Can Marvell Earnings justify the stock’s surge above $200, or is Wall Street already pricing in too much AI optimism?

Why did Marvell Earnings move MRVL?

Marvell Technology, Inc. reported fiscal first-quarter revenue of $2.42 billion, up 28% year over year, while adjusted earnings came in at $0.80 a share, slightly above consensus near $0.79. The standout remained the data center segment, where revenue hit a record $1.83 billion as hyperscalers kept spending on AI clusters, networking, optical links, and custom silicon.

For the current quarter, management guided to roughly $2.7 billion in revenue and about $0.93 in adjusted earnings per share at the midpoint. That guidance reinforced the central message from Marvell Earnings: AI infrastructure demand is still accelerating, and Marvell remains one of the more direct ways for investors to play that buildout beyond the GPU leaders.

The company also lifted its longer-term revenue outlook, now targeting about $11.5 billion for fiscal 2027 and $16.5 billion for fiscal 2028. That matters because Wall Street has increasingly treated Marvell as a supplier not just to traditional networking markets, but to the broader AI supply chain tied to cloud buildouts and custom accelerators.

How strong is Marvell in AI infrastructure?

Marvell’s positioning goes beyond one product cycle. The company supplies connectivity, electro-optics, custom ASIC capabilities, and data movement technology that become more valuable as AI clusters scale. That has made Marvell an important adjacent beneficiary of spending trends that also support NVIDIA and major cloud platforms.

Analyst commentary ahead of and after the report reflected that view. Stifel lifted its price target to $210, while Citigroup moved to $215. JP Morgan raised its target to $240, and Bank of America also set a $240 target. Deutsche Bank, Morgan Stanley, Goldman Sachs, and Cantor Fitzgerald have all updated views as investors reassess how much AI networking and custom silicon upside remains in estimates.

Some of that enthusiasm is tied to Marvell’s exposure to custom chip programs at large cloud players and to optical interconnect demand as workloads intensify. Investors have also been watching ties into ecosystems shaped by companies such as Amazon, Microsoft, and NVIDIA, where higher AI capital spending can ripple through suppliers like Marvell.

What is Wall Street worried about?

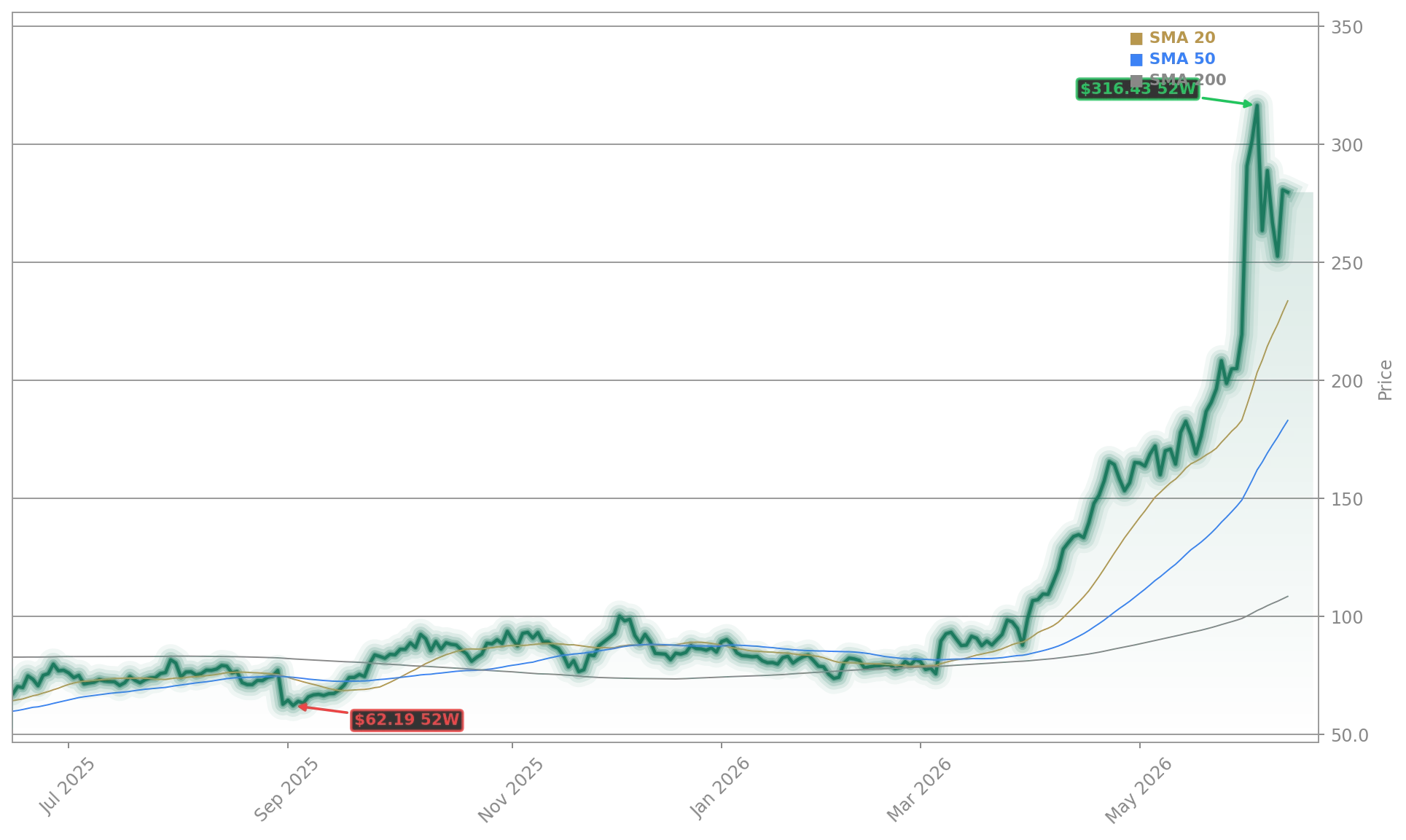

The biggest concern is not whether demand is real, but whether the stock already discounts too much of it. Marvell shares had surged sharply into the print, with some market watchers noting gains of roughly 130% in 2026 before the release. That created a high bar, and early reactions around Marvell Earnings were mixed as traders weighed the beat-and-raise against already lofty positioning.

Valuation is part of the debate. The stock trades at a rich earnings multiple, and Marvell’s adjusted gross margin guidance of 58.25% to 59.25% for the second quarter sits a bit below the prior year’s average near 59.5%. That does not break the bull case, but it reminds investors that growth at scale can still come with margin questions.

Technically, the $200 level now looks important after MRVL pushed above it. If that area holds, bulls may argue the market is accepting a higher earnings base. If it fails, traders may look back toward a lower consolidation zone.

What should investors watch next?

The next key test is whether Marvell can keep converting AI demand into upside revisions without disappointing a market that expects near-perfect execution. Investors will also watch whether custom silicon, optical products, and cloud demand continue broadening rather than relying on a narrow group of customers.

Related Coverage: StockNewsRoom recently examined whether Wall Street had already priced in the best-case AI scenario for MRVL in Marvell Technology Forecast +5.6% as AI Target Hikes Mount. That piece highlighted the same tension now visible after Marvell Earnings: strong AI momentum and rising analyst targets, but also a stock that needs continued flawless delivery to justify its premium.

Our data center business is burning.— Matt Murphy

Marvell Earnings reinforced that the company is becoming a core AI infrastructure name, not just a legacy networking chipmaker. For investors, the story now hinges on whether elevated expectations can be matched by another round of execution and estimate upgrades in coming quarters.