Did the Lam Research CEO sell at exactly the wrong moment for investors—or exactly the right moment for himself?

Why Did Lam Research CEO Act at the Peak?

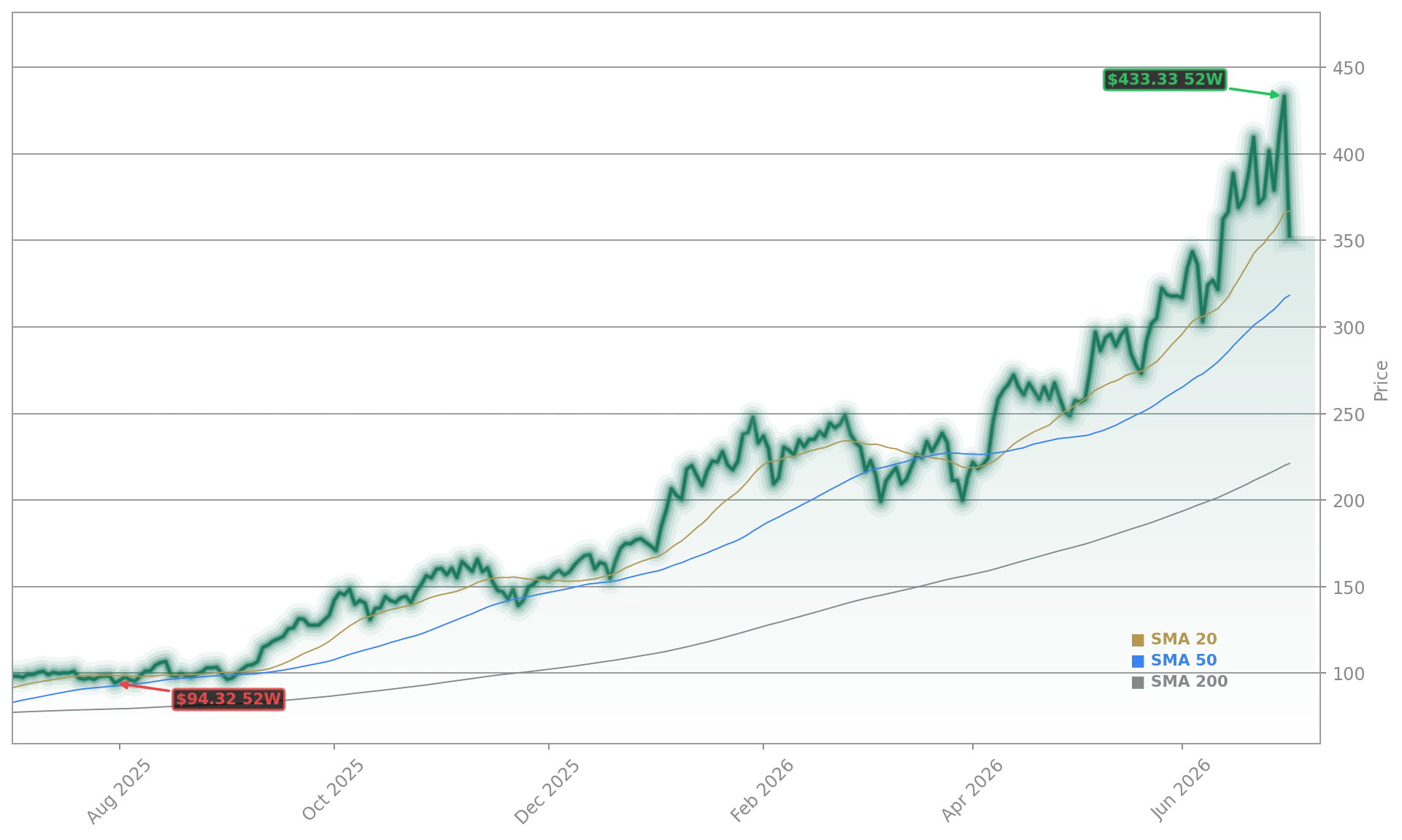

The Lam Research CEO filed a Form 144 with the SEC on July 2 to sell 30,000 shares — a pre-scheduled transaction permitted under Rule 144, not a discretionary trade. While routine for executives managing personal liquidity, the timing is notable: it coincides with Lam Research Corporation’s sharpest weekly decline since early 2025 and comes just two days after the stock hit an all-time high of $438.50. The move contrasts with recent insider activity at peers: at NVIDIA, no executive sales were reported in Q2, and at Micron, director trades were net neutral. Lam Research CEO’s filing — processed via Fidelity Brokerage Services — reflects neither alarm nor urgency but underscores how tightly priced the stock had become: trading at a forward P/E of 55 and a trailing P/E near 80, well above its five-year median of 28.

