Is Goldman Sachs seeing the first real crack in the AI chip trade, or just the next rotation opportunity?

Why Is Goldman Sachs AI Strategy Shifting Away From Chips?

Goldman Sachs Group, Inc. is urging portfolio managers to rotate out of semiconductor stocks amid mounting evidence of cyclicality and leverage-driven swings. Christian Mueller-Glissmann, managing director and Head of Asset Allocation Research at Goldman Sachs, told Bloomberg Television that chipmakers are ‘incredibly cyclical companies’ with outsized exposure to derivatives and ETF flows—making them prone to sharp reversals. While companies like NVIDIA powered much of the NASDAQ’s 2025–2026 rally, Mueller-Glissmann emphasized that their valuation multiples and positioning now carry elevated risk. The firm’s latest asset allocation framework recommends trimming exposure to chipmakers and reallocating toward hyperscalers—cloud infrastructure leaders with more stable, recurring AI-related revenue streams.

What Does This Mean for Hyperscalers?

The Goldman Sachs AI Strategy pivot elevates the strategic role of hyperscalers—including Meta, Apple, and Microsoft—as primary beneficiaries of long-term AI infrastructure buildout. Unlike chipmakers, whose earnings swing with memory pricing, foundry utilization, and export controls, hyperscalers control both the hardware deployment and software monetization layers. Goldman Sachs notes that capital expenditures by these firms have surged 42% year-over-year in Q2 2026, with AI-driven cloud investments now accounting for nearly 65% of total capex. This structural advantage, combined with pricing power and balance sheet strength, makes them more resilient during market corrections. Morgan Stanley recently reiterated its ‘Overweight’ rating on Meta, citing ‘unmatched AI deployment velocity,’ while RBC Capital Markets upgraded Apple to ‘Outperform’ on its on-device AI roadmap.

How Is Goldman Sachs Group, Inc. Performing Financially?

