Can JetBlue Expansion keep lifting the stock, or will fuel costs and debt bring this rally back to earth?

Why Is JetBlue Expansion Accelerating Now?

JetBlue Airways Corporation is doubling down on its Fort Lauderdale hub — a strategic pivot that now includes eight operational nonstop destinations and six more launching in the coming months. New routes span domestic markets like Indianapolis, San Diego, and Columbus, Ohio, and extend internationally to Cali and Barranquilla in Colombia, plus Caracas, Venezuela — marking JetBlue’s first service to the latter since 2019. Daily nonstop flights from Fort Lauderdale to Baltimore, Charlotte, Cleveland, Nashville, Detroit, Houston, Chicago, and Ponce, Puerto Rico, further cement the airport’s role as a growth engine. This JetBlue Expansion is not incremental — it’s infrastructure-led, with gate leases, crew basing, and maintenance investments locked in through 2027. Unlike legacy carriers scaling back in secondary airports, JetBlue is treating Fort Lauderdale as its second core — behind New York — and Wall Street is pricing in market-share gains in the Southeast and Caribbean corridors.

How Does JetBlue Expansion Compare to Peers?

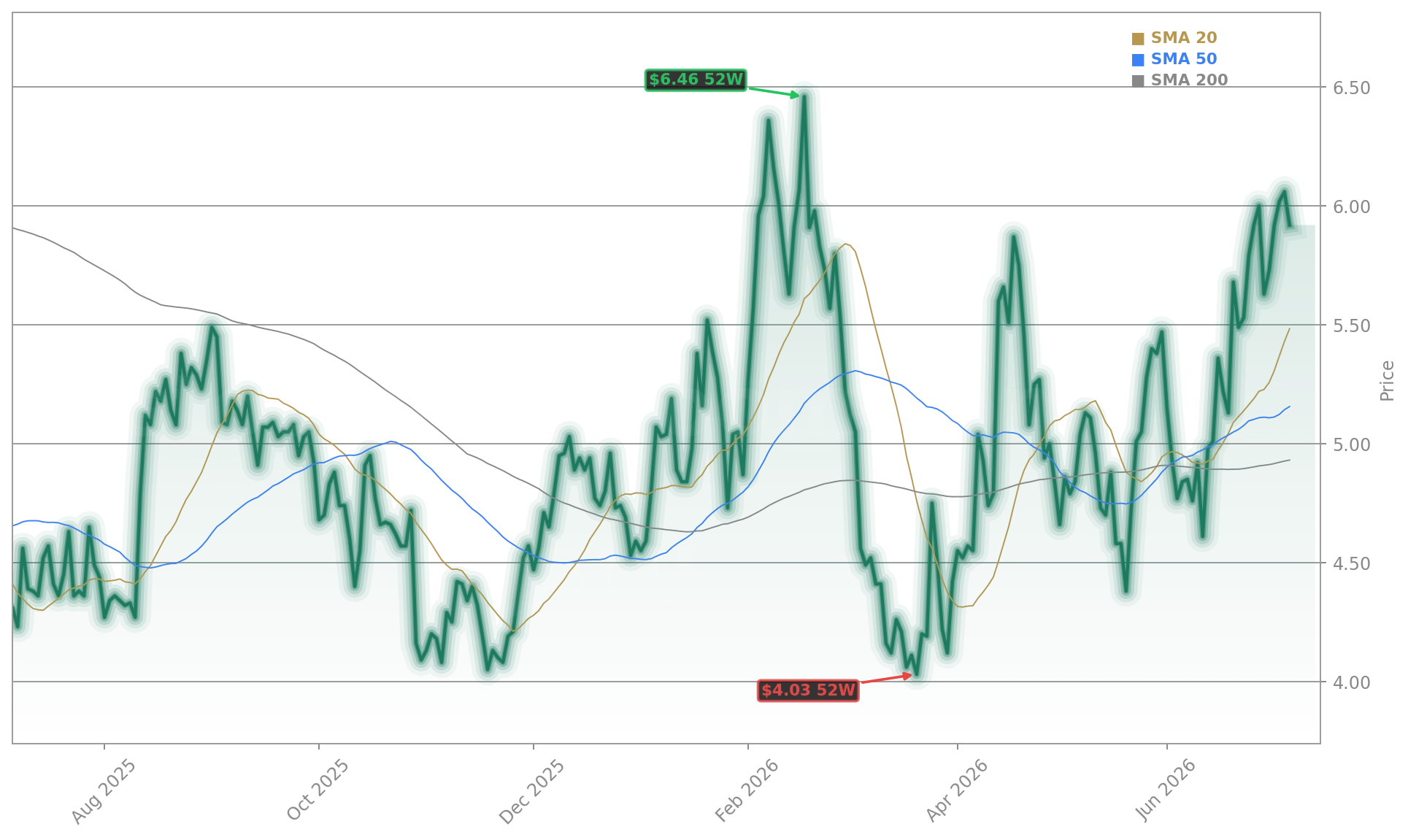

While Delta Air Lines and American Airlines focus on transatlantic and premium international capacity, JetBlue Expansion stands out for its domestic-Latin America adjacency. Southwest Airlines (LUV) has retreated from Fort Lauderdale entirely, and Spirit Airlines (SAVE) faces regulatory pressure on its ultra-low-cost model. JetBlue’s move directly challenges United Airlines’s dominance in Houston and Chicago, and its Colombia routes compete head-to-head with Avianca — now a U.S. bankruptcy case. Analysts at RBC Capital Markets note the expansion is “well-timed to capture pent-up leisure demand in a softening corporate travel environment,” while Citigroup upgraded JBLU to ‘Neutral’ with a $6.35 price target, citing “disciplined capacity growth and improving ancillary yield.” Morgan Stanley maintains an ‘Underweight’ rating but raised its 2026 EBITDA estimate by 4.2% on stronger-than-expected Fort Lauderdale load factors.

