Has the SanDisk AI Memory Boom become a real long-term trend, or is Wall Street already pricing in perfection?

Is the SanDisk AI Memory Boom Overdone?

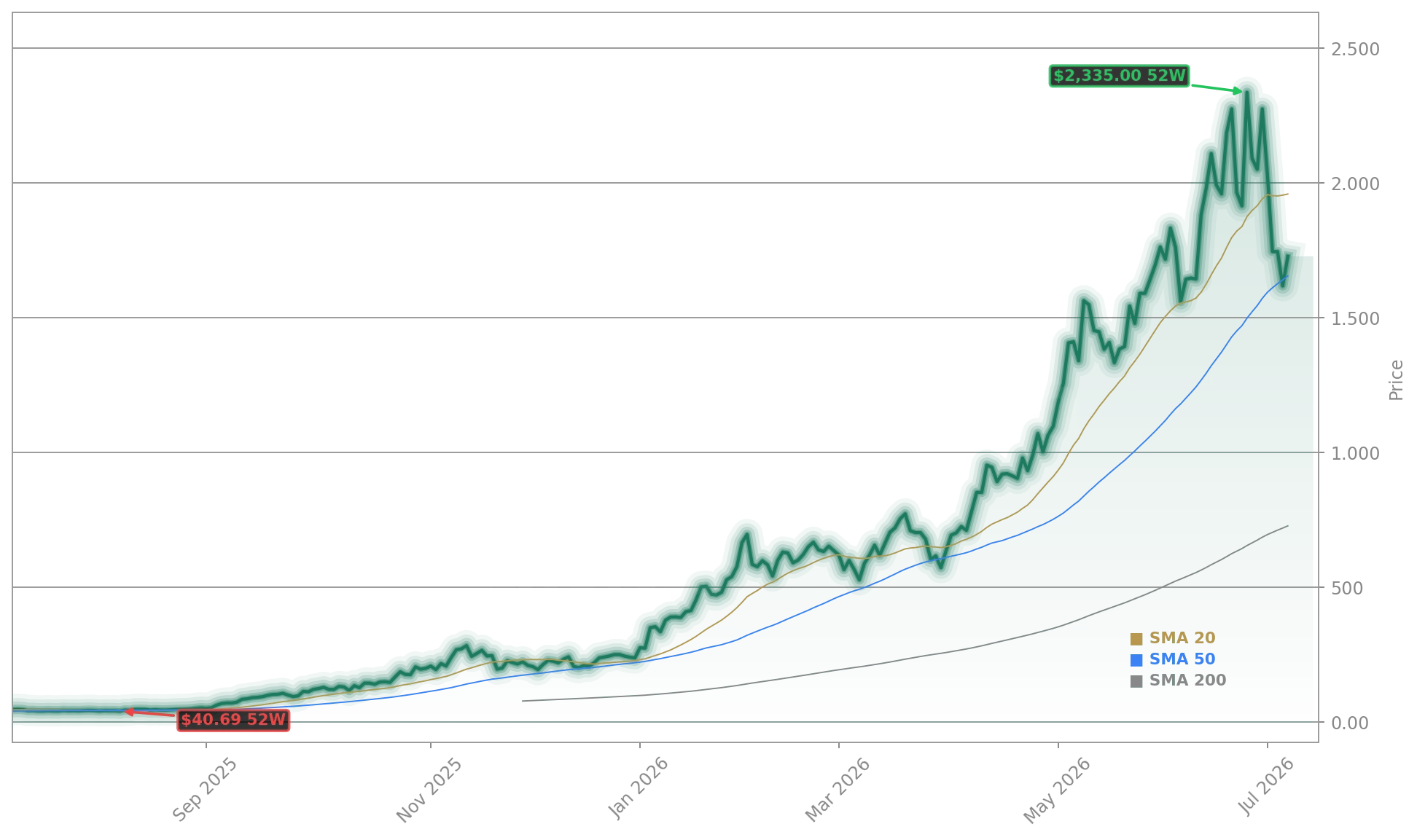

SanDisk (Western Digital) closed Wednesday at $1,727.00—up 6.76% on the day and 635% year to date—yet the rally has hit turbulence. Over the past week, shares fell 14.92%, even as the broader NASDAQ rose 2.1%. The pullback followed a sharp 7.3% intraday selloff on Tuesday, sparked by investor overreaction to Samsung’s announcement of new DRAM fabs in South Korea. Crucially, SanDisk does not manufacture DRAM—it specializes in NAND flash, the non-volatile memory essential for AI inference engines, high-performance SSDs, and generative AI training clusters. As one analyst at Bernstein noted, ‘Samsung’s DRAM play is orthogonal to SanDisk’s core NAND value chain.’ Still, the volatility underscores a growing Wall Street concern: whether the SanDisk AI Memory Boom has priced in too much too fast. With a trailing P/E of 60 and forward P/E of 56, the stock trades at a steep premium to the tech sector’s 39x average—and well above Micron (MU) at 22x and NVIDIA at 48x.

How Is SanDisk Outpacing the Semiconductor Sector?

SanDisk (Western Digital) is outperforming the VanEck Semiconductor ETF (SOXX), which gained just 67.8% YTD—less than one-tenth of SanDisk’s 635% rise. That outperformance stems from structural shifts: AI data centers now consume over 55% of global NAND shipments, per McKinsey, with enterprise SSD demand projected to grow 35% annually through 2030. SanDisk’s Q3 FY2026 results confirmed the inflection: datacenter revenue surged 233% sequentially and 645% year over year, while operating income jumped 272% to $4.2 billion. Its latest NAND generation—33% faster and 34% cheaper—strengthens its edge against rivals like Kioxia and SK Hynix. Notably, SanDisk’s zero-debt balance sheet and $2.99 billion in quarterly free cash flow support its aggressive capital allocation, including multi-year supply agreements with Meta and Microsoft—contracts that lock in demand through 2027.

