Is the Lam Research CEO signaling caution, or is this sharp sell-off simply a valuation reset in the AI memory trade?

Why did Lam Research CEO file a Form 144?

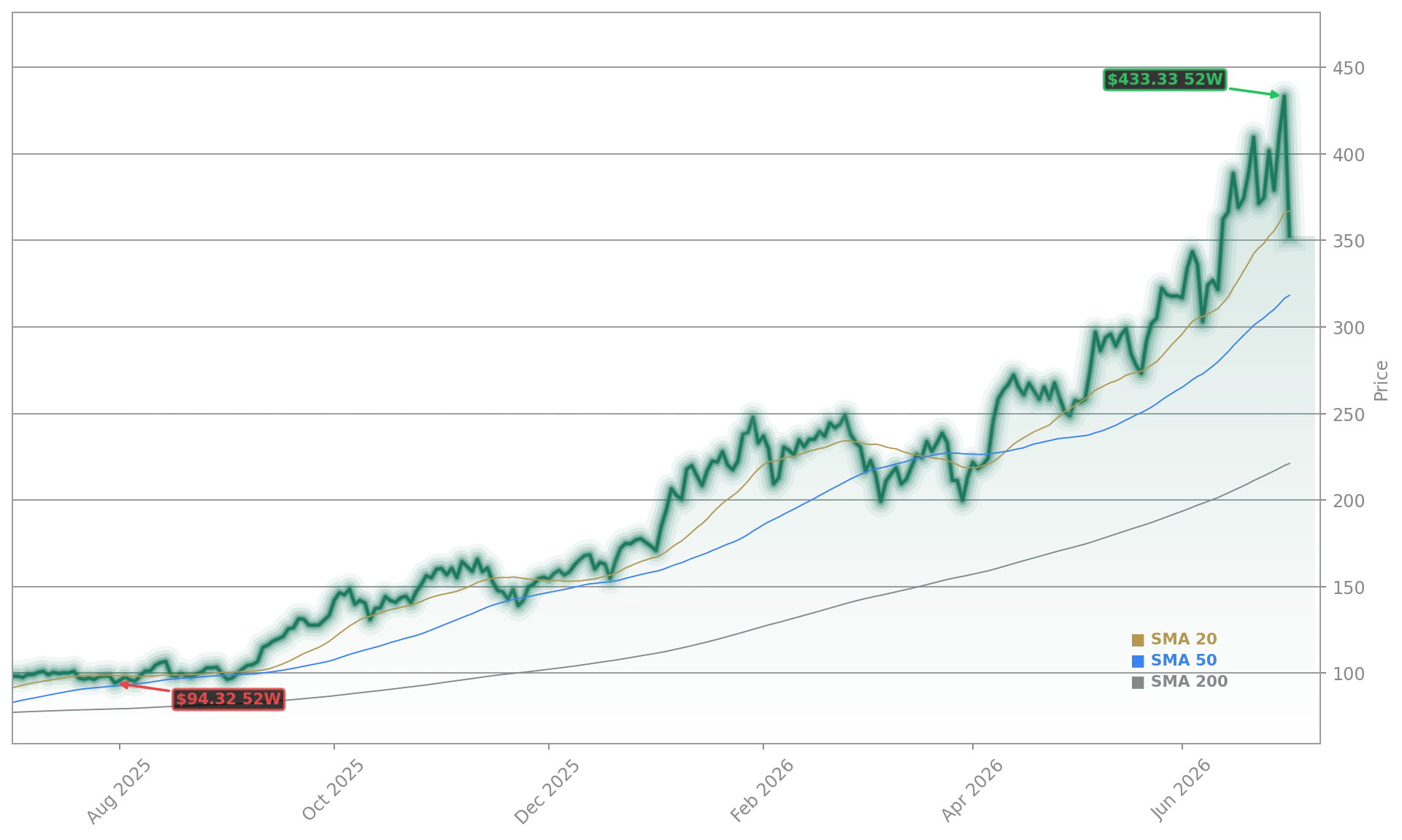

Timothy Archer, Chief Executive Officer of Lam Research Corporation, registered a Form 144 with the SEC on July 2, 2026, disclosing intent to sell 30,000 restricted shares. The filing — processed via Fidelity Brokerage Services — permits sales within 90 days and is consistent with pre-arranged trading plans, though its timing coincides with peak volatility. Lam Research Corporation shares plunged 11.5% intraday on July 1 — the largest single-day drop since early 2025 — and closed down 2.41% the following day. The stock now trades nearly 20% below its all-time high, though still up 153.6% year-to-date. While insider sales are routine, this action from the Lam Research CEO has intensified focus on valuation sustainability amid surging memory capex.

Is the AI memory boom still intact?

Yes — but sentiment has cooled. Global memory equipment investments are projected to reach $52 billion in 2026, up 29% year-over-year, driven by insatiable demand for DRAM and 3D-NAND in AI data centers. Micron Technology (MU) delivered blowout fiscal Q3 results on June 24, lifting Lam Research Corporation shares 7% the same day. Micron’s guidance confirmed memory supply deficits will persist through 2030, with SK Hynix estimating a 20% wafer supply-demand gap. Lam Research Corporation supplies etch and deposition tools to all three major memory makers — Samsung, SK Hynix, and Micron — and derives 39% of revenue from memory equipment. Yet recent Korean chip stock selloffs and reports of potential capex moderation at Meta have triggered profit-taking across the semiconductor equipment sector.

How does Lam Research compare to peers?

Lam Research Corporation trades at a forward P/E of 55 — elevated but not anomalous in the AI infrastructure cohort. NVIDIA (NVDA), though up only 7.42% year-to-date, commands a forward P/E near 68. Applied Materials (AMAT) trades at 32x, while KLA Corporation (KLAC) trades at 41x. Citigroup recently raised its price target on Lam Research Corporation to $410, citing “unmatched exposure to AI-driven memory expansion.” RBC Capital Markets maintains an ‘Outperform’ rating and highlights Lam’s 54% foundry equipment revenue as a diversifier against memory cyclicality. Still, Morgan Stanley notes that “valuation headroom is narrowing” as the stock’s 2026 revenue growth (25% YoY) begins to price in 2027–2028 acceleration.

What’s next for Lam Research Corporation’s earnings?

Fiscal Q4 2026 guidance calls for $6.6 billion in revenue and EPS of $1.50–$1.80 — implying full-year EPS of $6.40–$6.70. Analysts project $9.91 EPS by fiscal 2028. That implies 20% annual EPS growth, supported by sustained memory capex and expanding foundry demand from Apple and Tesla suppliers. Lam Research Corporation’s dividend remains modest — $0.26 per share — but the company has raised it annually for 14 straight years. With $4.2 billion in cash and no long-term debt, balance sheet flexibility remains a key strength. The company’s China exposure — ~33% of revenue — introduces geopolitical risk, though recent U.S. export license adjustments have eased near-term supply chain friction.

Related Coverage

We remain confident in our long-term roadmap and the structural demand drivers across memory and logic. Our Q4 guidance reflects disciplined execution amid a dynamic environment.— Timothy Archer, CEO of Lam Research Corporation

For deeper context on Lam Research Corporation’s AI-driven valuation thesis, Lam Research Forecast: $400 Target Signals AI Capex Boom analyzes how $400 price targets hinge on memory wafer output growth and U.S. CHIPS Act disbursements. Meanwhile, Qualcomm Acquisitions -3.7% as AI Pivot Faces Scrutiny offers a cross-sector lens on how semiconductor leaders are reallocating R&D toward AI software — a trend that indirectly boosts demand for Lam Research Corporation’s advanced process control tools.