What’s the Fuel and Debt Risk for Investors?

JetBlue Expansion doesn’t obscure the balance sheet reality: $8.4 billion in debt and $580 million in projected FY2026 interest expense. Fuel remains the largest variable cost — averaging $2.96 per gallon in Q1, up 15.2% YoY, and guided to $4.13–$4.28 in Q2, a staggering 75% YoY increase. That pressure contributed to Q1 adjusted EPS of −$0.87 versus a consensus of −$0.728 — a 19.5% miss. Yet the market is looking past the near-term squeeze. CEO Joanna Geraghty reaffirmed liquidity and highlighted the JetForward turnaround program, which delivered $305 million in incremental EBIT in 2025 and targets $310 million in 2026. Cumulative savings are now projected at $850–$950 million by 2027, with free cash flow expected to turn positive by year-end 2027. That forward line — not the Q1 miss — is what’s driving the 22.6% YTD gain.

Is JetBlue Expansion Sustainable Amid Rising Rates?

We’re taking decisive actions to manage what is within our control, including adjusting capacity, optimizing revenue, and maintaining disciplined cost control.— Joanna Geraghty, CEO of JetBlue Airways Corporation

With the Federal Reserve holding rates steady but signaling limited near-term cuts, JetBlue’s debt service burden remains elevated. Yet the carrier’s $1.2 billion in unrestricted liquidity — plus $200 million in undrawn credit facilities — provides runway. More importantly, JetBlue Expansion is capital-light: most new routes use existing aircraft, and Fort Lauderdale’s lower gate fees and labor costs improve unit economics versus JFK or Newark. The airline’s ancillary revenue per passenger rose 12.4% YoY in Q1, driven by higher baggage and seat-selection uptake. That’s a key differentiator versus peers like Spirit Airlines and a reason why short interest has fallen 27% over the past 90 days. Insiders have bought shares across 23 transactions — a quiet but telling vote of confidence. And while Polymarket has no active bankruptcy or delisting markets for JetBlue, the absence of such contracts — unlike for Beyond Meat (BYND) or Xerox — signals market consensus on solvency.