Is the Lam Research CEO share sale just routine profit-taking, or a warning sign investors should not ignore?

Why did the Lam Research CEO sell shares?

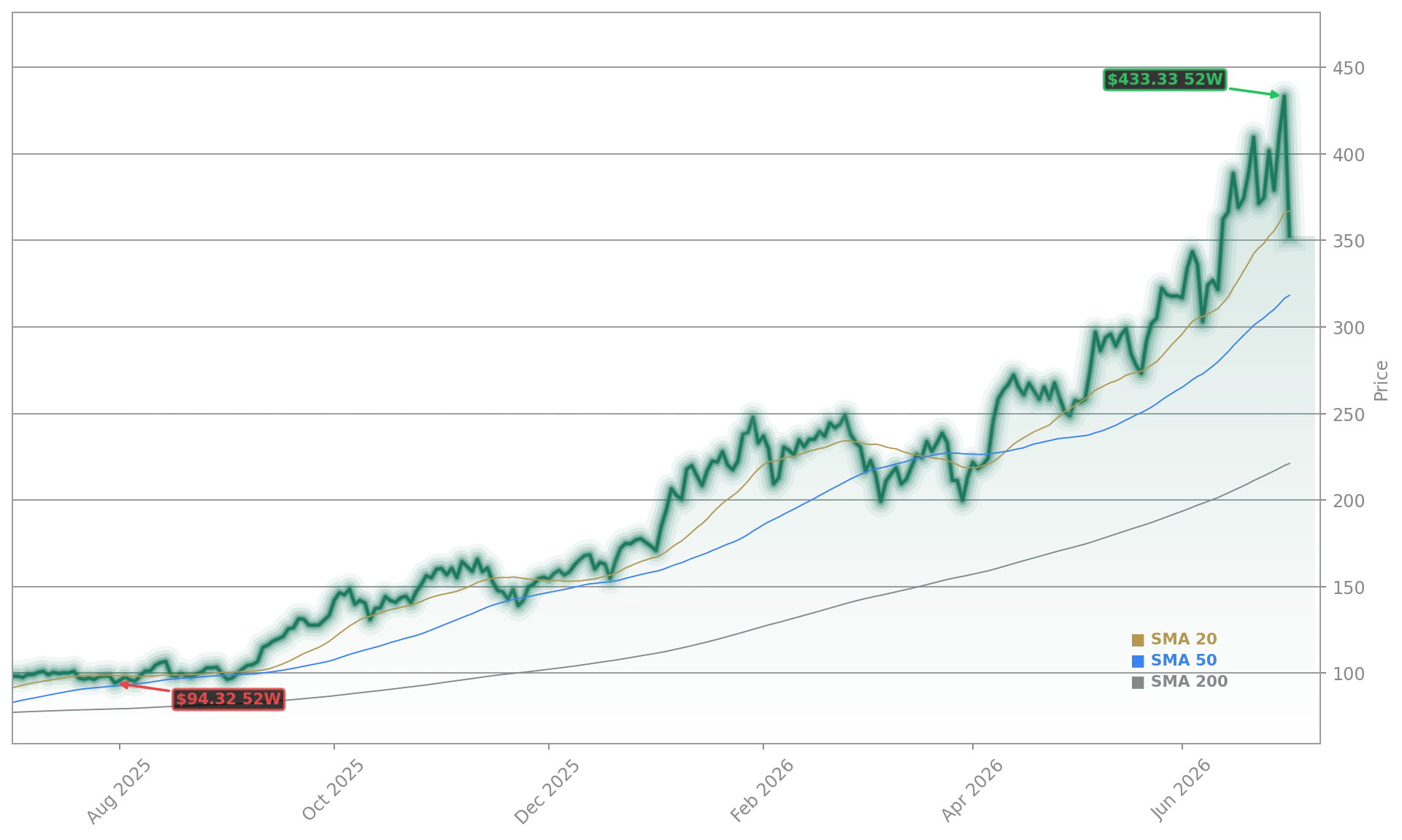

The Lam Research CEO filed a Form 144 on July 2, 2026, disclosing intent to sell 30,000 shares through Fidelity Brokerage Services. Such filings are routine for executives managing personal liquidity and tax obligations — especially after strong stock performance. Lam Research Corporation has surged 111% year-to-date, outpacing both the NASDAQ Composite (+28%) and S&P 500 (+14%). The sale does not indicate a change in strategic outlook: CEO Timothy Archer reaffirmed long-term confidence in the company’s roadmap during a post-earnings call, noting that ‘memory capacity additions remain underfunded relative to demand through 2030.’

How is Micron’s boom lifting Lam Research?

Micron Technology (NASDAQ: MU) reported fiscal Q3 2026 revenue of $8.2 billion — 32% above consensus — and raised full-year guidance on June 24. Its AI-optimized HBM3 and LPDDR5X ramp is accelerating capital expenditure across the memory ecosystem. Since Lam Research Corporation supplies ~39% of its equipment to memory manufacturers like Micron, SK Hynix, and Samsung, the surge directly benefits its top line. RBC Capital Markets recently upgraded Lam Research Corporation to ‘Outperform,’ citing ‘unprecedented memory capex visibility’ and raising its price target to $410 — a 16% upside from current levels.

What does Lam Research’s fiscal 2026 guidance reveal?

Lam Research Corporation’s fiscal Q4 2026 revenue guidance of $6.6 billion implies full-year revenue of $23.1 billion — up 25% year-over-year and well above the $18.5 billion recorded in fiscal 2025. Gross margins remain robust at 47.3%, supported by high utilization of its Kiyo and VECTOR platforms. Notably, the company expects foundry-related revenue (54% of total) to grow in tandem with NVIDIA’s Blackwell and Rubin GPU production, while memory-related revenue accelerates faster — a dual-engine growth model rare among semiconductor equipment peers. Goldman Sachs maintains its ‘Buy’ rating, highlighting Lam Research Corporation’s ‘structural advantage in etch and clean technologies’ versus competitors like Applied Materials (AMAT) and KLA Corporation (KLAC).

Is Lam Research’s growth sustainable beyond 2026?

We remain confident in our long-term roadmap and the semico— Maik Kemper, Editor in Chief

Yes — and the data is compelling. SK Hynix forecasts memory wafer supply will lag demand by 20% through 2030, requiring $120 billion+ in new fab investments over the next four years. Lam Research Corporation stands to capture ~28% of that spend, per Morgan Stanley’s latest supply-chain analysis. With fiscal 2028 EPS projected at $9.91 — and potential for $14.27 by fiscal 2030 assuming 20% annual growth — the stock’s forward P/E of 24.8 remains below the NASDAQ’s 39.5 average. That valuation gap, combined with its 2.1% dividend yield and $3.2 billion in net cash, positions Lam Research Corporation as a core holding for growth-and-income portfolios.