Is Caterpillar’s AI-powered rally cracking as short sellers target stretched valuation and weakening margins?

Why Is Caterpillar Short Bet Gaining Momentum?

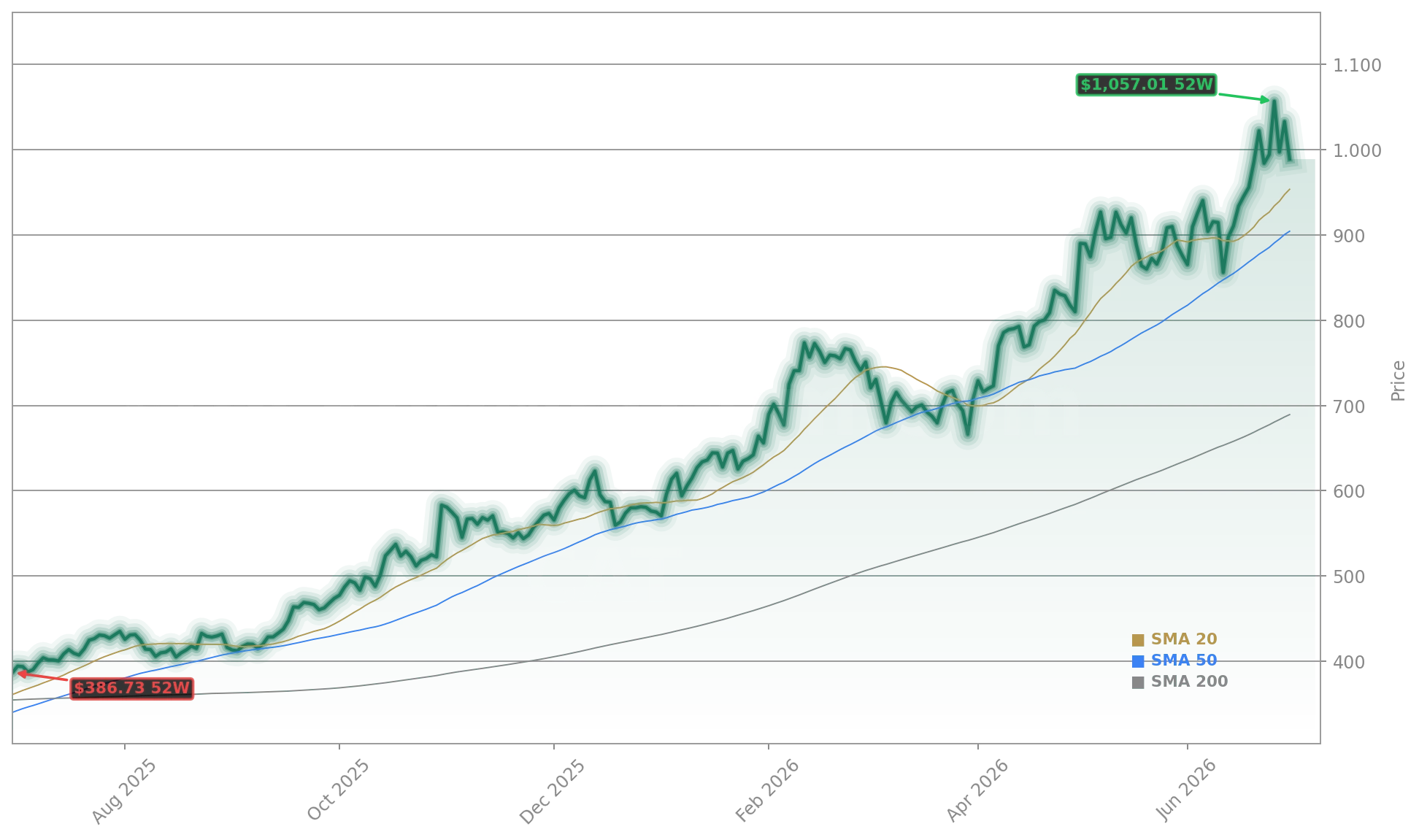

Michael Burry’s newly disclosed short position against Caterpillar Inc. has ignited a wave of institutional reassessment. Burry — renowned for his 2008 subprime mortgage call — entered the trade near $1,060, citing extreme valuation metrics: a forward P/E of 52 and a price-to-sales ratio at a 30-year high. His thesis hinges on decelerating capital expenditures in AI infrastructure, where Caterpillar’s Power and Energy segment (up 22% YoY in Q1) has become overindexed. While the segment supplies critical backup power for hyperscale data centers, Burry warns that hyperscale buildout is plateauing — a view echoed by recent guidance from Caterpillar Record +3% as AI Power Demand Lifts CAT, which noted diminishing marginal returns on new data center deployments.

What’s Dragging the Dow Today?

Caterpillar Inc. was the single largest negative contributor to the Dow on Wednesday, subtracting 323 points — more than Walmart and NVIDIA combined. The stock’s 7.0% plunge ($77.57) came amid broad-based weakness tied to Middle East tensions and global growth uncertainty. Notably, Caterpillar’s decline occurred despite a strong showing from industrial peers: Deere (DE) rose 1.2%, and Honeywell (HON) held flat. This divergence underscores that the sell-off is company-specific, not sector-wide. The move also coincided with passive fund rebalancing following Caterpillar’s removal from key Russell growth and value indices at month-end — triggering forced selling estimated at over $2.1 billion across ETFs and index funds.

Are Margins Holding Up?

No — and that’s central to the Caterpillar Short Bet thesis. Resource Industries, Caterpillar’s largest segment by revenue, reported a 39% YoY profit collapse and an operating margin compression to just 10%. Meanwhile, management warned of $2.2–$2.4 billion in additional tariff- and import-regulation-related costs for 2026 — a direct hit to operating leverage. RBC Capital Markets recently downgraded Caterpillar Inc. to ‘Sector Perform’ citing ‘unsustainable margin assumptions in Power and Energy’ and flagged ‘increasing risk of EPS downgrades in Q3’. Citigroup cut its 12-month price target from $1,150 to $925 — a 7.5% downside — citing ‘over-optimism around AI-driven power demand’.

