Is SanDisk’s explosive AI storage rally the start of a durable NAND supercycle, or the kind of peak that punishes late buyers?

What’s Fueling the SanDisk NAND Boom?

The SanDisk NAND Boom is rooted in AI infrastructure’s insatiable appetite for high-density, low-latency storage. As hyperscalers like Meta and Apple deploy next-gen AI data lakes, demand for SanDisk’s 256TB enterprise SSDs has outstripped supply — triggering a global NAND shortage that Goldman Sachs projects will persist through 2028. Unlike legacy memory cycles, this boom is underpinned by five signed multi-year New Business Model (NBM) contracts worth $42 billion, locking in pricing and insulating margins from volatility. SanDisk’s clean break from Western Digital’s HDD legacy has cemented its status as Wall Street’s purest AI memory play — and the market is pricing it accordingly.

How Does SanDisk Compare to NAND Peers?

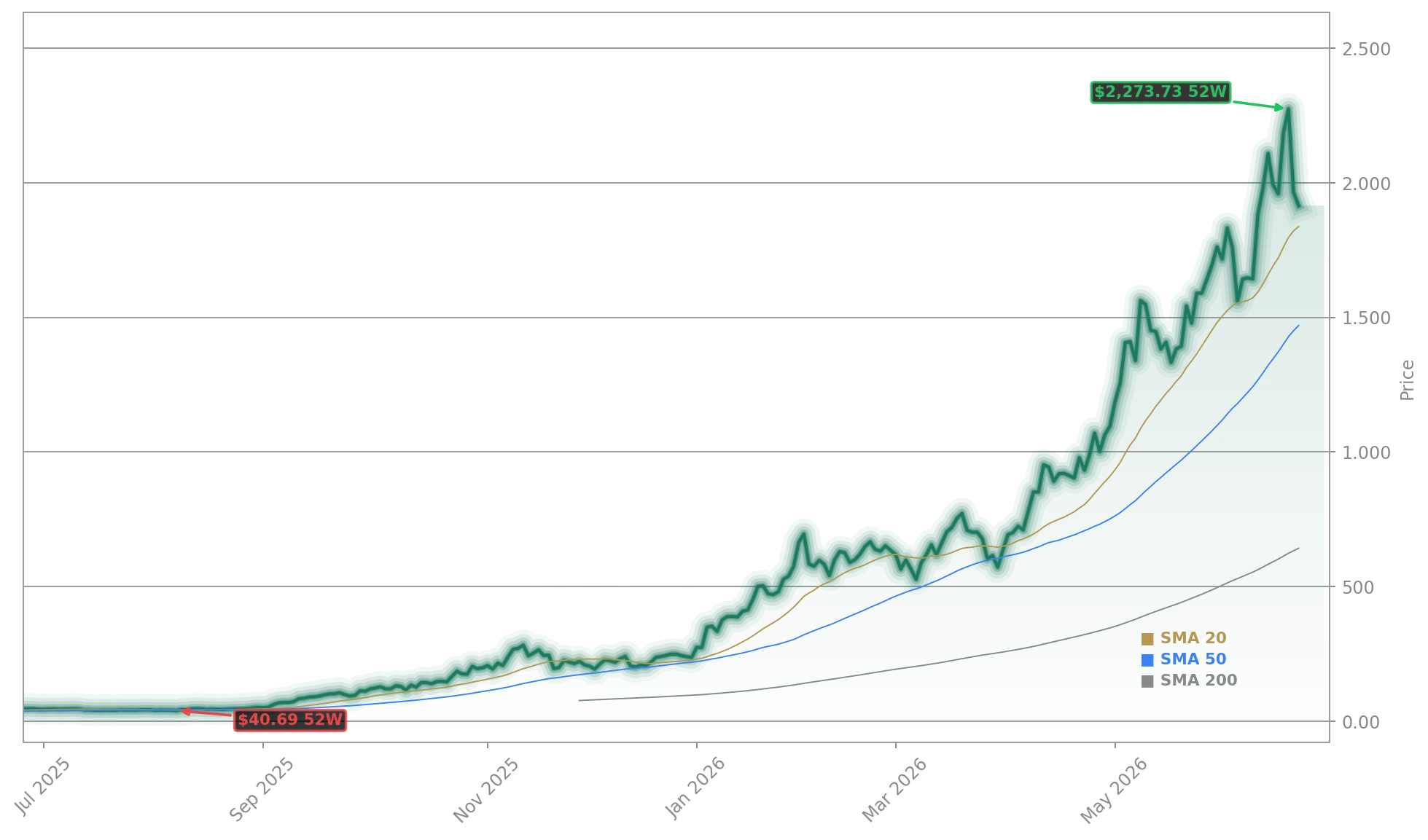

While NVIDIA dominates AI compute, SanDisk now anchors the storage stack — and its performance dwarfs peers. Micron Technology’s Q3 earnings triggered SanDisk’s 4.5% after-hours pop, underscoring sector-wide momentum. Yet SanDisk’s 251% YoY revenue growth and 645% datacenter surge significantly outpace Micron’s 112% NAND revenue growth and Kioxia’s constrained output. Bank of America analyst Wamsi Mohan raised his price target to $2,100 — citing ‘pricing strength through 2027’ — while Mizuho upgraded to Outperform with a $2,200 target. By contrast, Morningstar maintains a $1,000 fair value, warning of bubble conditions. That divergence reflects the core tension: Is SanDisk a $336.7 billion infrastructure utility — or a momentum bubble?

Are Valuations Justified Amid Record Margins?

SanDisk trades at just 10x next year’s non-GAAP EPS — a valuation that looks absurdly cheap for a company generating $1 billion in quarterly free cash flow and operating with zero long-term debt. Yet technical signals are flashing warnings: the monthly RSI hit 99.14, and CTO Alper Ilkbahar sold 2,000 shares near $1,755. 24/7 Wall St. issued a SELL rating with a $1,755.72 target — a 22.78% downside — citing inverted risk-reward above $2,000. Still, bulls point to Q4 FY26 guidance of $7.75–$8.25 billion in revenue and $30–$33 in non-GAAP EPS. With margins holding above 75%, the valuation case remains compelling — if execution sustains.

