Can blockbuster JPMorgan Earnings and record trading revenue outweigh a trimmed rate-income outlook and Jamie Dimon’s growing macro warnings?

How did JPMorgan Earnings beat Wall Street?

JPMorgan Chase & Co. opened the second day of big-bank earnings with a robust Q1 2026 print. Net income rose to $16.5 billion, up about 13% year over year, translating into earnings per share of $5.94. That topped consensus forecasts around $5.45 and marked a roughly 17% jump versus the prior-year EPS. Revenue climbed about 10% to roughly $50.5 billion, also ahead of expectations near $49.2 billion, as both Wall Street and Main Street businesses pulled their weight.

The beat was broad-based. Net interest income (NII), supported by higher loan balances and still-elevated rates, rose even as deposit mix shifted toward higher-yielding products. At the same time, noninterest revenue surged thanks to a powerful rebound in trading and investment banking fees. Return on equity remained in the low‑20s, reflecting the bank’s continued ability to convert scale into profitability despite heavier regulation and technology spend.

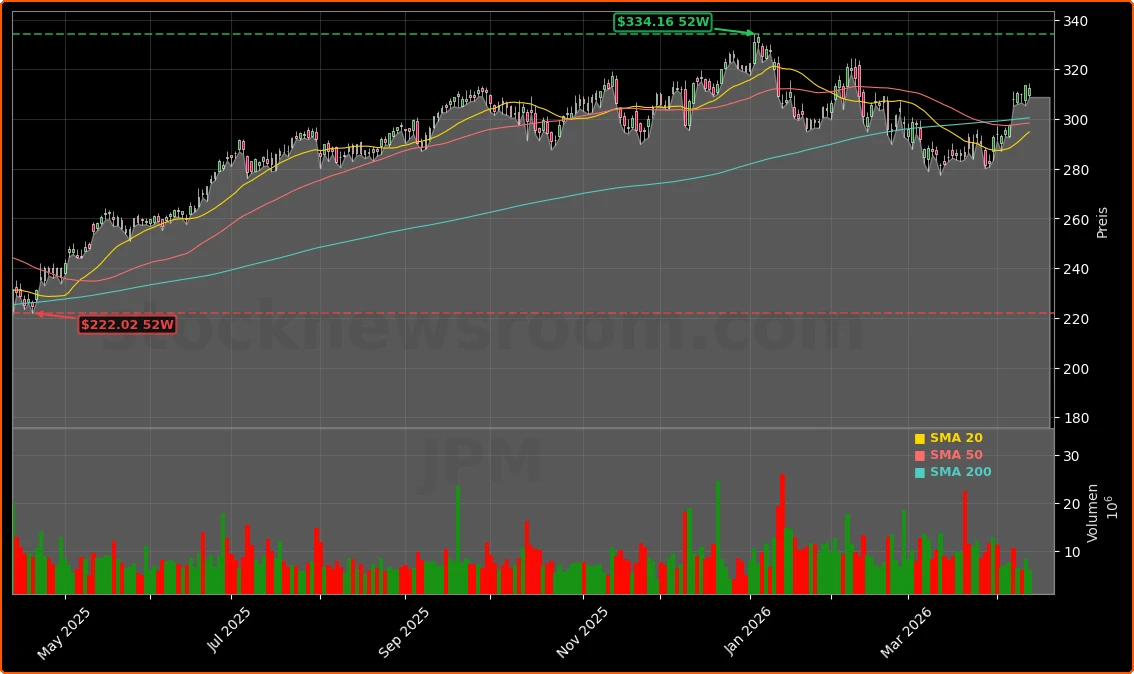

Still, JPMorgan shares recently traded around $312, down roughly 0.5% on the day and off pre‑market levels, suggesting that strong JPMorgan Earnings were largely priced in after a strong run-up into the print.

Why did JPMorgan trim its rate income outlook?

The main wrinkle in an otherwise stellar quarter was a modest downgrade to the full‑year NII outlook. Management now expects total 2026 net interest income of about $103 billion versus prior guidance of $104.5 billion. The reduction reflects lower anticipated contribution from markets-related NII as interest-rate dynamics shift and some of last year’s rate-driven windfalls normalize.

Importantly, JPMorgan held steady on its guidance for NII excluding markets at roughly $95 billion, signaling that the core consumer and commercial lending engines remain intact. CFO Jeremy Barnum emphasized that the change is driven more by market rates and technical factors than by deterioration in underlying demand or credit quality. Even so, the tweak was enough to trigger a classic “buy the rumor, sell the news” response after strong JPMorgan Earnings had raised the bar.

Barclays reiterated its “Buy” rating on the stock following the release, noting the strength of the franchise but flagging the lowered NII guidance and CEO Jamie Dimon’s macro caution as reasons why valuation expansion may remain measured in the near term.

What drove record trading and deal fees at JPMorgan?

The standout story inside the JPMorgan Earnings report was Wall Street activity. Markets revenue hit a record $11.6 billion, jumping about 20% year over year. Fixed income, currencies and commodities trading brought in roughly $7.1 billion, easily beating expectations, while equities trading delivered about $4.5 billion, its best quarter ever.

