Is the SanDisk Record just another AI trade, or the start of a longer storage supercycle with real pricing power?

What’s Driving the SanDisk Record?

SanDisk (Western Digital) isn’t riding a speculative wave — it’s executing against a hard supply-demand imbalance. With AI data centers demanding exponentially more persistent storage, NAND flash capacity remains critically constrained. Unlike DRAM, where Micron Technology competes across both memory tiers, SanDisk’s enterprise NAND specialization has positioned it as the preferred supplier for hyperscalers like Meta and Microsoft. Its latest quarter delivered $5.95 billion in revenue — up 97% sequentially — and $23.41 in non-GAAP EPS, a 247% jump. More telling: $42 billion in signed backlog and $11 billion in financial guarantees reflect multi-year pricing power, not quarterly noise.

How Does SanDisk (Western Digital) Compare to Micron and Intel?

While Micron (MU) and Intel (INTC) also lead the S&P 500’s 2026 performance, SanDisk (Western Digital) stands apart. Micron trades at 58x forward earnings and Intel at 90x — but SanDisk (Western Digital) trades at just 31x forward earnings despite 124% projected revenue growth next fiscal year. Wall Street sees less cyclicality here: Bernstein’s $3,000 price target — raised from $1,700 on June 30 — is anchored in long-term agreements guaranteeing a 29-cent-per-gigabyte floor, well above Micron’s implied floor. Citigroup followed on June 25 with its own $2,500 target, while Bank of America lifted its estimate to $2,500 on July 1. That consensus — 79% Buy ratings — reflects confidence that this SanDisk Record isn’t a bubble but a re-rating.

Is the Pullback a Buying Opportunity?

