Can Medicare coverage and faster FDA plant approvals turn Eli Lilly’s obesity franchise into an even bigger profit machine?

What Does Medicare Coverage Mean for Eli Lilly Medicare Obesity?

Beginning Wednesday, Medicare Part D plans must cover GLP-1-based obesity treatments—including Eli Lilly and Company’s Zepbound (tirzepatide) and Foundayo (oral tirzepatide)—at a $50 copay. This marks the first time obesity drugs have been broadly covered under Medicare, a program serving over 65 million Americans. With an estimated 15–20 million beneficiaries qualifying based on BMI and comorbidity criteria, the program represents the single largest near-term patient-access inflection for the obesity drug class. Eli Lilly currently holds ~60% U.S. market share in obesity GLP-1s, ahead of Novo Nordisk’s ~39%, per Q2 2026 data. While Zepbound’s KwikPen formulation is prioritized in the Medicare program for ease of administration, Foundayo’s April 2026 launch adds a key oral alternative—particularly attractive to seniors wary of injections. The $299–$699 monthly list price has been effectively neutralized by the $50 copay, dramatically lowering the barrier to entry for older adults.

How Is Eli Lilly Scaling to Meet Demand?

Supply constraints have been the primary bottleneck limiting GLP-1 adoption—and Eli Lilly is now accelerating manufacturing capacity with unprecedented regulatory support. On June 30, the FDA announced Eli Lilly and Company as one of seven companies selected for its PreCheck Pilot Program, a two-phase initiative designed to cut new facility review timelines by up to 14 months. Under PreCheck, regulators engage during construction—rather than after completion—enabling faster validation of sites producing tirzepatide APIs and finished doses. This is critical: Eli Lilly’s current Zepbound capacity remains tight, and the Medicare launch could add 2–3 million new prescriptions annually. The PreCheck designation complements recent expansions in Indianapolis and Ireland, and signals confidence from U.S. regulators in Lilly’s quality infrastructure. Competitors including Novo Nordisk and Johnson & Johnson are also scaling, but Eli Lilly’s dual advantage—market leadership plus FDA manufacturing acceleration—gives it a structural edge.

What’s the Impact on Eli Lilly’s Global Strategy?

Beyond U.S. Medicare, Eli Lilly and Company is executing a dual-track international expansion—most notably with a newly announced commercialization agreement with Innovent Biologics for Verzenios in mainland China. Under the deal, Innovent handles distribution and marketing of the CDK4/6 inhibitor for HR+/HER2− breast cancer, while Eli Lilly retains manufacturing and R&D control. Verzenios has been on China’s National Reimbursement Drug List since 2021 and was renewed in 2025—ensuring broad patient access. This partnership leverages Innovent’s deep oncology commercial network while freeing Eli Lilly to prioritize GLP-1 capacity. The move also diversifies revenue beyond the U.S. obesity market, where Eli Lilly Medicare Obesity is now the dominant catalyst. Notably, Eli Lilly’s Q2 2026 earnings—released last week—showed obesity franchise revenue up 142% year-over-year to $4.1 billion, accounting for 37% of total pharmaceutical sales.

