Is the new Federal Reserve Rate Policy quietly rewriting the rules for credit, stocks and crypto over the next few years?

How is Federal Reserve Rate Policy changing?

After more than 15 years of aggressive quantitative easing that held yields down and inflated asset valuations, the **Federal Reserve** is pivoting toward a structurally tighter stance. A new Fed chair is expected to prioritize shrinking the central bank’s multi-trillion-dollar balance sheet, reversing years in which the Fed was a dominant buyer of Treasuries and mortgage-backed securities. That move, together with a decision to keep policy rates on hold through 2026, implies higher term premiums and a reset for long-term interest rates across the curve.

Fed officials have become increasingly vocal that inflation risks still dominate. Recent minutes from the Federal Open Market Committee (FOMC) and comments from Chair Jerome Powell underscore growing concern that price pressures, amplified by an energy shock tied to conflict in the Middle East, could stay above the 2% target longer than previously anticipated. As a result, Federal Reserve Rate Policy is now firmly biased toward patience: no near-term cuts, a slower path back to lower borrowing costs and a focus on ensuring long-run inflation expectations remain anchored.

At the same time, Powell has stressed that the labor market, while cooling, remains resilient, with unemployment near 4.3%. That gives the Fed room to wait and watch how oil prices and geopolitical risks filter through to core inflation, even if growth slows. For investors, the message is clear: the era of reflexive Fed easing at the first sign of trouble is over.

What does this mean for credit and refinancing?

The shift in Federal Reserve Rate Policy is particularly critical for corporate borrowers that gorged on cheap debt during the pandemic. Many loans and bonds issued when the policy rate was near zero and the Fed was an indiscriminate buyer will need to be refinanced in a fundamentally different environment. Market participants are already looking ahead to a sizable refinancing wave around 2028 in the private credit space, where sponsors may face meaningfully higher coupons and tighter lending standards.

While credit costs eased off their late-2024 peaks, spreads remain sensitive to every Fed communication. RBC Wealth Management expects the Fed to leave rates unchanged for the rest of the year, citing persistent inflation risk and the added uncertainty from elevated energy prices. Pilar Gomez-Bravo of MFS also argues that central banks, having been burned by underestimating inflation in 2022, will be slower to cut this time precisely because starting policy rates are much higher than during the COVID shock.

For U.S. banks and asset managers, the end of QE and balance sheet runoff will likely translate into steeper yield curves but also more volatile funding conditions. Highly indebted sectors, including parts of commercial real estate and leveraged software companies tied to AI spending themes around NVIDIA and other high-growth names, could face higher refinancing risk if spreads widen into the 2028 maturity wall.

How are Wall Street and mega caps reacting?