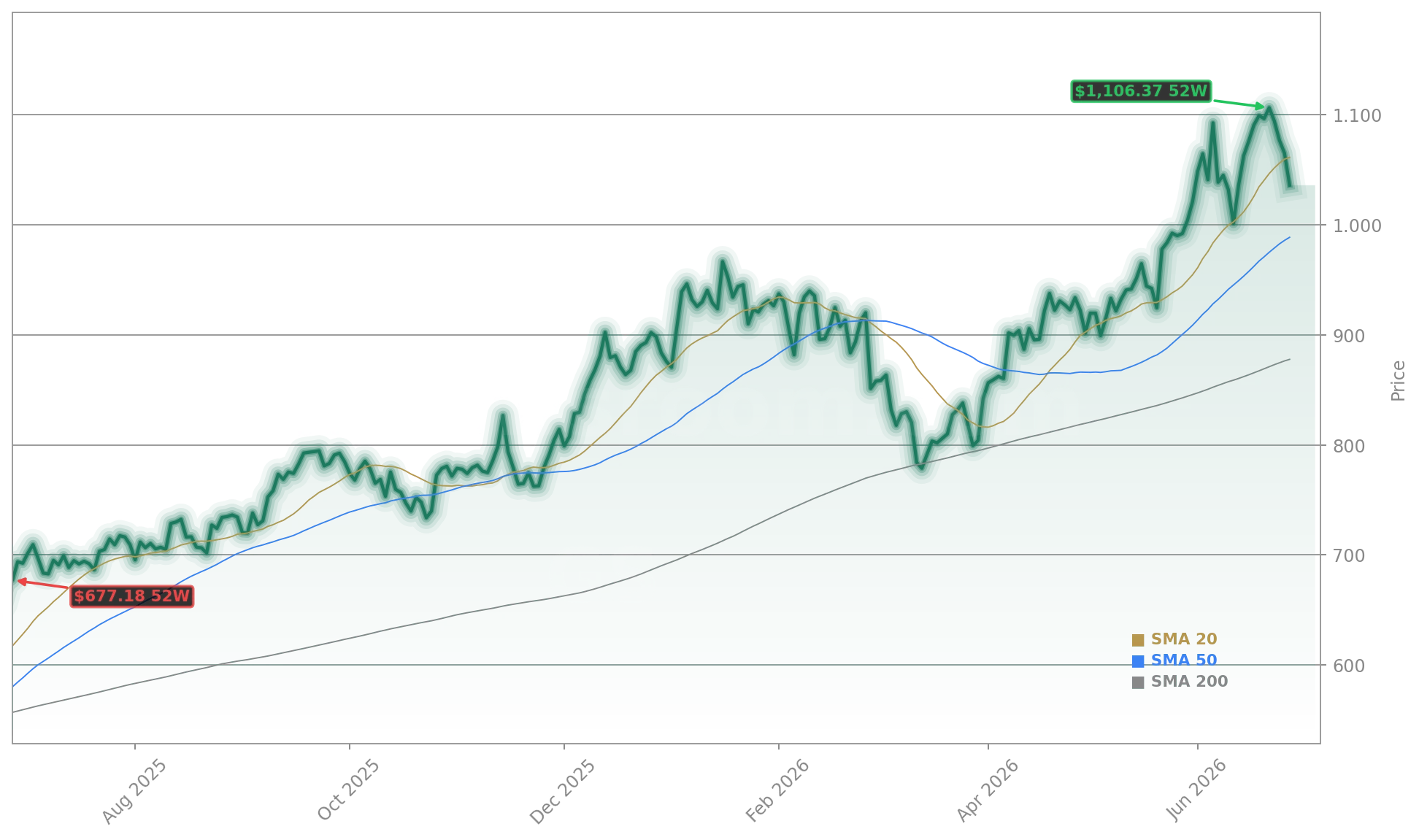

Goldman Sachs Group, Inc. reported Q2 2026 earnings that beat consensus estimates, driven by record investment banking fees and robust trading revenue. The firm posted $12.4 billion in net revenue and $4.2 billion in net income, up 9% year-over-year. Its investment banking division generated $3.1 billion—fueled by a 120% surge in IPO-related fees—while equities trading revenue rose 14%. Crucially, Goldman Sachs passed the Federal Reserve’s 2026 stress test with ‘flying colors,’ clearing it to raise its dividend to $5.00 per share, up from $4.75. Despite a 3.74% intraday decline on Friday, June 26, the stock remains up 18% year-to-date—outperforming the S&P 500’s 13% gain and the NYSE Financial Index’s 11% rise.

Is the IPO Boom Sustainable?

Goldman Sachs Group, Inc. helped lead 23 of the 50 U.S. IPOs completed in 2026—a pace double that of 2025 and matching the full-year 2021 record by dollar value ($120 billion). Yet Ben Snider, Goldman Sachs’ chief U.S. equity strategist, cautions against equating volume with euphoria. ‘Although the dollar volume is quite elevated, although we’re seeing an acceleration in activity, to me it still looks like we’re a far cry from that level of euphoric sentiment we saw in those episodes,’ he said on the bank’s Exchanges podcast. Crypto-focused listings from Payward, Ledger, and Grayscale have paused, underscoring selective investor caution. The firm’s analysis shows U.S. IPOs remain well below dot-com (nearly 400 in 1999) and pandemic-era (250+ in 2021) peaks—suggesting room for continued, measured expansion.

What’s Driving the Broader Market Rotation?

These are incredibly cyclical companies. So to some extent, it could make sense to diversify a bit away from them.— Christian Mueller-Glissmann, Goldman Sachs Head of Asset Allocation Research

Goldman Sachs’ latest risk appetite indicator has risen to its highest level since early 2025—driven first by AI capex and now by geopolitical stabilization, including the reopening of the Strait of Hormuz. Mueller-Glissmann describes the current environment as a ‘Goldilocks spectrum’: inflation expectations are falling, earnings growth remains solid, and liquidity conditions are supportive. Yet he warns that elevated optimism carries correction risk—especially if AI earnings disappoint or chip demand falters. The firm’s model shows semiconductor positions are now 2.3x more leveraged than the broader tech sector, with option open interest hitting record levels. For U.S. investors, the Goldman Sachs AI Strategy now prioritizes quality, cash flow visibility, and optionality—favoring hyperscalers over chipmakers, and diversified financials over single-sector tech bets.