What’s Driving the Sell-Off?

Three converging forces pressured Lam Research Corporation this week: first, profit-taking after a 153.6% year-to-date surge — the largest among major semiconductor equipment suppliers. Second, softening sentiment around AI-driven memory capex, triggered by reports of budget scrutiny at Meta and other cloud infrastructure spenders. Third, escalating legal uncertainty among top customers: Samsung, SK Hynix, and Micron face overlapping antitrust and export-control investigations that could delay or cancel multi-billion-dollar fab expansions. Lam Research Corporation derives 39% of revenue from memory equipment and 54% from foundry tools — making it uniquely exposed to both segments’ volatility. The stock’s 85% implied volatility — up from 42% in April — confirms mounting uncertainty.

How Does This Compare to Peers?

Lam Research Corporation’s correction stands apart from broader semiconductor equipment trends. While Applied Materials (AMAT) dipped 3.2% and KLA Corporation (KLAC) fell 1.8% this week, Lam Research Corporation’s 9.98% drop was the steepest in the group. That divergence reflects its outsized exposure to memory — a sector now facing near-term normalization after explosive 2025 growth. By contrast, Tesla and Apple remain insulated from memory capex swings, while NVIDIA’s 7.42% YTD gain looks modest next to Lam Research Corporation’s surge — yet NVDA’s valuation remains anchored by recurring AI software revenue. Citigroup maintains a ‘Buy’ rating on Lam Research Corporation but lowered its 12-month price target to $375 from $420, citing ‘valuation exhaustion ahead of Q4 guidance.’ RBC Capital Markets reaffirmed its ‘Outperform’ rating, noting ‘strong DRAM and 3D-NAND order visibility through 2027.’

Is the Long-Term Story Still Intact?

Yes — but with recalibrated expectations. Global memory equipment spending is projected to rise 29% to $52 billion in 2026, driven by AI data center demand. SK Hynix forecasts a 20% wafer supply-demand gap persisting through 2030 — a structural tailwind for Lam Research Corporation’s etch and deposition tools. Fiscal 2026 revenue is on track to hit $23.1 billion (+25% YoY), and Q4 EPS guidance of $1.50–$1.80 implies full-year earnings near $6.75. Goldman Sachs projects $9.91 EPS by fiscal 2028 and a potential $564 price target — a 44% upside — assuming a 39.5x multiple. Still, the current 55x forward P/E demands flawless execution and no macro shocks. The Lam Research CEO’s sale doesn’t contradict that thesis — but it does remind investors that even in AI’s golden age, valuation discipline matters.

What’s Next for Lam Research Corporation?

Investors now await Lam Research Corporation’s Q4 earnings call on August 19 — where management will clarify capex visibility, China exposure (33% of revenue), and margin trajectory amid rising R&D spend. Short-term, the stock faces resistance above $375 — the 50-day moving average — and support near $335, the June 2026 low. With Micron’s blowout June 24 report lifting memory sentiment, Lam Research Corporation could rebound sharply if Q4 guidance reaffirms growth. But until then, the Lam Research CEO’s insider filing serves as a timely reminder: in hypercharged markets, even the strongest fundamentals require price-aware entry points.

We remain confident in our long-term roadmap and the semiconductor industry’s structural growth drivers, particularly in AI-enabled memory and logic.— Timothy Archer, CEO of Lam Research Corporation

Related Coverage: Lam Research CEO Faces Fresh Questions After 10% Stock Drop analyzes whether the insider transaction reflects strategic caution or routine portfolio management. Lam Research Q4 Earnings Preview: Memory Capex in Focus breaks down how DRAM and NAND spending trends will shape guidance. Semiconductor Equipment 2026 Outlook: Beyond the AI Hype Cycle compares Lam Research Corporation’s positioning against Applied Materials and Tokyo Electron in a maturing AI infrastructure cycle.