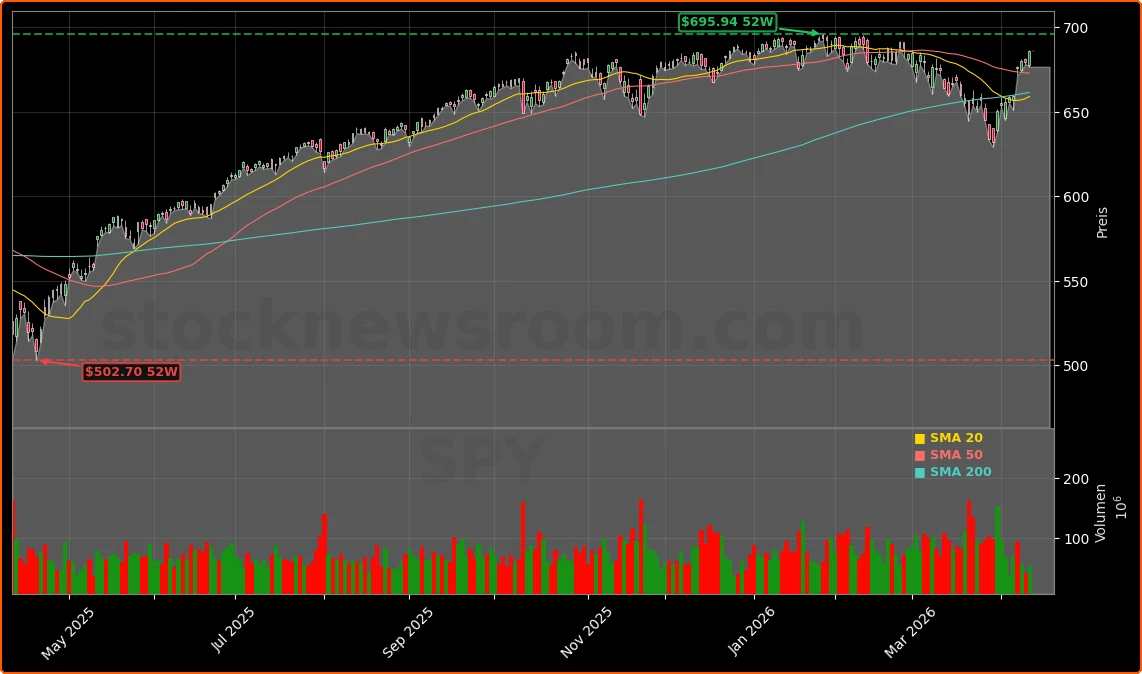

Despite the hawkish overhang from Federal Reserve Rate Policy, risk appetite on Wall Street has remained resilient. The S&P 500 recently traded around 6,886, up about 1% on the day, with megacap growth stocks such as Apple and Tesla continuing to attract capital on the view that strong balance sheets and secular growth can withstand higher-for-longer rates. For these cash-rich giants, elevated yields can even be a competitive advantage as weaker rivals struggle to refinance.

Yet the broader fixed income market must reassess inflation risk. The earlier assumption that slowing growth would quickly deliver multiple rate cuts has been unwound; fed funds futures now price no move for an extended period, with the first 25 basis point cut pushed out and only a shallow easing path beyond that. Paul Skinner of Wellington Management expects the Fed to sit in the middle of the global policy spectrum, doing less than the European Central Bank or Bank of England on both hikes and cuts, constrained in part by a U.S. debt load that has climbed from roughly 80% to around 120% of GDP.

With fiscal space limited and the Fed reluctant to ease, investors may see higher real yields as a semi-permanent feature rather than a cyclical blip. Portfolio positioning is shifting toward quality: investment-grade credit, profitable tech leaders such as NVIDIA and Apple, and sectors with pricing power that can navigate sticky inflation.

Why does this matter for Bitcoin and crypto?

The crypto market is also being repriced under the new Federal Reserve Rate Policy regime. Bitcoin, up more than 5% over the last 24 hours and still the largest digital asset by market cap, has benefited for years from the assumption that any growth scare would trigger swift Fed easing and a renewed liquidity wave into speculative assets. An oil-driven inflation shock complicates that narrative.

Elevated policy rates directly raise the cost of leverage for hedge funds, market makers, miners and retail traders operating on margin. A firmer dollar and higher real yields make non-yielding, volatile assets less attractive at the margin. Treasury Secretary Scott Bessent recently urged the Fed to adopt a “wait and see” stance on cuts as war-related inflation clouds the outlook, reinforcing market expectations that cheaper money is not imminent.

Powell has downplayed systemic risk in the private credit sector, including funds that have exposure to software and AI-linked firms, but refinancing pressures and tighter financial conditions still matter for crypto businesses seeking capital. High living and borrowing costs also shrink disposable income, limiting the ability of retail investors to consistently dollar-cost-average into Bitcoin or altcoins. That makes future rallies more dependent on organic spot demand, ETF flows and institutional adoption rather than broad macro liquidity.

At the same time, the end of QE and a long pause in rate cuts could support Bitcoin’s “hard money” narrative for some investors concerned about fiscal sustainability. The tug-of-war between that story and the drag from high real yields will likely define crypto performance in the coming quarters.

The risk in the private credit sector is probably not systemic, but higher-for-longer rates will still be a demanding test for leveraged business models.— Jerome Powell (paraphrased)

In summary, Federal Reserve Rate Policy is transitioning from an era of abundant liquidity and rapid easing to one of balance sheet shrinkage and extended stability at higher levels. For U.S. investors, that means more expensive credit, a challenging refinancing backdrop into 2028 and a less supportive environment for highly leveraged trades in both traditional and digital assets. The next phase of this cycle will test which business models, from Tesla to crypto miners, can thrive without the safety net of an ultra-dovish Fed.