What Do Options Tell Us?

Options activity signals growing bearish conviction. The $1,020 put contract — just 1% out-of-the-money — is trading with 46% implied volatility and a 67% probability of expiring worthless, implying strong downside conviction. Meanwhile, the $1,100 call (7% OTM) carries 48% implied volatility and only a 38% chance of being exercised — reinforcing expectations of range-bound or lower trading. Trailing 12-month realized volatility sits at 37%, meaning options are pricing in 24–30% more uncertainty than recent price action justifies. That gap — known as the volatility risk premium — is now the widest since early 2022, a classic signal of short positioning buildup.

How Does Caterpillar Compare to Peers?

Caterpillar Inc. trades at a 42% P/E premium to Deere & Company and a 78% premium to Cummins (CMI), despite slower revenue growth and deteriorating margins. In contrast, Tesla’s energy storage business — which competes directly in grid-scale backup power — posted 63% YoY growth in Q1 and expanded gross margins to 28%. Even Apple’s $500 billion capital expenditure plan for AI infrastructure includes zero hardware procurement from Caterpillar Inc., instead favoring custom-built solutions from partners like Flex (FLEX) and Foxconn (2354.TW). This competitive shift further undermines the AI-infrastructure narrative supporting Caterpillar’s valuation.

Caterpillar’s valuation no longer reflects industrial fundamentals — it reflects a speculative bet on AI’s power needs that’s already peaking.— Michael Burry

Related coverage: Caterpillar Record +3% as AI Power Demand Lifts CAT explores how recent strength masks structural demand shifts, while ADP Employment Report +5.3%: Hiring Slowdown, Stock Soars shows how weakening labor data is reshaping industrial capex forecasts — a critical input for Caterpillar’s next earnings cycle.