Can MercadoLibre’s growth machine outrun rising credit losses and Brazil’s price war before investor patience runs out?

Why Is MercadoLibre Forecast Under Review?

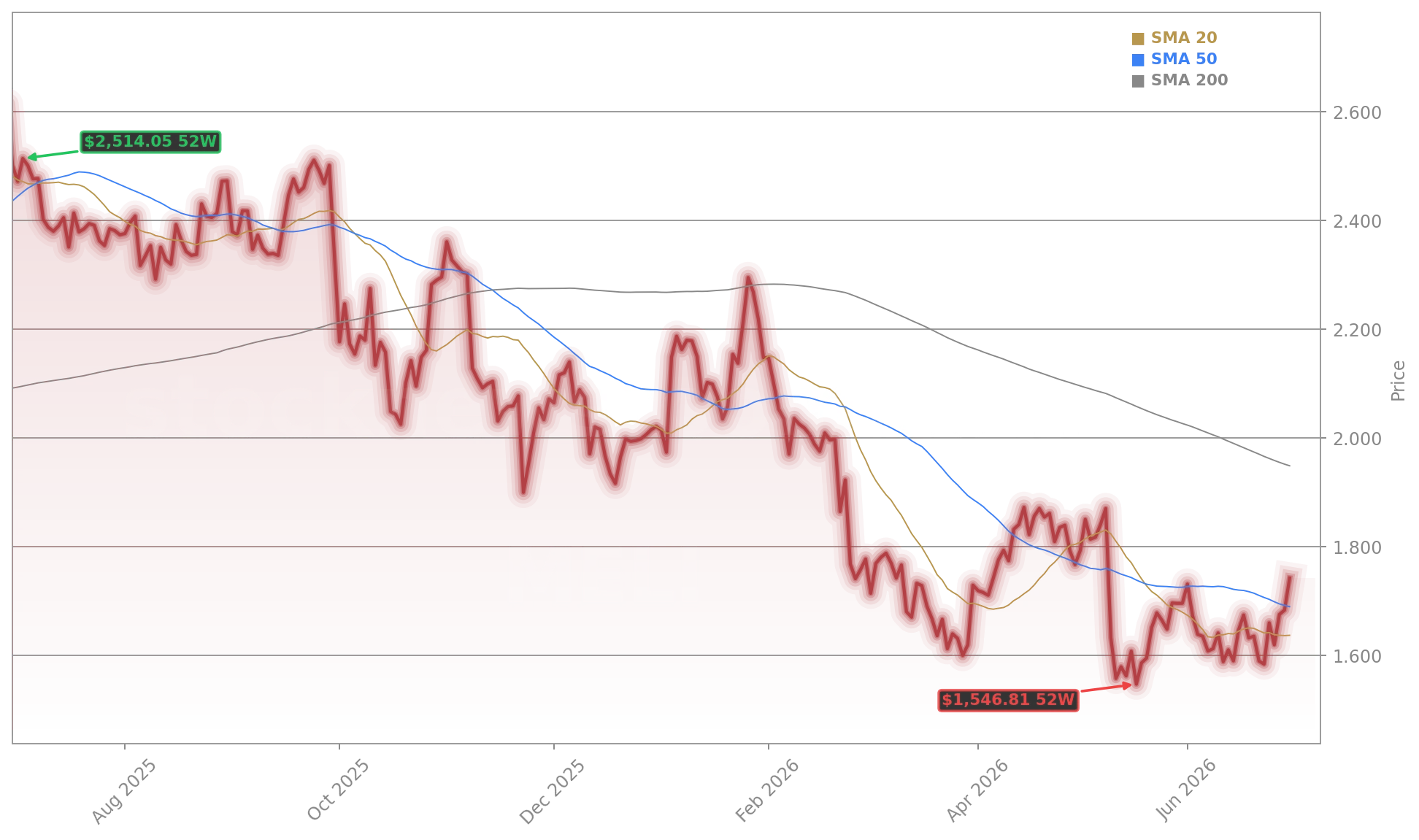

MercadoLibre, Inc. is experiencing a pronounced divergence between top-line strength and bottom-line strain. The company reported $87.2 billion in Mercado Pago transaction volume — up 50% year-over-year — and gross merchandise volume (GMV) growth of 42% in Q1 2026. Yet net income fell short of consensus by 19%, triggering a 17% intraday selloff immediately after earnings. This disconnect has forced analysts to confront structural headwinds: intensifying price wars in Brazil and ballooning credit risk. As of July 1, 2026, MercadoLibre, Inc. trades at $1742.19 — up 2.64% in after-hours action — but remains 16% below its 2026 peak amid mounting skepticism about near-term profitability.

