Is Michael Burry spotting a regulatory winner in sports betting before the rest of Wall Street catches on?

Why Did DraftKings Burry Enter Now?

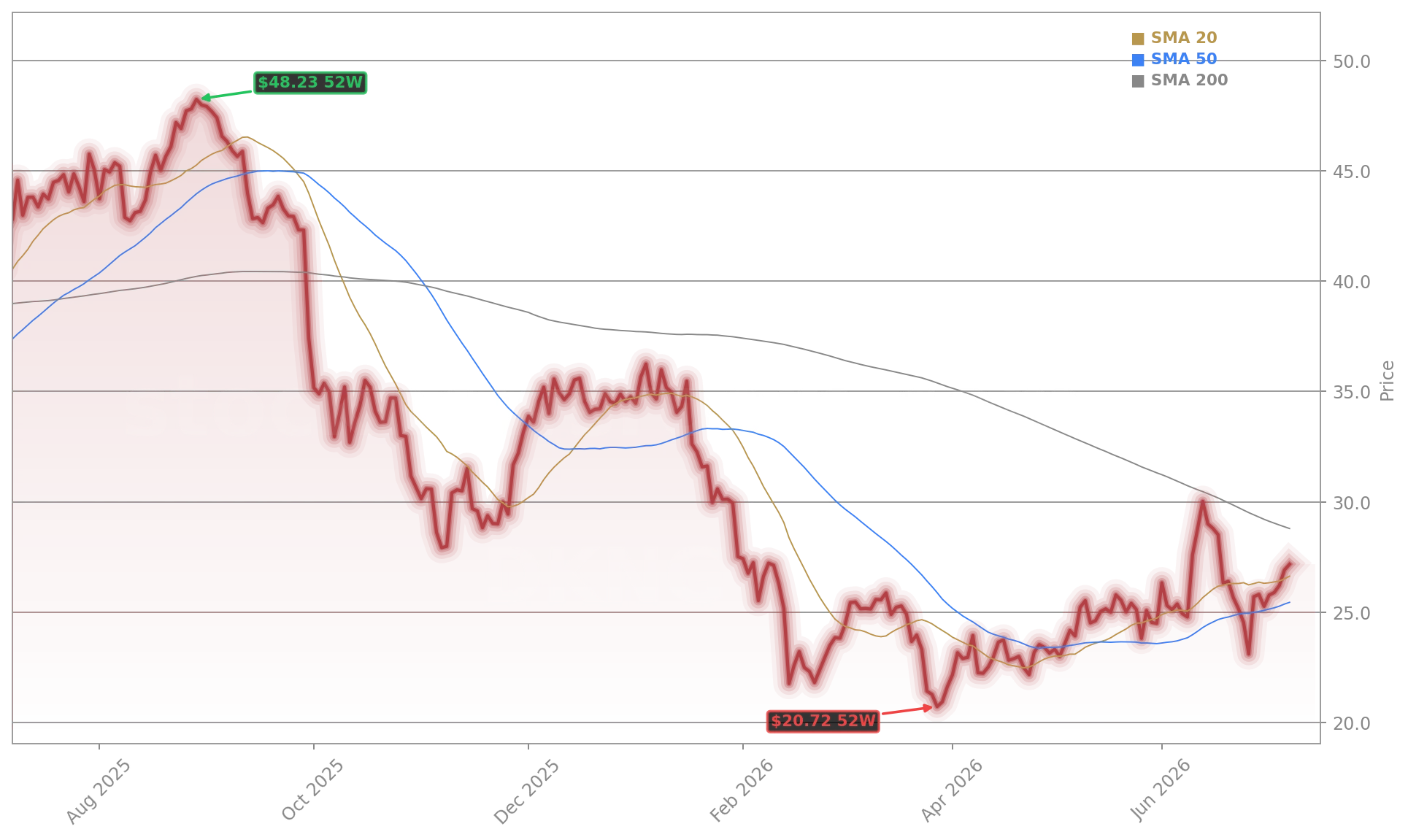

Michael Burry’s recent substack post, widely cited by CNBC and Bloomberg, confirms he purchased DraftKings Inc. shares in the low $26 range — near current levels — as part of a broader $200M+ commitment to regulated U.S. sports betting. His 60/40 split between Flutter Entertainment and DraftKings Inc. reflects confidence in both companies’ scale and path to positive free cash flow. Crucially, Burry sees DraftKings Burry’s timing as aligned with a broader market consolidation: customer acquisition costs are falling, promotional spend is down 22% year-over-year, and Q1 2026 marked the company’s first GAAP net profit ($21.1M), a stark reversal from a $33.9M loss in Q1 2025. This inflection point matters deeply for Wall Street, where investors are increasingly rewarding cash generation over top-line growth — especially in the overvalued segments of the NASDAQ.

