If MicroStrategy is selling Bitcoin to fund dividends, is its once-bulletproof treasury strategy starting to crack?

Why did MicroStrategy Incorporated sell Bitcoin?

MicroStrategy Incorporated confirmed the sale of 3,588 BTC — roughly 0.9% of its total 392,000 BTC holdings — to generate $216 million in cash. The proceeds were allocated to cover dividend payments on its 7.5% Series A Preferred Stock and to replenish operating liquidity. Unlike prior capital raises via debt or equity issuance, this transaction signals a structural shift: Bitcoin is no longer treated solely as a long-term store-of-value but as a working capital reserve. That pivot comes as Bitcoin’s price has declined for four consecutive quarters, pressuring MSTR’s ability to sustain its aggressive dividend policy without monetizing reserves. The sale occurred well below MicroStrategy Incorporated’s weighted average acquisition cost of $75,476 per BTC — meaning the company realized a substantial book loss.

What does the MicroStrategy Bitcoin Sale mean for Wall Street?

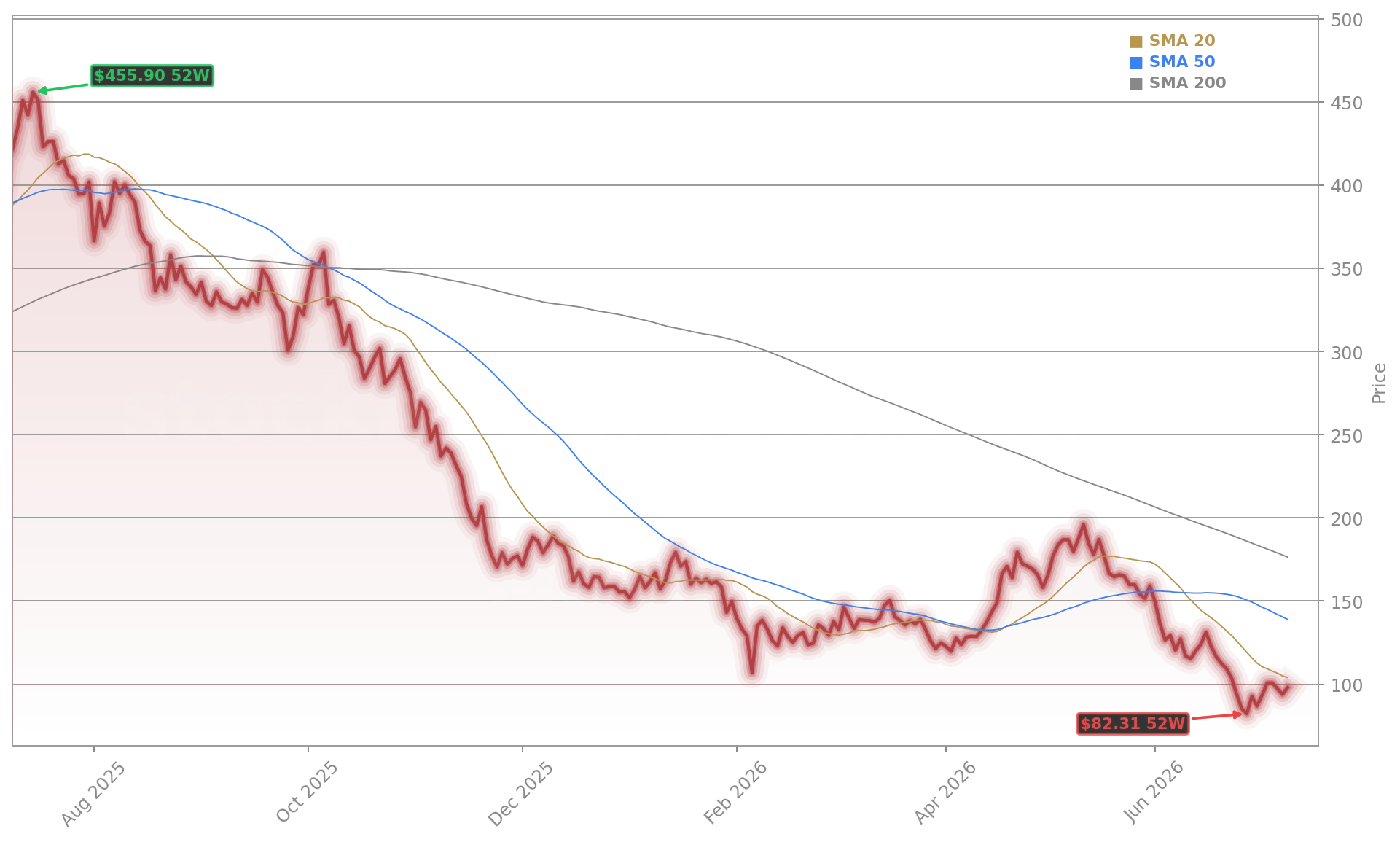

The MicroStrategy Bitcoin Sale is reverberating across the NASDAQ’s crypto-adjacent cohort. While NVIDIA and Tesla continue to benefit from AI and energy transition tailwinds, MicroStrategy Incorporated stands alone as a pure-play Bitcoin balance sheet proxy — and now, a potential liquidity risk indicator. Analysts at RBC Capital Markets note that MSTR’s price-to-BTC-reserve ratio has collapsed from 2.3x in Q4 2025 to parity today, erasing the valuation premium investors once paid for ‘Bitcoin leverage.’ Meanwhile, Citigroup analysts downgraded MSTR to ‘Neutral’ on July 8, citing ‘increasing vulnerability to BTC price decay and diminishing optionality for non-dilutive financing.’ The firm lowered its 12-month price target to $85, warning that further BTC sales could trigger a negative feedback loop — especially if Bitcoin remains range-bound below $65,000.

How does this compare to other Bitcoin-linked stocks?

MicroStrategy Incorporated’s decision stands in stark contrast to peers like Marathon Digital Holdings and Riot Platforms, which have maintained strict ‘no BTC sales’ policies despite margin pressures. Those firms instead cut operating expenses and deferred capex — a discipline MSTR has historically avoided. The divergence underscores MSTR’s unique leverage: its preferred stock obligations create fixed-dollar liabilities, unlike equity-only Bitcoin miners. That structural rigidity makes MicroStrategy Incorporated more sensitive to Bitcoin’s volatility than even Apple-adjacent semiconductor suppliers benefiting from AI chip demand. Notably, MSTR’s pre-market volume surged 220% on Friday — outpacing all Bitcoin-related equities — suggesting institutional traders are actively repositioning ahead of Q3 2026 earnings, expected August 12.

