Can Marvell AI Infrastructure keep hyperscaler momentum alive after a brutal selloff rattled one of AI’s hottest semiconductor trades?

What triggered Marvell’s sharp Tuesday selloff?

This week began with strong momentum: Marvell Technology, Inc. surged on Monday after SemiAnalysis reported major production setbacks for Nvidia’s Kyber NVL144 — citing PCB midplane and co-packaged optics (CPO) challenges — and the outright cancellation of the NVL72x2 rack architecture. The news validated Marvell’s strategic focus on custom AI chips and optical networking, with CNBC’s Jim Cramer recently highlighting Marvell’s role in the sector and Jensen Huang’s trillion-dollar valuation comment. Yet the optimism proved fleeting. On Tuesday, Marvell Technology, Inc. plunged -7.4%, its largest single-day drop of the week, amid a broader semiconductor sell-off triggered by Samsung Electronics’ ‘sell-the-news’ Q2 results and weakening risk appetite. The move reflected profit-taking after a 187% YTD rally and growing sensitivity to macro volatility — a dynamic amplified by Marvell’s beta of 2.197.

Price action over the week

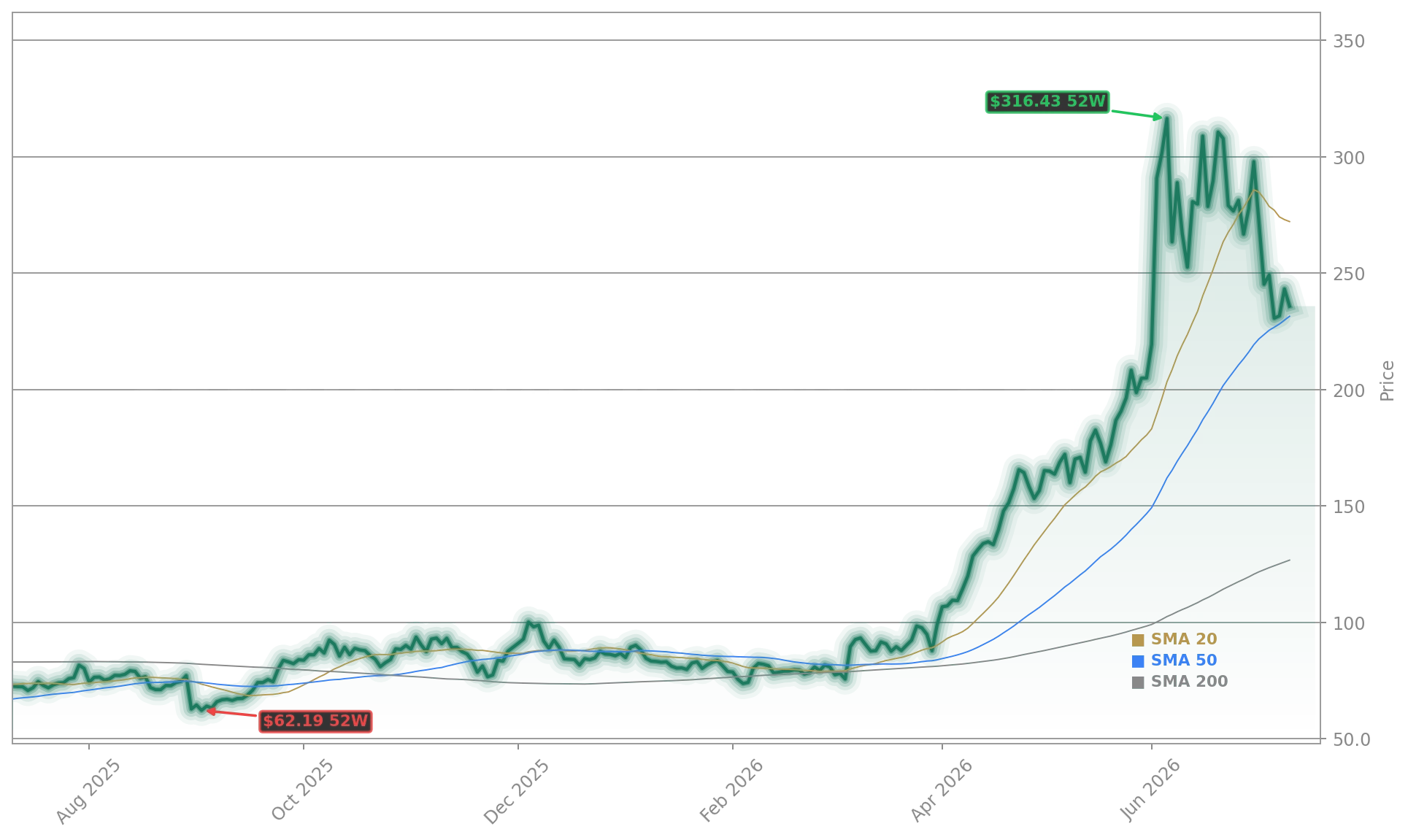

From Monday’s open at $254.76 to Friday’s close at $235.81, Marvell Technology, Inc. lost 7.4% — its worst weekly performance since March. The weekly high stood at $260.40, reached early Monday, while the weekly low of $222.89 occurred midweek — a $37.51 swing reflecting intense sentiment whiplash. Notable outlier days included Tuesday’s -7.4% drop, Thursday’s +5.0% rebound (fueled by RBC Capital’s reaffirmed Outperform rating and $360 price target), and Friday’s -3.0% retreat amid broad market caution. The week’s price action crystallized a core tension: bullish fundamentals anchored in Marvell AI Infrastructure leadership versus near-term valuation fragility and concentration risk.

How do analysts view Marvell AI Infrastructure today?

Wall Street remains overwhelmingly bullish — but with diverging emphasis. RBC Capital reiterated its Outperform rating and $360 price target on July 7, citing >50% data center revenue growth expected this year and next. UBS raised its Buy rating and price target to $340 on June 29, citing the Teralynx T100 102.4 Tbps switch silicon. Goldman Sachs and Bank of America have also turned constructive, citing improving visibility into the custom-silicon pipeline and Marvell’s dual role in AI chips and optical interconnects — a synergy that makes customer relationships ‘stickier’. In contrast, HSBC has taken a more cautious view, flagging customer concentration (76% of revenue now from data centers) and the risk of hyperscalers pulling work in-house. The consensus price target stands at $270.17, though proprietary models project a bull case of $352, suggesting analysts may be lagging behind management’s raised fiscal 2028 guidance.

Why is Marvell AI Infrastructure so pivotal for hyperscalers?

