Can Walmart Forecast hold up as slowing July sales and margin pressure start shaking Wall Street confidence?

Is Walmart Forecast at Risk?

Walmart Inc. is facing intensifying scrutiny as Cleveland Research released a note confirming softening U.S. comparable sales trends quarter-to-date. The firm’s channel checks indicate a measurable slowdown — particularly in consumables and general merchandise — that could undermine the company’s ability to meet its current Q3 guidance. With the quarter ending July 31, the coming weeks are critical: the outcome of July sales performance will likely determine whether Walmart can reaffirm or revise its Walmart Forecast. Notably, Cleveland Research did not downgrade the stock, but flagged inventory normalization efforts — including aggressive price adjustments — as a potential drag on gross margin, even with tariff refunds flowing in.

How Are Tariff Refunds Shaping Strategy?

Walmart is leveraging $1.2 billion in expected tariff refunds — stemming from the Supreme Court’s April 2026 invalidation of Trump-era import duties — to fund targeted price reductions. While this supports its value positioning amid persistent inflation, it also compresses margins. Analysts at Morgan Stanley note that Walmart’s ability to absorb cost pressures remains best-in-class among U.S. retailers, but the dual headwinds of higher oil prices (driven by the Iran conflict) and looming new tariffs scheduled for July 24 add uncertainty. Unlike Amazon, which relies heavily on its Prime ecosystem for margin insulation, Walmart’s model depends on high-volume, low-margin execution — making pricing discipline paramount.

