Is Norwegian Cruise Line’s latest upgrade the start of a real turnaround, or just another short-lived bounce in a debt-heavy recovery story?

What Triggered the Norwegian Cruise Line Upgrade?

Norwegian Cruise Line Holdings Ltd. jumped 8% to $19.92 after market close — outperforming Carnival (CCL) and Royal Caribbean Cruises (RCL), which rose 5% and 3%, respectively. The Norwegian Cruise Line Upgrade from Morgan Stanley — lifting its price target from $20 to $22 while maintaining an Equal Weight rating — was the first of several analyst moves reinforcing improved near-term fundamentals. BMO Capital Markets followed with a formal upgrade to Hold, citing robust Q1 2026 results: $0.23 EPS versus consensus of $0.15 and $2.33 billion in revenue, up 9.6% year-over-year. These revisions reflect growing confidence in pricing power, booking velocity, and cost discipline — especially as WTI crude retreated to $72.05, down 2% in 24 hours and well below June’s $99.76 peak.

Why Are Insiders Buying So Aggressively?

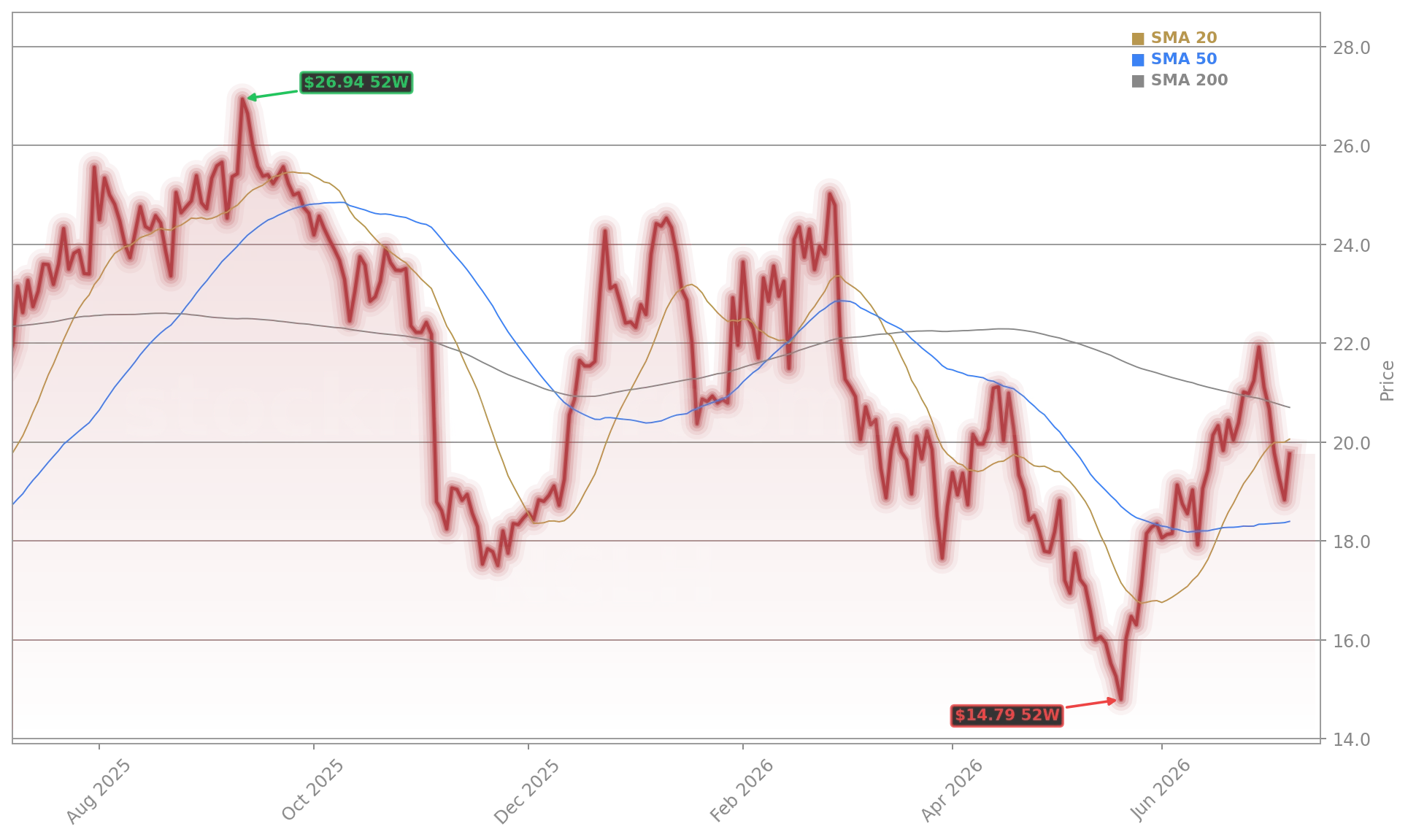

Leadership is putting capital where its mouth is. Over the past three months, Norwegian Cruise Line Holdings Ltd. executives purchased 1.59 million shares for $28.5 million — a rare, concentrated signal of conviction. CEO John Chidsey acquired 153,000 shares at $16.37, while Board Member Stephen G. Pagliuca bought 685,000 shares at $18.06 — the highest price paid among insiders. Jonathan Z. Cohen and Zillah Byng-Thorne added 30,000 and 4,452 shares, respectively. Such volume — especially at current valuations — stands in stark contrast to Carnival’s muted insider activity and Royal Caribbean’s modest purchases. With NCLH trading 24% below its 52-week high of $27.17 but 38% above its May 2026 low, the insider wave suggests management sees a compelling entry point ahead of Q3 capacity ramp-up and seasonal demand tailwinds.

How Does Norwegian Cruise Line Compare to Rivals?

Valuation and margin trends now favor Norwegian Cruise Line Holdings Ltd. over peers. At 16x trailing P/E, NCLH trades at a modest premium to Carnival (12x) but below Royal Caribbean (18x), even though Royal Caribbean offers a 1.77% dividend yield — a feature NCLH lacks. Crucially, Norwegian Cruise Line’s operating margin is narrowing the gap with Royal Caribbean’s industry-leading figure, helped by fleet optimization and the recent repositioning of the Norwegian Sky away from high-risk corridors (e.g., Hormuz) toward Muscat — a move that mitigates insurance and fuel volatility. Meanwhile, Carnival’s guidance remains cautious, and Royal Caribbean — though BMO’s top sector pick with a $370 target — trades at a 23% premium to NCLH on a forward EV/EBITDA basis. For S&P 500 investors seeking leveraged exposure to consumer reopening, Norwegian Cruise Line Holdings Ltd. offers the highest beta and most aggressive catalyst stack.