Market volatility across rates, credit, commodities and equities kept clients active without devolving into the kind of “bad volatility” that freezes liquidity. That backdrop allowed JPMorgan’s traders to capture wider spreads and higher volumes, reinforcing the bank’s position alongside firms like NVIDIA-driven AI beneficiaries as key volatility winners in this market cycle.

Investment banking also roared back. Fees climbed roughly 28% year over year, powered by a resurgence in equity capital markets and an 80%+ jump in advisory revenue as M&A deals that had been delayed late last year finally closed. Management described pipelines as “healthy” across M&A and IPOs, while cautioning that the war in Iran and broader geopolitical tensions could delay some transactions if conditions worsen.

How healthy is the U.S. consumer for JPMorgan?

For U.S. investors, one of the most important signals in the JPMorgan Earnings release is the state of the American consumer. Dimon and Barnum repeatedly stressed that consumers are “still earning and spending” and that the labor market remains the key support for strong credit performance. In Consumer & Community Banking, revenue rose about 7% to $19.6 billion, with net income around $5 billion.

Card and auto revenues jumped 13%, driven by higher revolving credit card balances and strong auto lease income. Total credit card spend was up about 9% year over year. Delinquencies across consumer products, including mortgages and cards, remain below last year’s levels, and JPMorgan added over 450,000 net new checking accounts in the quarter. Deposits in the consumer segment grew about 2–3%, even as competition from money market funds and high‑yield products stayed intense.

Management acknowledged that higher gas and energy prices are nibbling at households, but noted that such expenses account for only about 3% of the typical customer’s outlays. So far, JPMorgan sees little evidence of consumers “trading down” in a way that would signal a sharp slowdown.

What risks and regulatory pressures did Dimon flag?

Despite blockbuster JPMorgan Earnings, Dimon’s tone on the macro and regulatory environment stayed characteristically sober. He highlighted a “complex set of risks” including wars in the Middle East, volatile energy prices, large U.S. fiscal deficits, and elevated asset valuations. While he does not see private credit as a systemic threat, he warned that the next credit cycle is likely to be “worse than people expect” in some pockets.

On the regulatory front, Barnum and Dimon sharply criticized elements of the proposed Basel III endgame and higher G‑SIB surcharges, estimating that JPMorgan’s required CET1 capital could rise by about 4% under current proposals. They argued this could make some low‑risk, market‑making activities in U.S. capital markets uneconomic and ultimately raise borrowing costs for households and businesses. RBC Capital Markets’ Gerard Cassidy and other analysts pressed management on how these rules might constrain balance‑sheet growth, especially in the markets franchise.

Even so, JPMorgan ended Q1 with a standardized CET1 ratio of roughly 14.3%, far above minimums, after returning around $4.1 billion in common dividends and $8.1 billion in buybacks over the past twelve months.

How does JPMorgan compare with peers for U.S. investors?

For S&P 500 and Dow investors, JPMorgan’s print sets a high bar for other money center banks. Goldman Sachs also delivered a strong quarter in core banking and trading but stumbled in some fixed‑income areas, underscoring JPMorgan’s relative advantage in diversified markets revenue. Wells Fargo and Citigroup reported solid consumer trends but lack JPMorgan’s dominant advisory and trading franchises.

On Wall Street, JPMorgan’s commentary on private credit, AI‑driven investment, and regulatory capital is widely used as a roadmap for peers and for sectors beyond banking, from Apple and other Big Tech names funding massive data centers to EV players like Tesla that depend on capital markets access. The stock now trades slightly below recent highs and under the average analyst price target near the low‑$330s cited by MarketBeat, leaving room for upside if execution remains strong and regulatory overhangs ease.

Related Coverage

Investors looking to dig deeper into the risk side of today’s strong JPMorgan Earnings may want to revisit earlier concerns around the bank’s exposure to nonbank lenders. An in‑depth feature titled “JPMorgan Private Credit Risk -2.6% Warning for Wall Street” explores whether recent moves in private credit are a routine adjustment or a signal for a crowded $2 trillion market, and today’s management comments suggest those risks remain contained but closely monitored. For a broader sector view, Citi’s restructuring remains a key theme: “Citigroup Strategic Shift Warning as Global Focus Resets” examines whether the bank’s global reset is unlocking value or just the latest twist in a long turnaround story, giving context to how rivals are repositioning as JPMorgan doubles down on its universal-bank model.

While the U.S. economy remains resilient today, an increasingly complex set of risks — from geopolitics to fiscal deficits and elevated asset prices — means we must be prepared for a wide range of outcomes.— Jamie Dimon, Chairman and CEO, JPMorgan Chase & Co.

Overall, JPMorgan Earnings confirm the bank’s status as the bellwether of U.S. finance: record trading and resurgent deal-making are offsetting a plateau in rate-driven income, leaving the franchise well positioned even as macro and regulatory risks build. For long‑term investors, the combination of strong capital, consistent profitability and a cautious but opportunity‑focused outlook keeps the stock firmly on the shortlist of core financial holdings, with the next quarter’s results set to show whether the momentum in markets and investment banking can continue.