Will MicroStrategy’s massive new stock dilution break the premium on its Bitcoin treasury, or is this just cheap fuel for the next crypto bull run?

What did the MicroStrategy Filing reveal?

According to the official Form 8-K MicroStrategy Filing submitted on July 13, 2026, the company raised approximately $466.7 million in net proceeds through its at-the-market (ATM) equity offering program. Between July 6 and July 12, 2026, the corporation sold 4,818,781 shares of its Class A common stock. These transactions were executed under its massive capital-raising program, which includes a $21.0 billion offering expansion initiated earlier in the year.

The fresh capital has been directed into the company’s dedicated U.S. dollar reserve. Following this latest stock issuance, the cash reserve has increased to $3.0 billion. This strategic reserve is specifically maintained to support dividend payments on the company’s outstanding preferred stock and to cover interest obligations on its corporate debt. During this same weekly period, the firm did not execute any share repurchases under its existing buyback programs.

How are MicroStrategy’s Bitcoin holdings affected?

The latest MicroStrategy Filing confirms that the company made no purchases or sales of digital assets during the week ending July 12, 2026. This leaves the total corporate treasury holding unchanged at 843,775 coins. The aggregate purchase price for this massive digital portfolio stands at approximately $63.69 billion, representing an average purchase price of $75,476 per coin, inclusive of all associated fees and expenses.

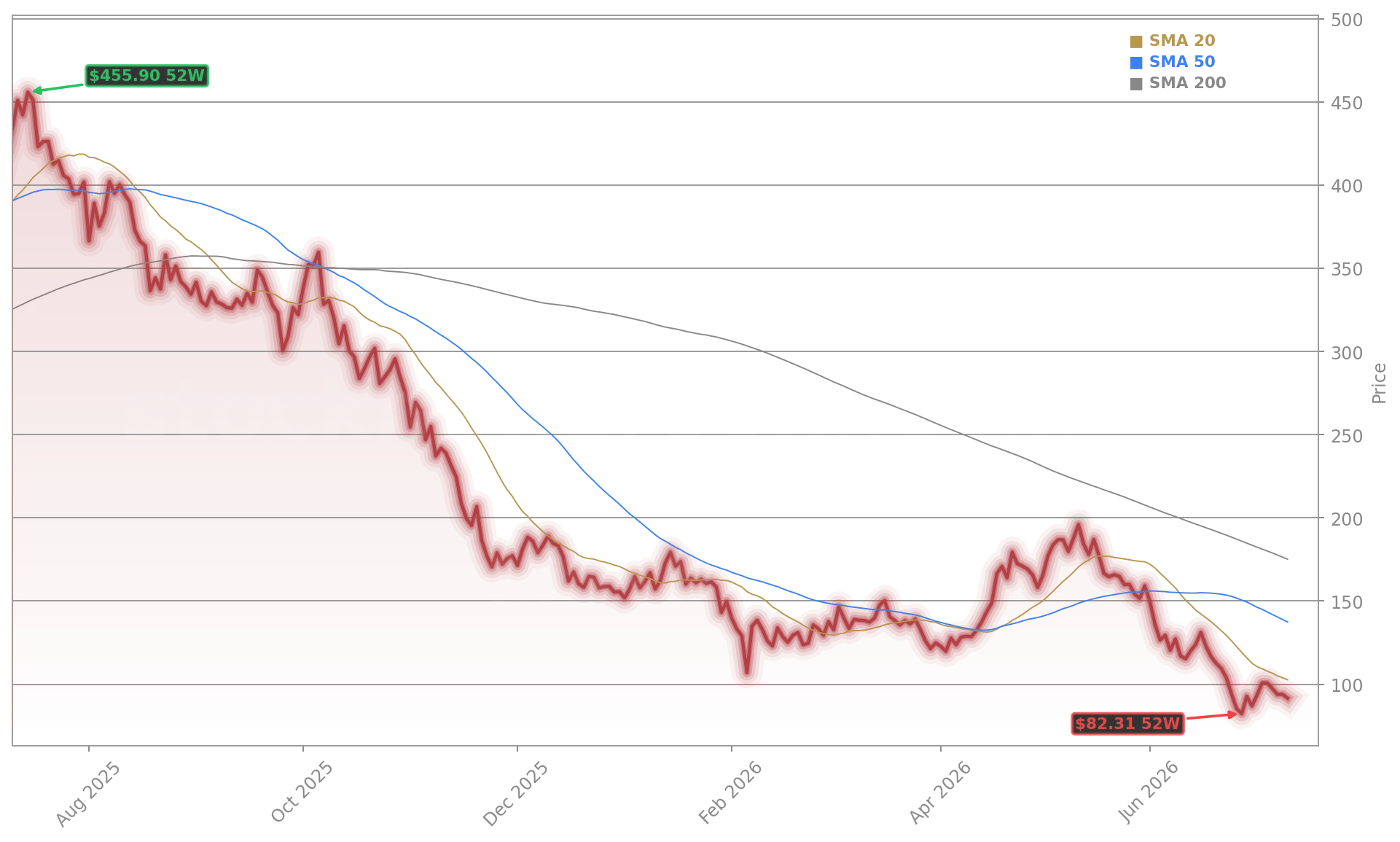

This treasury status update comes at a time of increased market volatility. In early trading on Monday, shares of MicroStrategy Incorporated fell by 3.32% to $91.43, tracking a weekend decline in the broader cryptocurrency market where the underlying digital asset slipped back toward the $62,500 level. The stock has experienced a significant correction of roughly 80% from its historical peak, compressing the premium at which the equity previously traded relative to its net asset value.

How do Wall Street analysts rate the stock?

Despite the recent stock price correction, financial institutions remain highly focused on the company’s dual identity as an enterprise software provider and a proxy for digital assets. Several prominent investment banks have recently updated their outlooks on the firm. Barclays initiated coverage on the stock with an Overweight rating and a price target of $130, emphasizing that a broader sector reset has placed a premium on strong franchises positioned for long-term growth.

Meanwhile, Mizuho adjusted its price target to $213 from $265 while maintaining an Outperform rating. This revision by Mizuho reflects the adjusted long-term price forecast for digital assets through 2027. Overall, the consensus remains overwhelmingly positive, with 90% of covering analysts maintaining a Buy rating on the stock, pointing to substantial upside potential from current trading levels.

Related Coverage

For investors tracking the strategic decisions of the company’s treasury, the recent decision to liquidate assets has raised some eyebrows. The article MicroStrategy Bitcoin Sale +5.3%: Warning for MSTR Bulls explores whether selling digital assets to fund corporate dividends indicates that the company’s once-bulletproof treasury strategy is starting to show cracks.

At the same time, the broader digital finance ecosystem is undergoing rapid regulatory shifts. As detailed in Bitcoin Stablecoin Surges as Circle Wins OCC Approval, new federal banking approvals are paving the way for institutional settlement infrastructures that could redefine how Wall Street interacts with digital ledgers.