What’s Next for SanDisk’s AI Storage Leadership?

The next catalyst isn’t just another earnings beat — it’s scale. SanDisk’s HBF (High-Bandwidth Flash) product line, expected to launch in Q4, targets 512TB density and could double hyperscaler rack consolidation efficiency. Simultaneously, $650 billion in 2026 datacenter capex — rising to $1 trillion in 2027 per NVIDIA’s forecast — guarantees demand elasticity. With 122% revenue growth expected in fiscal 2027 and EPS projected to jump from $65.45 to $183.05, SanDisk’s forward P/E of 12 suggests room for rerating — especially if the NASDAQ’s AI trade regains momentum. But the clock is ticking: any sign of NAND oversupply or qualification delays could trigger a swift correction.

Related coverage: The recent SanDisk Plunge -10.6% as Valuation Pressure Hits AI Trade shows how quickly sentiment can shift when technical indicators clash with fundamentals. Meanwhile, Adobe Earnings Hit $6.62B as Record Revenue Meets Doubts highlights a parallel dynamic in the software layer — where AI monetization is accelerating, but valuation discipline is returning. Both stories underscore a broader market theme: infrastructure wins, but execution must keep pace.

We’re at a fundamental inflection point — not just for SanDisk, but for how the world stores and processes AI workloads.— David Goeckeler, CEO of SanDisk (Western Digital)

The SanDisk NAND Boom is real, structural, and accelerating — not a flash in the pan. For investors, it represents a rare chance to own foundational AI infrastructure at a valuation that still discounts future growth. The next quarterly earnings will test whether this momentum can sustain into fiscal 2027 — and whether Wall Street finally treats SanDisk as the high-growth leader it has become. Act now: the opportunity isn’t just in the rally — it’s in the rerating.