What’s Squeezing MercadoLibre Margins?

Two interlocking pressures dominate MercadoLibre’s margin outlook. First, Brazil’s e-commerce battleground has turned hyper-competitive. International players — including subsidiaries of Amazon and regional challengers — are operating at steep losses to gain share in Latin America’s largest digital market. To retain dominance, MercadoLibre slashed its free-shipping minimum order threshold — a move that lifted GMV and buyer engagement but compressed e-commerce contribution margins by 320 basis points year-over-year. Second, MercadoLibre’s loan portfolio surged 87% in 12 months, driving $1.2 billion in new loan loss provisions. That accounting hit alone erased $0.43 per share in Q1 earnings — more than double the prior year’s provision. RBC Capital Markets downgraded MercadoLibre, Inc. to ‘Sector Perform’ last week, citing ‘unsustainable margin dilution from credit expansion and pricing aggression.’

How Are Analysts Adjusting the MercadoLibre Forecast?

Wall Street’s MercadoLibre Forecast has undergone aggressive recalibration. Over the past 90 days, consensus EPS estimates for 2026 have been slashed by 28%, while 2027 projections fell 25%. Citigroup cut its price target from $1,950 to $1,680, warning of ‘persistent pressure on operating leverage until Brazil’s competitive intensity eases.’ Goldman Sachs maintains a ‘Buy’ rating but reduced its 2026 EBITDA forecast by 15%, citing ‘higher-than-expected fulfillment and credit costs.’ Meanwhile, Morgan Stanley highlighted that MercadoLibre’s adjusted EBITDA margin dipped to 12.1% — its lowest level since 2021 — despite 46% FX-neutral revenue growth. The firm notes that ‘the company’s capital allocation discipline remains intact, but margin recovery hinges on pricing stabilization in Brazil and loan portfolio seasoning.’

Is the Growth Engine Still Intact?

Yes — and that’s why the MercadoLibre Forecast debate remains sharply divided. Active buyers grew 26% year-over-year to 84.1 million, and Mercado Pago’s payment volume now exceeds Apple Pay’s annual volume in Latin America. The company’s logistics network — Mercado Envíos — processed 124 million shipments in Q1, up 38% YoY, while its fintech ecosystem now accounts for 41% of total revenue. Crucially, net cash from operations doubled to $1.07 billion — suggesting underlying cash generation remains robust despite accounting headwinds. For context, MercadoLibre, Inc. trades at 42x forward 2026 earnings — a premium to the NASDAQ’s 28x average — but below peers like NVIDIA (58x) and Tesla (62x) given its emerging-market risk profile. The valuation gap reflects investor demand for clearer margin visibility before re-rating.

What’s Next for MercadoLibre, Inc.?

The company’s capital allocation discipline remains intact, but margin recovery hinges on pricing stabilization in Brazil and loan portfolio seasoning.— Morgan Stanley

Q2 2026 earnings — due August 5, 2026 — will be the true stress test for the MercadoLibre Forecast. Investors will scrutinize whether Brazil’s pricing war is peaking, whether loan loss provisions begin to moderate, and whether GMV growth sustains above 40%. A strong Q2 could trigger a rapid rebound in sentiment — especially if MercadoLibre, Inc. reaffirms its long-term 20%+ operating margin target. Related coverage offers deeper context: MercadoLibre Strategy +45% Boom but Profit Warning explores how ecosystem expansion is reshaping unit economics, while PDD China Expansion +8.3% Rally Despite Analyst Cuts shows how investors reward growth resilience even amid margin warnings — a dynamic that could soon re-emerge for MercadoLibre, Inc. if Q2 delivers clarity.