Can SanDisk’s AI-fueled memory surge survive a sharp pullback, or is the market finally questioning how durable this boom really is?

What’s Driving the SanDisk Memory Boom?

SanDisk (Western Digital) didn’t just ride the AI wave — it helped define its storage layer. With NAND flash now the bottleneck for real-time AI inference at scale, SanDisk’s fiscal Q3 2026 results — ended April 3 — revealed a company in full transformation: revenue surged 251% year-over-year to $5.95 billion, while data center revenue alone jumped 233% sequentially to $1.5 billion. Non-GAAP gross margins hit 78.4%, a staggering figure for a memory business historically plagued by volatility. As CEO David Goeckeler stated on the earnings call, ‘NAND flash is emerging as the only economically viable solution to deliver the capacity, performance, and efficiency required to keep models accessible for real-time inference at scale.’ That narrative resonated powerfully after Micron Technology’s record quarter reignited broad memory-stock momentum — sending SanDisk up 12% on Thursday alone.

How Do SanDisk’s New Contracts Change the Game?

For decades, memory cycles swung on supply-demand imbalances and spot pricing — a recipe for boom-and-bust earnings. SanDisk’s new business model flips that script. The company has secured five multi-year supply agreements with major cloud providers and AI infrastructure firms, locking in committed volumes and pricing backed by over $11 billion in financial guarantees. Management says these deals already cover more than a third of its planned fiscal 2027 output. According to Citigroup, which raised its price target to $2,550, these contracts ‘de-risk the revenue stream and support a structurally higher, less volatile earnings profile’ — a stark contrast to peers like Micron (MU) and SK Hynix, which remain more exposed to spot-market swings.

Is SanDisk’s Valuation Justified?

At $2,234, SanDisk trades at a trailing P/E of ~78 — a number that looks rich until you annualize forward guidance. Management projected $30–$33 in adjusted EPS for Q4 alone, implying annualized earnings near $125 per share. That puts the forward P/E closer to 18 — far more reasonable, especially when compared to Apple’s 32x or Tesla’s 65x. Still, risks remain: NAND capacity expansions are accelerating globally, and insider selling has increased amid the rally. TradingKey notes that ‘while the AI memory thesis is intact, SanDisk’s lack of diversification beyond NAND leaves it uniquely exposed to any normalization in pricing.’

How Is SanDisk Performing Relative to the S&P 500 and Peers?

