $1.41 billion in revenue, down 30.5% year over year and 4.7% below consensus. EPS landed at -$1.49 — a $1.53 miss — driven entirely by $482.4 million in non-cash markdowns on crypto held for investment. Adjusted EBITDA remained positive at $303.3 million, marking the 13th straight quarter of profitability. Still, transaction revenue — historically the company’s most volatile line — fell sharply as total crypto market cap and trading volumes both declined over 20% quarter over quarter. In response, management announced a 14% headcount reduction targeting $500 million in annualized savings.

Can Subscription Revenue Save COIN From Crypto Volatility?

Yes — and that’s the core of the bull case. Subscription and services revenue now accounts for 44% of net revenue, up from 29% in Q1 2025. Stablecoin revenue hit $305 million in Q1, buoyed by USDC’s $80 billion market cap in March. Prediction markets crossed $100 million annualized within two months of launch; retail derivatives are on track for a $250 million run rate. This structural shift matters: subscription revenue has a beta of just 0.4 to Bitcoin, versus 3.32 for the overall stock. As 24/7 Wall St. notes, this ‘durability’ is the factor tipping their scale — and why their $271.94 target implies 64.97% upside from $164.84.

How Does COIN Stack Up Against Crypto Peers?

While Coinbase Global, Inc. fell 4.3% Wednesday, MicroStrategy (MSTR) dropped 9% to $94.43 after bouncing off a 27-month low — a sign of mounting liquidity pressure that our recent analysis flagged. Robinhood’s 5.2% decline highlights its continued exposure to crypto-driven transaction revenue, unlike Coinbase Global, Inc.’s diversified services stack. Meanwhile, Coinbase Global, Inc. is expanding beyond crypto: its pre-IPO platform now includes OpenAI and Anthropic offerings, positioning it as a broader digital brokerage — a move echoing Interactive Brokers and Robinhood, but with deeper on-chain integration. That ambition is visible in its $211 billion in notional volume from 20x futures on stock-index bundles since July 2025.

What’s the Path to Recovery?

Stabilization above $60,000 in Bitcoin is critical — and BlackRock’s recent recommendation of 1–2% portfolio allocation to Bitcoin adds institutional credibility. The $13.5 million CIMG stock offering paid entirely in Bitcoin signals growing corporate adoption, while Hyperscale Data’s $45.9 million Bitcoin treasury underscores balance sheet resilience. Yet risks remain: insider net selling across 90 recent transactions, a forward P/E of 77, and regulatory uncertainty under the GENIUS Act. Still, with $10.21 billion in cash and $2.10 billion in remaining buyback authorization, Coinbase Global, Inc. has dry powder to defend value — and execute its ‘Everything Exchange’ vision.

Related coverage: Coinbase Global, Inc.’s tokenization push is accelerating Wall Street’s on-chain shift — though legacy exchanges and custodians are preparing countermeasures, as detailed in our June 19 analysis. Meanwhile, MicroStrategy’s liquidity strain — now at $1.2 billion — is intensifying the STRC-MSTR feedback loop, as explored in our June 24 report.

Coinbase Global, Inc. remains a high-beta play on crypto recovery — but its subscription pivot is real and accelerating. For investors, the Coinbase Crypto Crash may be the last major test before the next cycle. The next quarterly earnings will show whether Q2 transaction revenue meets management’s $215 million May 5 pace — and whether stablecoin and prediction-market growth can sustain momentum. Long-term investors should watch for continued execution on its Everything Exchange strategy and regulatory clarity under the GENIUS Act framework.

Our 24/7 Wall St. price target is $271.94, buy, with 90% confidence. The factor tipping the scale is the durability of subscription revenue, which now cushions trading swings far better than during the 2022 cycle.— 24/7 Wall St.

Fazit folgt.