When giants like Alphabet and Meta design their own AI chips — custom ASICs or XPUs — they don’t build alone. They rely on partners like Marvell Technology, Inc. and Broadcom to turn specs into silicon. Marvell’s edge lies in integrating those chips with optical interconnects — the high-speed ‘plumbing’ moving data across AI clusters. That vertical integration creates cross-selling leverage: a customer using Marvell’s silicon is more likely to buy its connectivity products too. Recent milestones — including 5 million Tower Semiconductor PIC shipments and an expanded $2 billion strategic partnership with NVIDIA — confirm Marvell AI Infrastructure is scaling rapidly. Yet the same focus makes Marvell more exposed than diversified peers: data center concentration, a handful of enormous customers, and integration risk from recent acquisitions all weigh on the valuation premium.

What matters next week for Marvell Technology, Inc.?

Investors now pivot to the August 27 earnings report — with Wall Street expecting $2.70 billion in revenue and $0.87 EPS. Key watchpoints include commentary on booking velocity, gross margin sustainability (currently near 59%), and updates on custom XPU wins with the five largest U.S. cloud operators. Macro data — especially the July 17 CPI report — could reignite volatility, given Marvell’s high beta. Also on the radar: any follow-up on the NVIDIA partnership, particularly NVLink integration progress, and whether Marvell’s optical interconnect roadmap keeps pace with 1.6T and 51.2T Ethernet demand. A sustained break above the 20-day SMA ($273.10) would signal renewed bullish momentum; failure to hold $244 support could extend the consolidation.

Marvell Technology, Inc. delivered a textbook week for Marvell AI Infrastructure: powerful fundamentals colliding with sharp sentiment swings. The 7.4% weekly loss wasn’t a rejection of the thesis — it was a recalibration of expectations amid heightened risk sensitivity. For investors, the takeaway is clear: Marvell AI Infrastructure remains one of the purest, highest-octane growth plays in the AI hardware stack — but it demands patience through volatility and rigorous attention to execution. With RBC’s $360 target still 52% above Friday’s close and custom silicon wins accelerating, the long-term runway remains intact. The next move hinges on whether Marvell Technology, Inc. can convert infrastructure leadership into consistent, de-risked revenue growth — and whether the market rewards that transition with renewed conviction.

Marvell Technology Forecast -8.5%: RBC Keeps $360 Target details how Marvell’s recent pullback has not derailed Wall Street’s bullish outlook, with analysts citing resilient bookings and structural advantages in AI infrastructure. Meanwhile, NVIDIA China AI Chips: H200 Access Shock Boosts Outlook underscores how geopolitical constraints on NVIDIA’s H200 shipments could further accelerate demand for alternative AI infrastructure solutions — a tailwind directly benefiting Marvell AI Infrastructure’s optical and custom silicon offerings.

We expect revenue growth to continue accelerating each quarter throughout fiscal 2027.— CEO Matt Murphy

Fazit folgt.