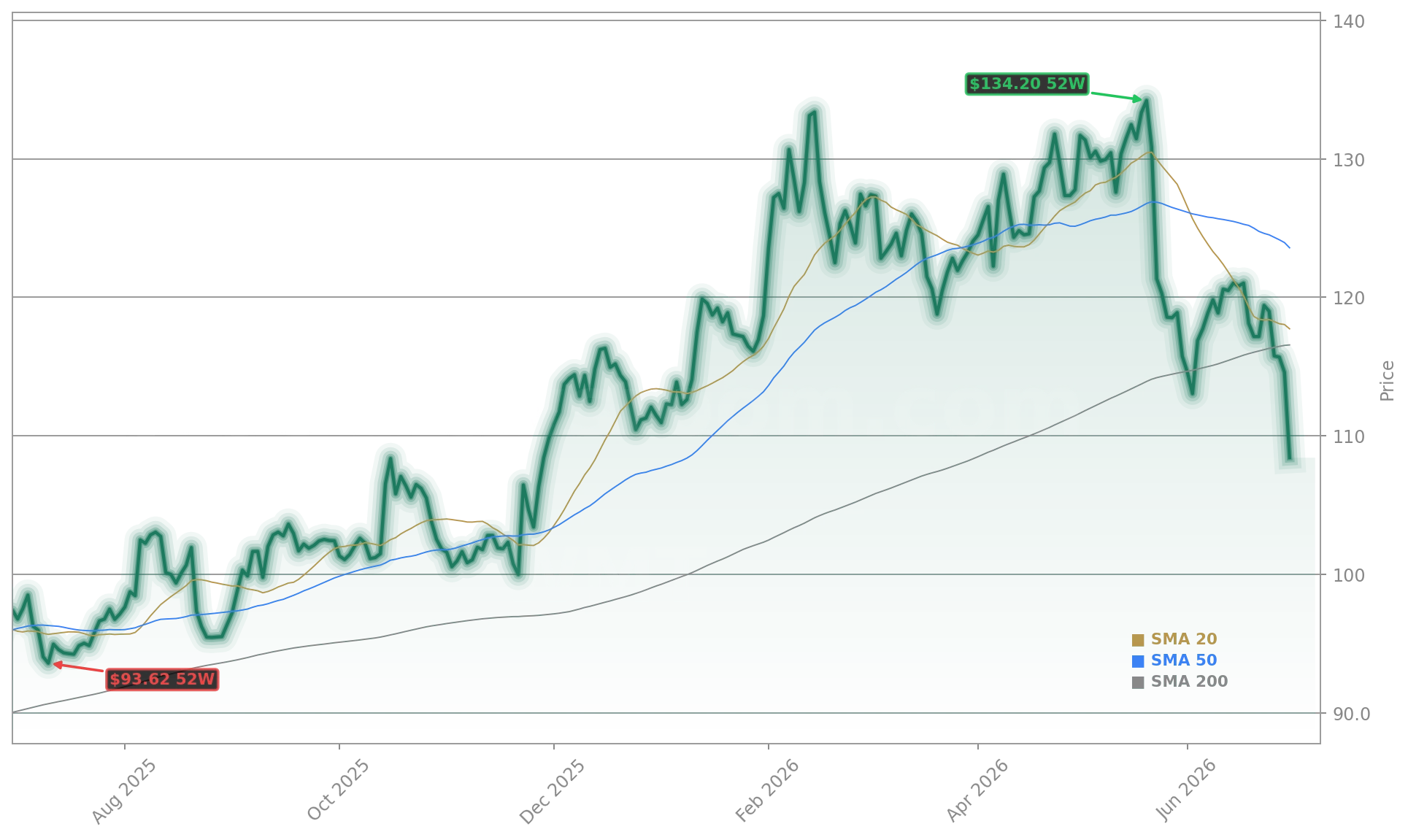

What Do Technical Indicators Say?

Technically, Walmart Inc. is flashing multiple red flags. The stock trades 8.1% below its 20-day moving average and 12.3% beneath its 50-day average — a bearish alignment that has contained rallies since May. Its Relative Strength Index (RSI) sits at 24.96, signaling oversold conditions but offering no guarantee of a reversal. Key support now rests at the psychologically critical $100.00 level — just $8.42 below current pricing and above the 52-week low of $97.35. Resistance looms at $123.00, the May swing high and former 50-day average zone. With options volume surging — 182,812 contracts traded — including heavy put interest at the $110 strike, short-term bearish sentiment is structurally embedded.

How Does Walmart Compare to Retail Peers?

While Walmart Inc. remains a logistics and speed leader — delivering groceries in ~48 minutes nationally per Morgan Stanley — its growth edge is narrowing. Target and Kroger are gaining ground in core markets, with Kroger averaging 40-minute delivery in its densest metro areas. Meanwhile, NVIDIA-powered AI tools are accelerating fulfillment automation across rivals, raising the bar for operational efficiency. Walmart’s valuation — still at 38x forward earnings — looks increasingly stretched versus Target (22x) and Kroger (14x), especially with only ~4% revenue growth expected for fiscal 2027. Citigroup recently lowered its price target to $115 from $124, citing “increased execution risk” and “weaker-than-expected July momentum.” RBC Capital Markets maintains an ‘Outperform’ rating but trimmed its Q3 EPS estimate by 3 cents, citing “inventory-driven promotional intensity.”

What’s Next for Walmart Forecast?

The next major catalyst is Walmart Inc.’s Q3 2026 earnings report, expected in mid-August. Until then, investors will parse weekly traffic data, inventory metrics, and macro developments — including the July 24 tariff deadline and oil price volatility. Cleveland Research’s warning has shifted the narrative from steady execution to potential vulnerability. With the stock now down nearly 20% from its May peak and trading near key technical support, the Walmart Forecast is no longer a given — it’s a question mark Wall Street is actively pricing in. The company’s ability to reaffirm guidance — or deliver a credible path to recovery — will define its near-term trajectory.

No retailer has optimized on all three yet — speed, assortment, and price/delivery fee structure — and we believe these nuanced trade-offs will be critical in driving both consumer and agency-assisted purchasing decisions.— Simeon Gutman, Morgan Stanley analyst

Related Coverage: Walmart’s recent earnings report showed solid bottom-line results but triggered a sharp selloff due to its cautious forward outlook — a pattern that now appears to be repeating ahead of Q3. For deeper context, see Walmart Earnings Fall -7.2% as Weak Outlook Hits Shares. Meanwhile, consumer staples peers like General Mills are navigating similar challenges — reporting a headline $2 billion loss yet holding its dividend — suggesting sector-wide pressure on margins and guidance. Read more in General Mills Earnings +6.4%: Shock Loss, Dividend Holds.