Is the SanDisk Meta Deal the start of a lasting AI storage boom, or is Wall Street already pricing in perfection?

What Does the SanDisk Meta Deal Mean for NASDAQ Tech?

The SanDisk Meta Deal is more than a supply contract — it’s validation of SanDisk’s strategic pivot to AI-optimized enterprise SSDs. Meta Platforms is deploying custom AI chips and scaling inference capacity across new datacenters, requiring ultra-low-latency, high-density NAND storage. SanDisk’s BiCS10 technology — co-developed with Kioxia and featuring 332-layer stacking — meets those specs. Unlike legacy memory plays, this deal locks in pricing, volume, and R&D collaboration through 2029. For NASDAQ investors, it elevates SanDisk alongside NVIDIA and Tesla as a foundational AI infrastructure enabler — not just a cyclical component supplier.

Why Did Israel Englander Sell 24% of His SNDK Position?

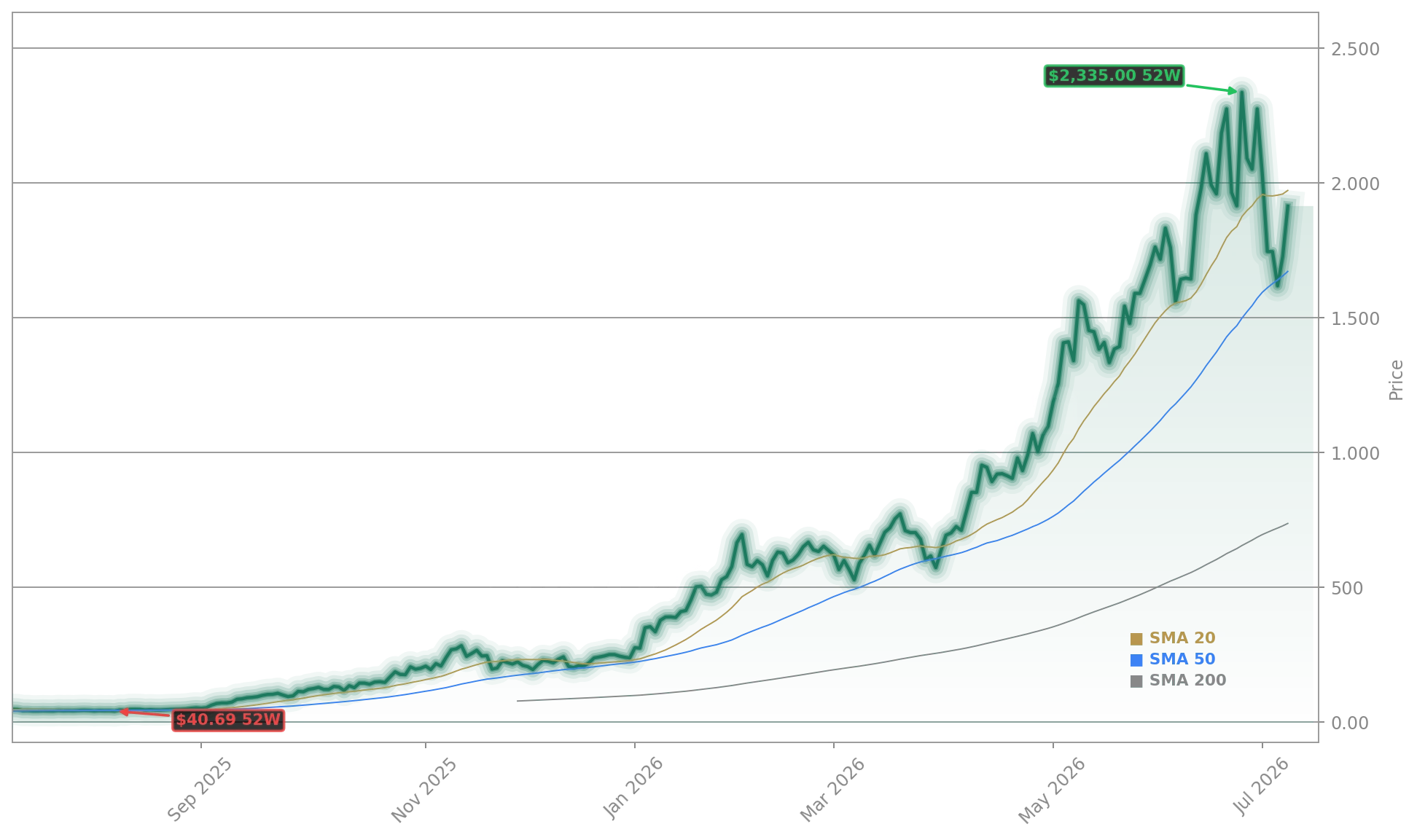

Millennium Management founder Israel Englander sold 1.1 million shares of SanDisk in Q1 2026 — cutting his stake by 24% — even as shares surged 3,600% over the prior 12 months. His move highlights a growing Wall Street divergence: while the SanDisk Meta Deal fuels near-term euphoria, concerns linger over valuation (60x forward P/E), manufacturing dependency on Kioxia, and limited multi-year enterprise agreements (just five signed to date). Englander simultaneously increased exposure to Everpure — a data storage infrastructure play with lower cyclicality — suggesting a tactical rotation from memory volatility to infrastructure resilience.

How Does SanDisk Compare to Micron and SK Hynix?

SanDisk’s Q3 datacenter revenue exploded 645% year-over-year to $1.47 billion — outpacing even Apple-linked supply chain peers. Yet its 60x valuation dwarfs Micron Technology (MU), trading at 22x trailing P/E with owned U.S. fabs and $20+ billion in locked contracts. SK Hynix’s U.S. listing on July 10 added pressure, triggering sector-wide rotation — SNDK gapped down ~3% in after-hours trading despite the Meta news. Bernstein raised SanDisk’s price target from $1,700 to $3,000, citing supply constraints and AI-driven NAND demand, while Wedbush lifted its target to $2,000. Still, analysts note SanDisk’s lack of vertical integration remains a structural risk versus Micron or Samsung.

Is SanDisk’s Profitability Sustainable Amid AI Hype?

SanDisk delivered $23.41 in non-GAAP EPS for Q3 FY2026 — crushing consensus of $14.66 — and guided Q4 revenue to $7.75–$8.25 billion. Gross margins are expected to exceed 84% in FY2027, driven by premium enterprise SSD pricing. But cracks exist: consumer revenue slipped 10% sequentially, and the company remains reliant on the Kioxia Flash Ventures JV for wafer supply. CEO David Goeckeler called this a ‘fundamental inflection point’ — yet Wall Street is pricing in perfection. With S&P 500 tech valuations near all-time highs, any Q4 miss or guidance cut could trigger sharp multiple compression. The August 12 investor day will be critical for clarifying long-term margin sustainability and new customer wins beyond Meta.

NAND flash is emerging as the only economically viable solution to deliver the capacity, performance, and efficiency required to keep models accessible for real-time inference at scale.— David Goeckeler, CEO of SanDisk (Western Digital)

Related Coverage: The SanDisk AI Memory Boom +6.8%: Rally Faces Valuation Test explores whether current momentum reflects durable infrastructure demand or speculative froth. Meanwhile, Intel Forecast -4%: Warning Signs Ahead of Q2 Earnings offers a cautionary contrast — highlighting how semiconductor peers face steeper hurdles in justifying AI-related valuation premiums. For investors weighing SanDisk’s explosive growth against its execution risks, these analyses provide essential context ahead of the Q4 earnings release.