Has Caterpillar found the most unexpected way to become one of Wall Street’s biggest AI infrastructure winners?

How Did Caterpillar Become a Data Center Powerhouse?

Caterpillar Inc. has long symbolized heavy industry — bulldozers, mining trucks, and diesel engines. But today, its power and energy division is quietly powering the AI revolution. Unlike legacy backup deployments, Caterpillar’s large reciprocating engines and integrated generator sets now serve as primary, grid-independent power sources for hyperscale data centers. With lead times for utility interconnection stretching 36+ months, operators like Microsoft and Amazon are deploying Caterpillar gensets as ‘day-one’ power — turning the industrial giant into a first-call AI infrastructure vendor. This pivot explains why power generation revenue jumped 48% YoY in Q1 2026 to $2.82 billion — nearly all tied to AI data center applications.

What Does This Mean for the Dow and DIA?

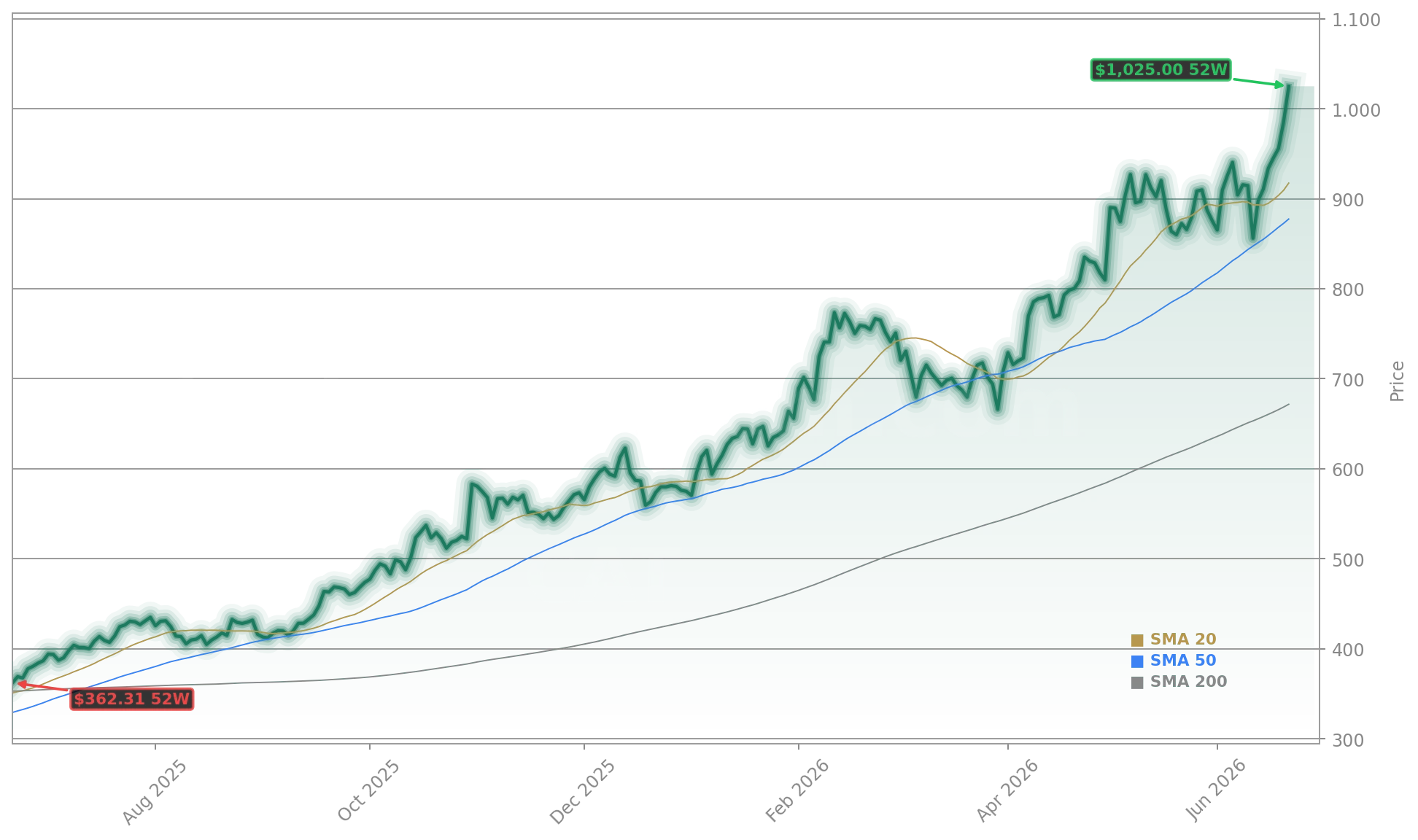

Caterpillar Inc. now dominates the Dow Jones Industrial Average not by market cap, but by price weight — at $1,025.74, it’s the index’s single largest influence, contributing more to daily moves than Apple ($298) or Microsoft combined. The SPDR Dow Jones Industrial Average ETF Trust (DIA) has surged 7% YTD, but its performance is increasingly a proxy for AI capex sentiment. A 10% CAT pullback would now drag DIA roughly twice as hard as a similar drop in Apple — a structural risk Wall Street is only now pricing in. With Caterpillar up 177% over the past year versus Microsoft’s 21% YTD decline, DIA’s ‘smooth ride’ masks extreme concentration — and growing sensitivity to hyperscaler capex guidance.

Caterpillar Data Center Backlog: Is $1,000 Just the Start?

Caterpillar Inc. CEO Joe Creed confirmed a landmark 2.1 gigawatt prime power agreement — its sixth deal of at least one gigawatt — signaling accelerating scale in AI infrastructure. The company has revised its 2030 power generation sales forecast to triple from 2024 levels, up from prior guidance of doubling. That ambition aligns with GE Vernova reporting Q1 data center orders exceeding all of 2025 — and Chevron (CVX) supplying the Permian Basin natural gas to feed Caterpillar and GE Vernova turbines. With AI capex from Microsoft, Amazon, Alphabet, and Meta projected to exceed $37 billion in 2026, Caterpillar’s exposure is both deep and direct — and its $1,000 valuation reflects that shift.

Are Analysts Still Bullish at These Levels?

Yes — but with divergent conviction. Evercore ISI analyst David Raso raised Caterpillar Inc.’s price target to $1,103 from $878 and maintained an Outperform rating, citing ‘unprecedented prime power demand’ and a ‘structurally higher backlog.’ In contrast, UBS analyst Steven Fisher lifted his target to $900 from $677 but held a Neutral rating, noting ‘much of the upside appears priced in’ after Q1’s beat and sharply elevated consensus estimates. The gap reflects Wall Street’s split: one camp sees Caterpillar Data Center as a multi-year structural tailwind; the other sees valuation risk amid a 45x forward P/E.

How Does Caterpillar Compare to Tech Infrastructure Peers?

Power generation grew 48%, driven by strong demand for large gensets and turbines used in data center applications with an increasing mix towards prime power.— Joe Creed, CEO of Caterpillar Inc.

While NVIDIA dominates AI chips and Vertiv (VRT) leads thermal and power distribution, Caterpillar Inc. occupies the foundational layer: prime power generation. Its margin profile — 24.1% operating margin in power and energy — outpaces Vertiv’s 15.3% and rivals industrial peers like Cummins (CMI). Unlike pure-play tech names, Caterpillar benefits from pricing power, long-cycle contracts, and global service networks — making it a rare ‘AI infrastructure compounder’ with industrial resilience. Its dividend — recently raised 8% to $1.63 — further anchors it for income-focused portfolios amid rising rate uncertainty.