Is MicroStrategy Incorporated’s business model at risk?

Not imminently — but the MicroStrategy Bitcoin Sale is a warning flare. With Bitcoin down 28% from its 52-week high of $92,440 and MSTR’s market cap now just $6.1 billion, the company’s ability to self-fund dividends without further BTC liquidations hinges on either a Bitcoin rebound or new financing vehicles. Goldman Sachs analysts emphasize that ‘the flywheel is broken’ — referring to the prior self-reinforcing cycle where rising BTC prices enabled MSTR to raise capital at ever-lower costs. Without that dynamic, the company faces a stark choice: reduce dividends (risking preferred stock downgrades), issue equity (diluting common holders), or sell more BTC at a loss. Morgan Stanley has flagged MSTR as ‘highly sensitive to Bitcoin’s next 12-month trajectory’ and added it to its ‘Watchlist for Capital Structure Stress.’

Related Coverage: A recent analysis titled MicroStrategy Bitcoin Strategy -4.8% Warning for Bulls explores how shifting BTC treatment could erode investor confidence in MSTR’s long-term thesis. Meanwhile, Cardano Governance +14% as Chang Push Meets Wallet Hack highlights how broader crypto ecosystem resilience — including governance upgrades and security responses — is becoming a key differentiator for digital asset exposure.

This sale changes the calculus for every Bitcoin treasury holder — if MSTR, the most vocal advocate, is monetizing BTC for dividends, what does that say about the asset’s role as a ‘non-correlated reserve’?— Sarah Chen, Senior Crypto Strategist, Bloomberg Intelligence

MicroStrategy Incorporated’s Bitcoin sale is not a one-off liquidity event — it’s the first visible crack in a business model built on perpetual Bitcoin appreciation. For U.S. investors, it underscores the critical need to stress-test Bitcoin-linked equities against multi-year sideways or bearish crypto markets. The next catalyst will be MSTR’s Q3 2026 earnings report, where management must clarify its capital allocation framework and BTC monetization policy. For portfolios seeking crypto exposure, diversification beyond single-asset treasury models is no longer optional — it’s essential.