Are Analysts Still Bullish Amid the Pullback?

Yes—aggressively. Citigroup raised its price target to $2,500, citing ‘tight NAND supply-demand fundamentals through 2027.’ Bernstein followed with a $3,000 target, while China Renaissance set a $3,169 forecast. The consensus 12-month target stands at $1,930.50, backed by 3 Strong Buys, 15 Buys, and only 1 Sell rating. Yet caution is creeping in: GuruFocus flagged six insider sales over the past year—including $1.25 million from Chief Legal Officer Bernard Shek—and noted SNDK’s P/E of 60.65 exceeds both its historical median and the industry average. Bank of America maintains a Buy rating but warns of ‘competitive risks from YMTC and other Chinese NAND entrants.’ That duality—record demand versus rising supply competition—keeps volatility elevated, with 52-week swings from $40.10 to $2,354.39 reflecting extreme sentiment whipsaw.

What’s Next for SanDisk (Western Digital) Investors?

This is a fundamental inflection point for SanDisk—not just growth, but a redefinition of memory’s role in AI infrastructure.— David Goeckeler, CEO of SanDisk (Western Digital)

Three catalysts will determine whether SanDisk (Western Digital) can reach $2,500 by 2027: Q4 FY2026 earnings (due August 5), confirmation of long-term NAND supply contracts, and continued undersupply in the AI memory stack. The path requires a 43% gain from current levels—achievable only if forward P/E expands from 56x to 77x, implying sustained earnings acceleration. Competitors like Micron (MU) and Apple-supplier SK Hynix face similar AI tailwinds, but SanDisk’s pure-play NAND exposure—unlike diversified peers—makes it both the highest-beta and highest-reward name in the AI storage stack. With AI workloads demanding exponentially more NAND bandwidth—and smartphones/PCs no longer the primary memory drivers—the SanDisk AI Memory Boom remains structurally intact, even if its valuation demands patience.