How Does DraftKings Burry Compare to Flutter?

While Burry’s position is split, his commentary distinguishes the two operators. He calls Flutter ‘a fundamentally very good operating business with terrific scale’ — referencing its FanDuel dominance and global reach — but flags past capital misallocation. In contrast, he describes DraftKings Inc. as ‘inflecting as an operating business,’ highlighting its U.S.-only focus, stronger iGaming margins, and faster path to EBITDA positivity. That divergence matters for U.S. portfolios: DraftKings Inc. has outperformed Flutter by 12% YTD despite both being down sharply from 52-week highs — a sign institutional investors may be pricing in earlier U.S. regulatory clarity for DraftKings Inc. Citigroup recently reiterated its ‘Buy’ rating on DKNG with a $34 price target, citing improved marketing efficiency and market-share stability versus peers like Apple-backed Caesars and Tesla-adjacent betting integrations.

What’s the Threat From Prediction Markets?

Burry isn’t bullish on DraftKings Inc. in isolation — he’s bearish on its unregulated competitors. He explicitly warns that prediction markets like Kalshi and Polymarket ‘exist in a loophole adjacent to a heavily regulated and taxed industry’ and will ultimately be ‘subsumed into regulation and taxation.’ His view aligns with recent action: the U.S. Commodity Futures Trading Commission proposed new derivatives oversight rules in June 2026, and multiple state attorneys general have launched probes into offshore crypto-based platforms. That regulatory tailwind could accelerate DraftKings Inc.’s transition from land-grab to profit leader — especially as both DraftKings Inc. and Flutter begin rolling out their own compliant prediction-market products. For S&P 500 investors, this isn’t just about DKNG — it’s about the broader re-rating of regulated digital consumer platforms versus speculative, unlicensed alternatives.

Is DraftKings Burry a Signal for the Broader Sector?

Yes — and it’s already resonating. While DraftKings Inc. rose 2.56% on Wednesday, the broader gambling ETF (BETZ) gained 1.8%, outpacing the NASDAQ’s 0.7% gain. RBC Capital Markets upgraded the sector to ‘Overweight’ last week, citing ‘a clear pivot toward profitability and lower regulatory risk.’ Meanwhile, DraftKings Burry’s move stands in sharp contrast to recent insider activity: director Levin Woodrow sold $880K worth of shares in May, and CFO Erik Bradbury sold $22K under a pre-arranged 10b5-1 plan. That divergence — institutional conviction versus routine insider liquidity — underscores why Wall Street is watching DraftKings Burry so closely. With FMR LLC holding 1.9% of DKNG and Q1 2026 cash flow up 41% year-over-year, the fundamentals are aligning with Burry’s thesis — and that’s rare in today’s volatile tech-adjacent sectors.

Related Coverage: DraftKings’ prediction-market ambitions face mounting pressure as Meta’s AI-powered betting integrations gain traction, while Tesla’s robotaxi expansion stumbles amid rising AI expectations — highlighting how adjacent tech narratives impact investor sentiment in high-beta consumer platforms. Meanwhile, DraftKings Inc.’s full stock profile offers real-time metrics, analyst consensus, and earnings history for deeper due diligence.

DraftKings Burry represents more than a single stock call — it’s a macro bet on regulatory clarity, capital discipline, and the re-emergence of cash flow as the dominant valuation driver in post-AI hype markets. For U.S. investors, the DraftKings Burry position signals that the risk-reward calculus has shifted decisively toward regulated, scaled operators. The next quarterly earnings will test whether that inflection translates into sustained margin expansion — and whether Wall Street follows Burry into the fold.

DraftKings is inflecting as an operating business and the value is in the transition I foresee in the near future.— Michael Burry

Fazit folgt.