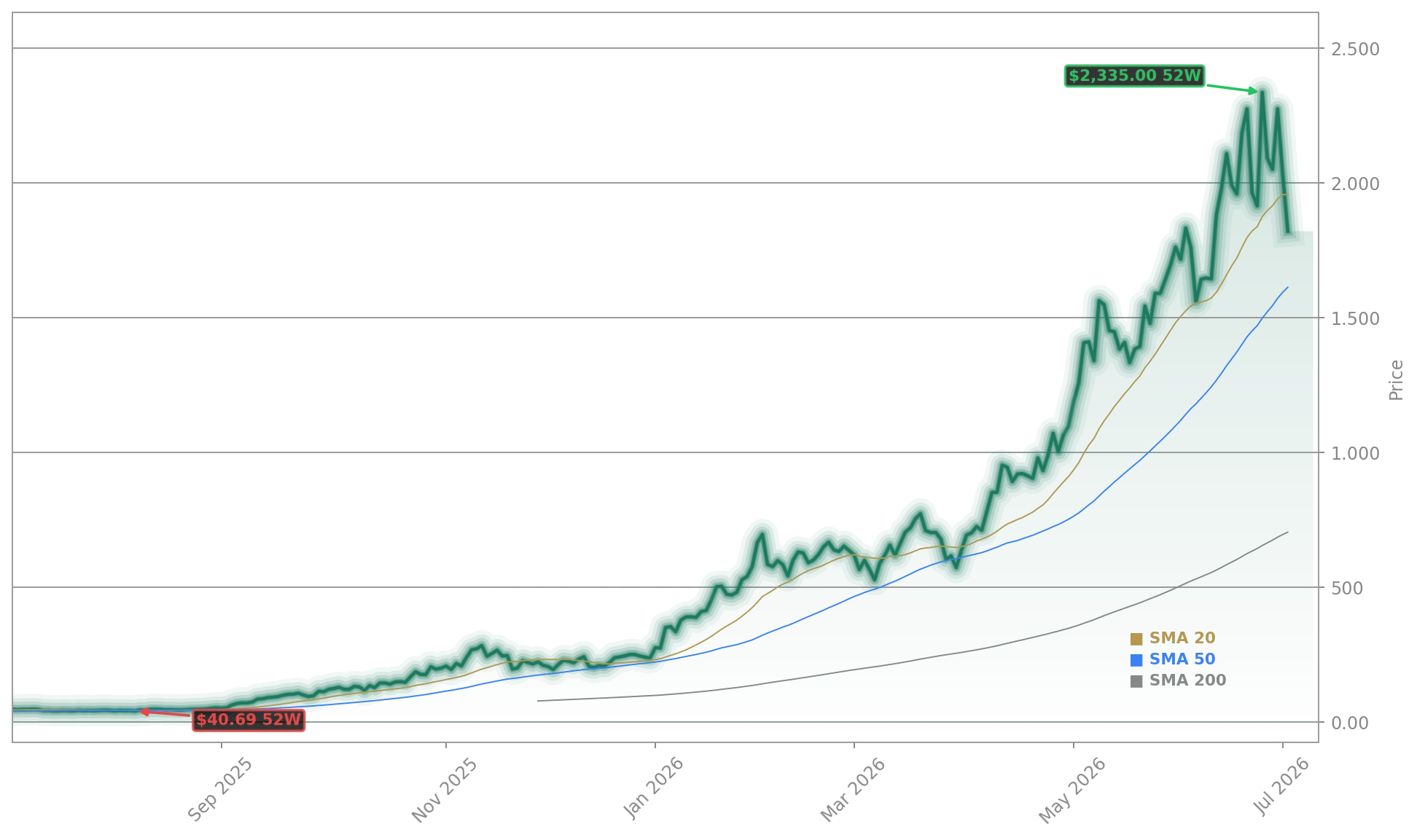

After peaking near $2,354 in late June, SanDisk (Western Digital) retreated 25% — a correction, not a collapse. Technicals remain robust: the stock trades 12.4% above its 50-day moving average ($1,610.45), and the RSI sits at 46.99 — neutral, not oversold. Insider activity warrants attention: Bernard Shek, Chief Legal Officer, sold $1.25 million in shares on July 1 under a pre-arranged plan, consistent with broader profit-taking across memory stocks. But that move stands in stark contrast to analyst conviction — and to the $42 billion backlog, which insulates near-term earnings from short-term sentiment swings. For U.S. portfolios, this volatility is a feature, not a flaw: it creates entry points in a stock with embedded growth rarely seen outside of early-stage AI enablers like Tesla.

What’s Next for SanDisk Record Momentum?

SanDisk (Western Digital) reports Q4 2026 earnings on August 13 — and expectations are extraordinary. Analysts forecast $8.24 billion in revenue (up from $1.90 billion a year ago) and $33.38 in EPS (versus $0.29). More importantly, CEO David Goeckeler stated at May’s investor conference that the NAND market will remain ‘undersupplied for a long period of time’ — a signal that extends the SanDisk Record runway well beyond 2027. With Chinese entrants like YMTC still years from meaningful scale, and hyperscaler contracts locking in pricing, SanDisk (Western Digital) isn’t just participating in the AI boom — it’s structurally advantaged within it. That’s why it’s now a top holding in the Roundhill Memory ETF (DRAM) and the Invesco S&P 500 Pure Growth ETF (RPG).

Our technology and product portfolio are intersecting this extraordinary demand at exactly the right moment.— David Goeckeler, CEO of SanDisk (Western Digital)

Related Coverage: SanDisk’s recent 11.4% plunge — detailed in SanDisk Plunge -11.4% as AI Memory Stocks Face Rotation — was driven by sector-wide profit-taking, not fundamentals, and occurred even as Bernstein and Citigroup lifted price targets. Meanwhile, Adobe Upgrade +4.9%: HSBC Turns Bullish on AI Fears reveals how Wall Street is recalibrating risk across the tech stack — with memory stocks like SanDisk (Western Digital) now viewed as beneficiaries, not victims, of AI disruption.