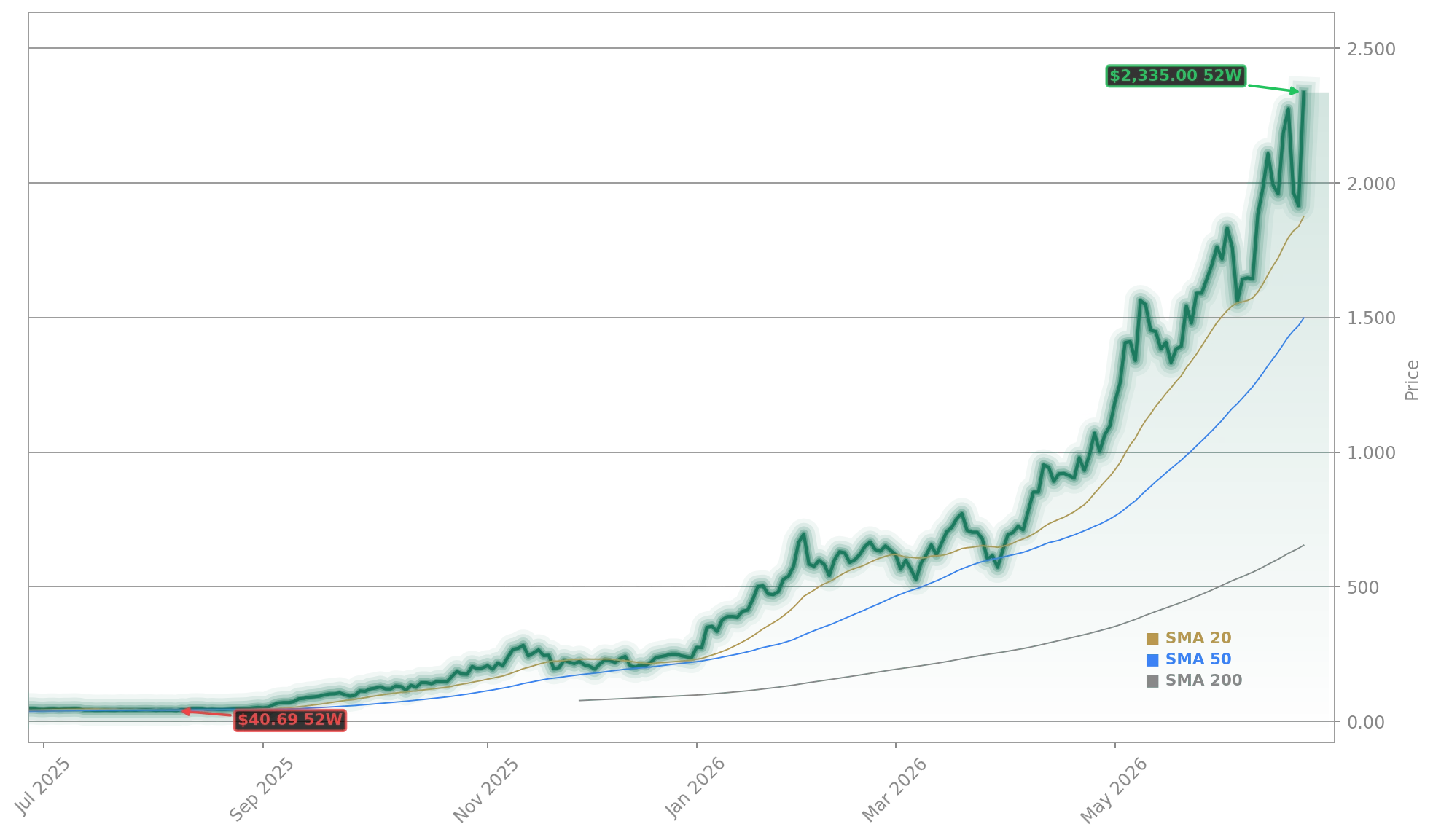

SanDisk (Western Digital) is the top-performing stock in the S&P 500 in 2026 — outpacing even NVIDIA on a percentage basis — and its 726% one-year gain dwarfs Intel’s (INTC) 528%. The NASDAQ Composite fell 0.46% on Thursday, yet SanDisk led gains across the index. Barron’s highlighted the stock as a ‘leading stock during this trading session,’ underscoring its role as a bellwether for AI infrastructure demand. Unlike traditional chipmakers, SanDisk’s revenue is now dominated by hyperscale data centers — a segment growing faster than the broader semiconductor market and increasingly insulated by contractual visibility.

What’s Next for SanDisk Investors?

Wall Street is watching two near-term catalysts: SanDisk’s Q4 earnings report (due July 22) and the commercial launch of its next-generation HBF (High-Bandwidth Flash) modules — designed specifically for Edge AI inference. Seeking Alpha analysts project 57% upside from current levels, citing ‘strong design wins in enterprise SSDs and accelerating Edge AI adoption.’ Meanwhile, TipRanks cautions that ‘the chip sell-off jolts investor confidence,’ especially as SK Hynix prepares for its Nasdaq listing — a move that could dilute SanDisk’s scarcity premium. For U.S. investors, the SanDisk Memory Boom represents both opportunity and discipline: a high-conviction, high-beta play on AI’s storage layer — but one requiring careful position sizing and a clear view on NAND’s supply timeline.

Related Coverage: SanDisk’s explosive AI storage rally is examined in depth in SanDisk NAND Boom +9.4% as AI Storage Demand Surges, where analysts debate whether this is the start of a durable NAND supercycle or a peak that punishes late buyers. Meanwhile, the broader enterprise AI race is highlighted in ServiceNow AI Strategy: Stock Falls 4.4% Despite AI Push, underscoring how infrastructure enablers like SanDisk may benefit even as application-layer players face execution pressure.

NAND flash is emerging as the only economically viable solution to deliver the capacity, performance, and efficiency required to keep models accessible for real-time inference at scale.— David Goeckeler, CEO of SanDisk (Western Digital)

The SanDisk Memory Boom is real, structural, and accelerating — not just hype. For U.S. portfolios, it offers concentrated exposure to AI’s most underappreciated bottleneck: memory. The next quarterly earnings will show whether the momentum holds — and whether SanDisk’s new contracts truly insulate it from the next cycle. Long-term investors should treat this as a core infrastructure holding, not a momentum trade.