If Deere beat estimates again, why did investors punish the stock so aggressively after earnings?

Why are Deere Earnings pressuring the stock?

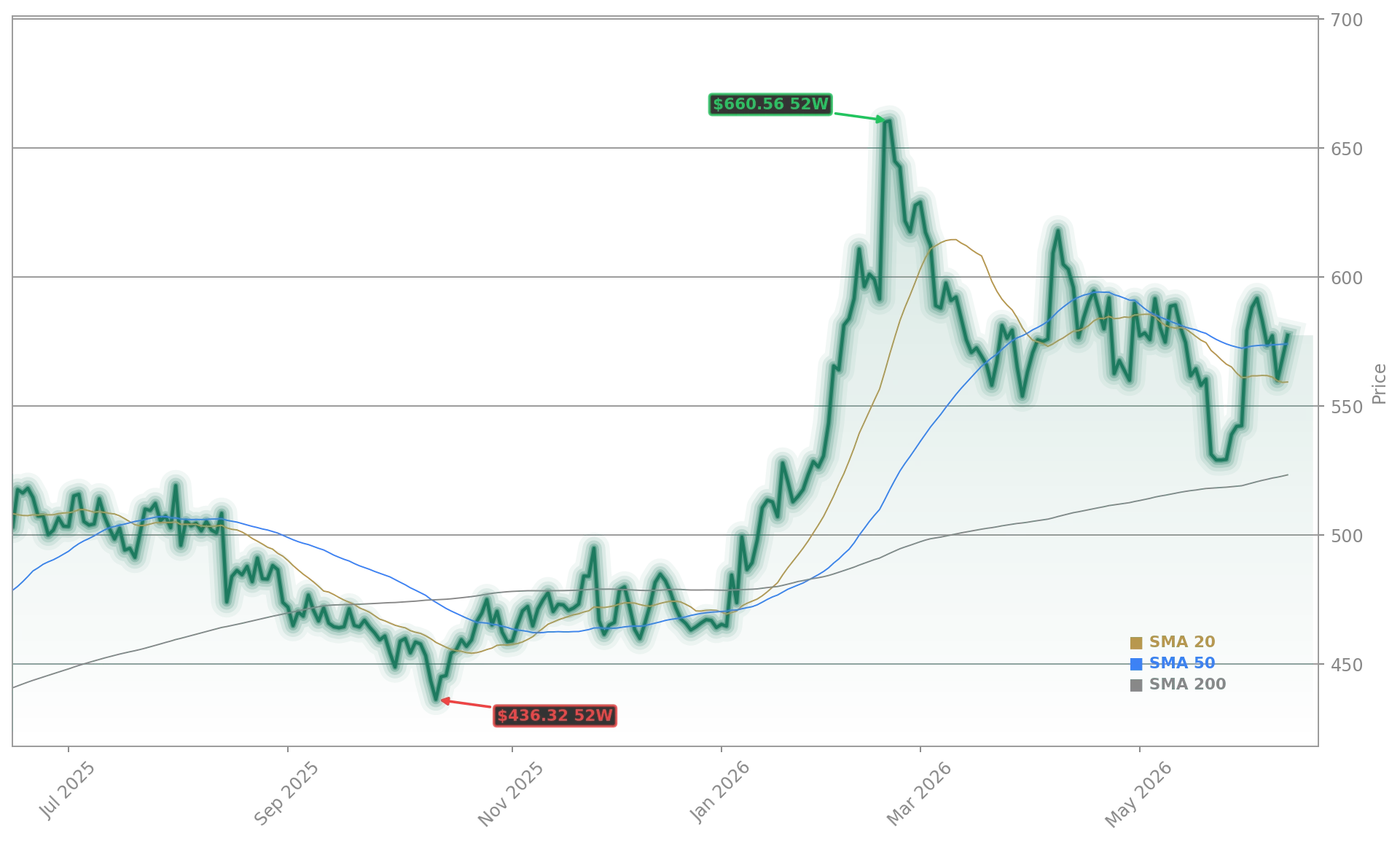

Deere & Company reported fiscal second-quarter net income of $1.77 billion, or $6.55 a share, on net sales and revenue of $13.37 billion. Both figures came in ahead of consensus expectations, with analysts looking for roughly $5.70 per share and revenue closer to $12.73 billion. Even so, shares fell sharply intraday to $518.67, down 7.40% from the previous close of $560.46.

The market reaction suggests investors wanted more than a beat. Deere left its fiscal 2026 net income guide at $4.5 billion to $5.0 billion, rather than raising it after the strong quarter. That stood out because the company had lifted guidance after its prior report in February, helping fuel a major rally at the time. Now, Wall Street appears worried that the next two quarters could remain subdued as farmers delay large equipment purchases.

How did Deere perform across businesses?

The biggest drag remained Production & Precision Ag, where sales fell 14% to $4.50 billion and operating profit came in at $706 million. Farmers are still holding back on expensive machinery as crop prices remain under pressure relative to recent peaks, while fertilizer, fuel, and financing costs stay elevated. Deere continues to expect full-year sales in that segment to decline 5% to 10%.

Elsewhere, the story was much stronger. Small Ag & Turf sales jumped 16% to $3.49 billion, with an operating margin of 20.6%. Construction & Forestry sales surged 29% to $3.79 billion, and Deere raised its full-year sales outlook for that unit to up 20%, from a prior expectation of up 15%. That construction strength reflects infrastructure spending, roadbuilding demand, and heavy activity tied to data centers.

The quarter also benefited from a $272 million tariff refund recovery, which supported margins. Management said total tariff exposure for the year remains around $1.2 billion, or roughly a 3% margin headwind, with net tariff costs now seen near $900 million after refunds.

What are Deere and rivals signaling now?

The latest Deere Earnings call made clear that management still sees 2026 as the bottom of the agricultural cycle, with a recovery more likely in 2027. New and used inventory trends have improved, especially in North American large ag equipment, and fleet age is rising, which should eventually support replacement demand. Deere also pointed to precision agriculture momentum, expanding See & Spray adoption, and satellite connectivity through Starlink.

That technology angle matters as Deere competes not just with farm-equipment makers such as AGCO and CNH Industrial, but increasingly for investor attention against automation leaders like NVIDIA and industrial digitization plays tied to AI. Deere’s precision strategy, software upsell opportunity, and connectivity push also fit a broader market theme that has benefited companies such as Tesla and Apple when recurring revenue becomes more visible.

On valuation and sentiment, Barron’s noted before the open that Deere traded at a premium multiple to AGCO and CNH Industrial. That premium may now be harder to defend if farm demand remains soft. No fresh analyst rating changes from firms such as Citigroup, RBC Capital Markets, Goldman Sachs, or Morgan Stanley were disclosed in the earnings materials, so the market is trading mainly on guidance and management commentary.

Related Coverage: Investors may want to compare Thursday’s muted reaction with Deere’s previous earnings surge. In Deere Quarter with +11.6% Rally: Record Forecast Provides Boost, we looked at how a stronger outlook in February drove a sharp upside move. That earlier setup highlights why today’s unchanged forecast is carrying more weight than the headline beat in these Deere Earnings.

Deere Earnings delivered a clear beat, but Wall Street is focused on what management did not do: raise the full-year outlook. For investors, the near-term setup now depends on whether construction momentum and precision ag adoption can offset another few quarters of weak large-farm demand. The next update will be crucial in showing whether Deere can turn an earnings beat back into stock momentum.

As we address ongoing challenges within global agricultural markets, our comprehensive portfolio continues to drive market share expansion and support our targets for sustained growth.— John May

Fazit folgt.