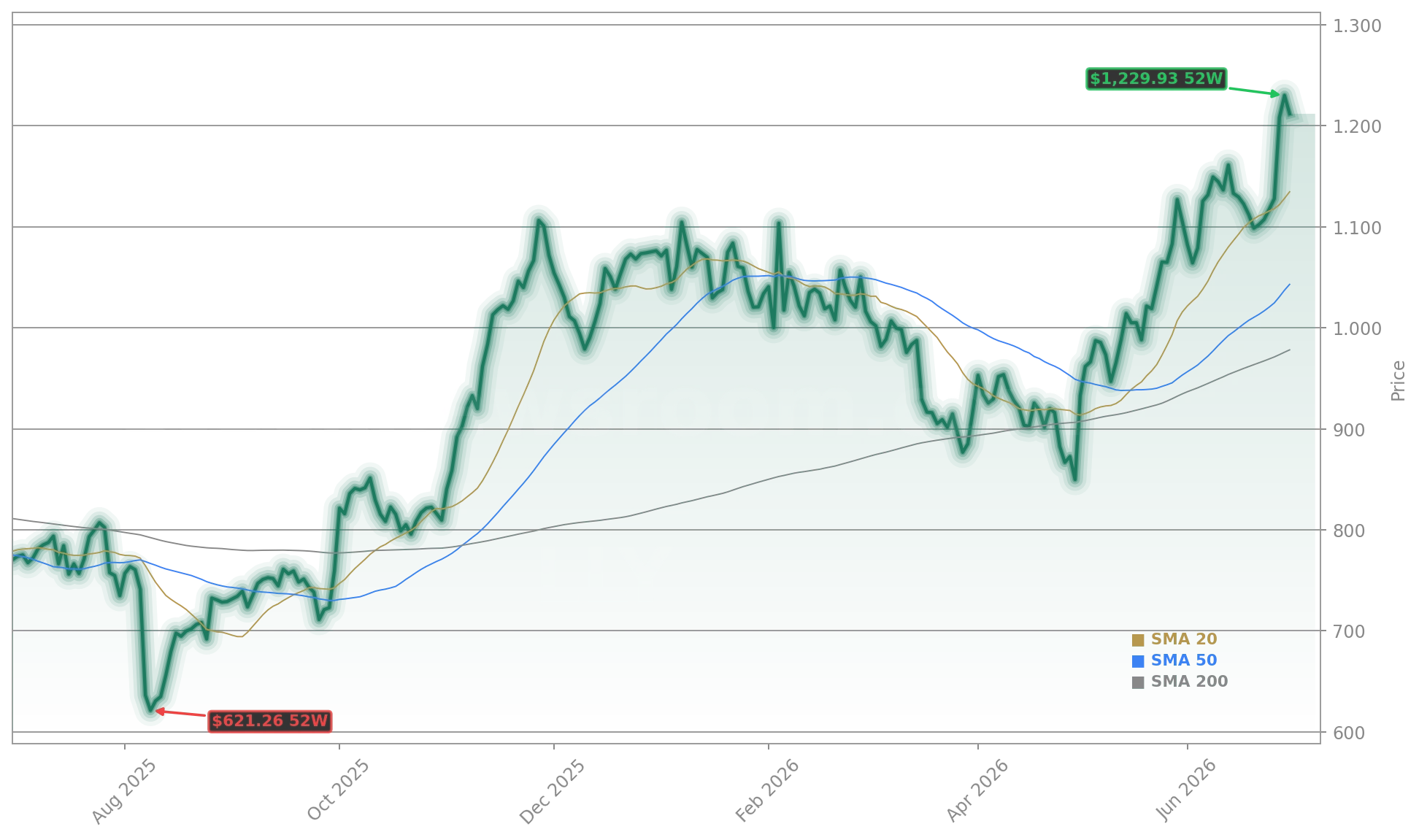

How Are Analysts Reacting to the Medicare Catalyst?

Wall Street is upgrading its outlook on Eli Lilly and Company with growing conviction. Citigroup raised its price target to $1,325, citing ‘Medicare-driven volume acceleration and pricing resilience.’ Morgan Stanley upgraded the stock to ‘Overweight,’ emphasizing ‘the structural shift in payer coverage as a multi-year tailwind.’ RBC Capital Markets maintained its ‘Outperform’ rating and increased its 2027 EPS forecast by 8%, factoring in 1.8 million new Medicare Zepbound prescriptions by year-end. Meanwhile, the stock trades at $1,209.60—within 2.3% of its 52-week high of $1,238.00—reflecting strong institutional demand. Eli Lilly Medicare Obesity has become the central narrative in healthcare sector positioning, with the company now the largest holding in the Fidelity MSCI Health Care Index ETF (FHLC), at 3.85% weight.

What’s Next for Eli Lilly and the Obesity Market?

Medicare’s launch is just the beginning: CMS will evaluate clinical outcomes and cost offsets over the next 12–18 months, with potential for expansion into Medicare Advantage plans and broader private payer adoption. Eli Lilly and Company is also advancing next-gen obesity candidates—including dual GIP/GLP-1 agonists and oral small molecules—while investing $8.2 billion in R&D for 2026. With Verzenios scaling in China and PreCheck accelerating U.S. manufacturing, Eli Lilly is building a diversified, globally resilient growth engine. The convergence of policy, capacity, and pipeline makes Eli Lilly Medicare Obesity not just a quarterly catalyst—but a structural investment theme for the next decade.

Related Coverage: Eli Lilly’s record $1 trillion market cap reflects its dominance in the GLP-1 boom—Eli Lilly Record at $1 Trillion as GLP-1 Boom Lifts LLY. Meanwhile, Pfizer’s recent lung cancer trial setback underscores the high stakes in oncology—Pfizer Lung Cancer Trial Sends Warning on Oncology Pivot.

From my perspective, both companies are treating this very intentionally and seriously as an opportunity for access.— Ilya Yuffa, President of Lilly USA and Global Customer Capabilities

Eli Lilly Medicare Obesity is now the cornerstone of the company’s growth story. For investors, this isn’t just about Q2 earnings—it’s about a paradigm shift in chronic disease coverage that lifts the entire healthcare sector. The next catalyst will be Q3 prescription data, expected in mid-August, which will confirm whether Medicare uptake meets Wall Street’s aggressive forecasts. For long-term portfolios, Eli Lilly and Company remains a core healthcare holding with unmatched execution capability and policy tailwinds.