Why did solid Walmart Earnings still trigger a sharp selloff as investors focused on what management said comes next?

Why did Walmart Earnings hit the stock?

Walmart Inc. reported first-quarter revenue of $177.8 billion, up 7.3% from a year earlier and ahead of consensus near $174.8 billion. Adjusted earnings per share came in at $0.66, matching expectations. U.S. comparable sales excluding fuel rose 4.1%, while global e-commerce sales jumped 26%. Net income climbed nearly 19% to $5.33 billion.

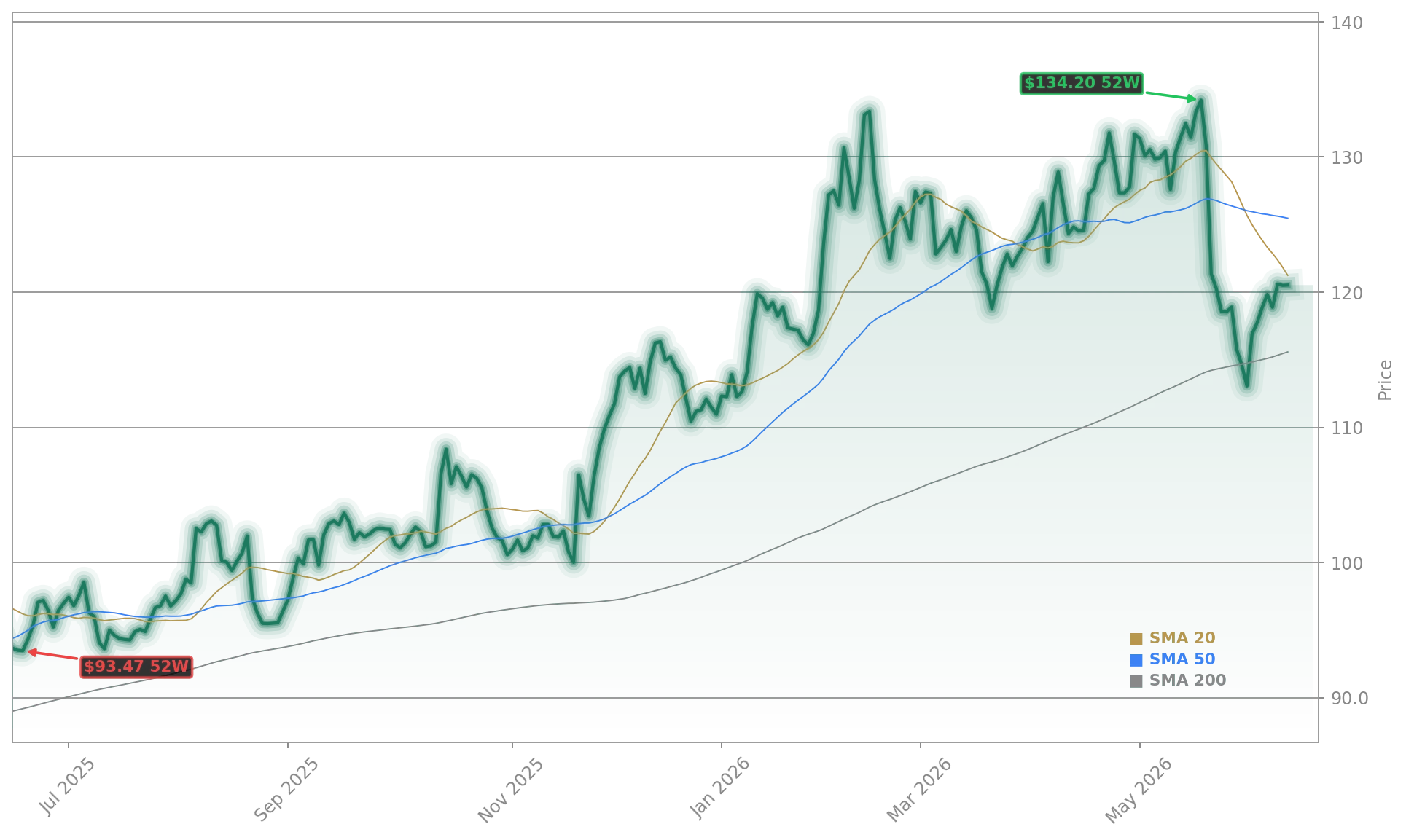

On paper, those are solid Walmart Earnings. But investors were looking for more after the stock had rallied sharply into the report and hit its all-time closing high of $134.20 on May 19. The main disappointment came from the outlook. Walmart projected second-quarter adjusted EPS of $0.72 to $0.74, below the $0.75 consensus, and kept full-year adjusted EPS guidance at $2.75 to $2.85, also below Wall Street expectations near $2.92.

How much are fuel costs hurting Walmart?

Management made clear that higher fuel prices are pressuring both shoppers and profitability. CFO John David Rainey said Walmart absorbed roughly $175 million of fuel cost increases in the quarter, creating a 250-basis-point drag on operating income growth. The company is still investing aggressively in low prices and rollbacks, a strategy that can win market share but limits margin upside.

Rainey also described a split consumer backdrop. Higher-income shoppers are still spending confidently, especially in delivery, fashion, beauty, and other discretionary categories. Lower-income shoppers, by contrast, are becoming more budget-conscious as gas prices rise. Walmart even said average gallons purchased at its fuel stations fell below 10 per visit for the first time since 2022, a sign that household budgets are tightening.

Can Walmart keep taking share from rivals?

That mixed backdrop matters well beyond one retailer. Walmart is often treated as a real-time read on the U.S. consumer, and these Walmart Earnings suggest demand is still holding up, but unevenly. The company continues to gain share across income groups thanks to value pricing, convenience, and fast delivery. Membership income rose 17.4%, and advertising remained a major profit contributor.

The quarter also showed Walmart’s strategic progress against rivals including Amazon and Target. E-commerce strength, marketplace expansion, and Walmart Connect advertising continue to reshape the business mix. In that sense, Walmart looks more like a hybrid of traditional retail and platform economics than it did a few years ago. That evolution helps explain why investors had assigned the stock a premium multiple before today’s drop.

Analyst commentary before the report had been broadly constructive. Citigroup said Walmart was unlikely to raise full-year guidance because of fuel and freight uncertainty. Mizuho maintained an Outperform rating with a $137 price target, while Bernstein had reiterated Outperform and raised its target to $145 ahead of results. Thursday’s reaction suggests the market wanted those bullish long-term calls validated immediately.

What should investors watch next?

With shares now about 9.4% below their all-time closing high and still up more than 26% from 52 weeks ago, valuation remains a central debate. Investors will need to decide whether today’s selloff resets expectations enough, or whether margin pressure and softer earnings guidance point to more downside. Broader market sentiment was also shaped by results from NVIDIA and recent retail updates from Target and Amazon.

Related Coverage: Investors looking for more context on valuation and strategy should also read Walmart Forecast Warning: Can the Valuation Boom Last?. That earlier analysis examined whether Walmart’s AI and e-commerce momentum justified its premium setup, a question that looks even more relevant after this earnings-driven pullback.

The headline consumer is reasonably healthy, but when you look underneath, the pressure is uneven.— John David Rainey

Walmart Earnings showed that demand remains resilient, but Wall Street is now focused on whether fuel-driven cost pressure and softer profit guidance will cap upside in the next quarter. If Walmart can protect margins while continuing to grow e-commerce and market share, this selloff may prove temporary. For investors, the next update will be critical in showing whether the company’s premium story is merely pausing or starting to crack.