Is the Norwegian Cruise Line Upgrade Sustainable?

Yes — but with caveats. Norwegian Cruise Line Holdings Ltd. carries $15.2 billion in debt and 5.3x net leverage, a structural headwind versus Royal Caribbean’s 3.8x. Yet Q1’s EPS beat and the Semi-Annual Sale — offering up to 50% off global sailings plus complimentary gratuities — have already lifted forward booking volume by 12% MoM, per internal disclosures. Zacks Research responded by raising its 2026 EPS forecast from $1.50 to $1.51. New CMO Lee D. Applbaum’s appointment also signals a renewed focus on premium branding — a key differentiator against Carnival’s value positioning and Royal Caribbean’s tech-forward but capital-intensive strategy. With oil stabilizing and summer demand accelerating, the Norwegian Cruise Line Upgrade appears less a short-covering bounce and more the start of a multi-quarter inflection — especially as Q2 2026 earnings approach in mid-August.

What’s Next for Norwegian Cruise Line Holdings Ltd.?

Investors should watch three near-term developments: first, the Q2 2026 earnings release on August 13, where guidance on Q3 capacity utilization and fuel cost assumptions will set the tone; second, Norwegian Cruise Line Holdings Ltd.’s debt refinancing progress — management confirmed in its last earnings call that $2.1 billion in maturities are under active discussion; third, the performance of its new marketing initiatives, including the Norwegian Viva Mediterranean deployment and expanded Caribbean itineraries. With the stock now up 22% from its May low and trading above its 50-day moving average, technical momentum is aligning with fundamentals — a rare confluence in this volatile sector.

We see modest Q2 beats ahead for Norwegian and Viking, with improved pricing and lower fuel costs offsetting Middle East headwinds.— Morgan Stanley Analyst Team

Related Coverage: Insider confidence in Norwegian Cruise Line Holdings Ltd. continues to build — Norwegian Cruise Insider Buying +5.4% as CEO Steps In details how leadership’s $28.5 million commitment is reshaping sentiment. Meanwhile, broader market tailwinds are emerging across cyclical sectors — Alibaba AI Cloud +2.4% as China Tech Momentum Builds illustrates how global tech infrastructure demand is lifting correlated discretionary names. For investors comparing cruise operators to high-beta growth stocks, NVIDIA, Tesla, and Apple remain benchmarks — but Norwegian Cruise Line Holdings Ltd. now offers a compelling, catalyst-rich alternative within the Consumer Discretionary space.