Is the Oracle AI Strategy powering a sustainable turnaround or just masking the risks of a massive, debt-fueled data center boom?

Oracle AI-Ausbau und Utilities-Offensive is suddenly moving the broader software complex, with Oracle leading S&P 500 gainers as traders rotate back into beaten-down enterprise tech. The stock’s sharp move higher comes even as questions mount over how the company will fund tens of billions in AI-driven data center investments with limited cash and rising debt.

Is Oracle winning back Wall Street?

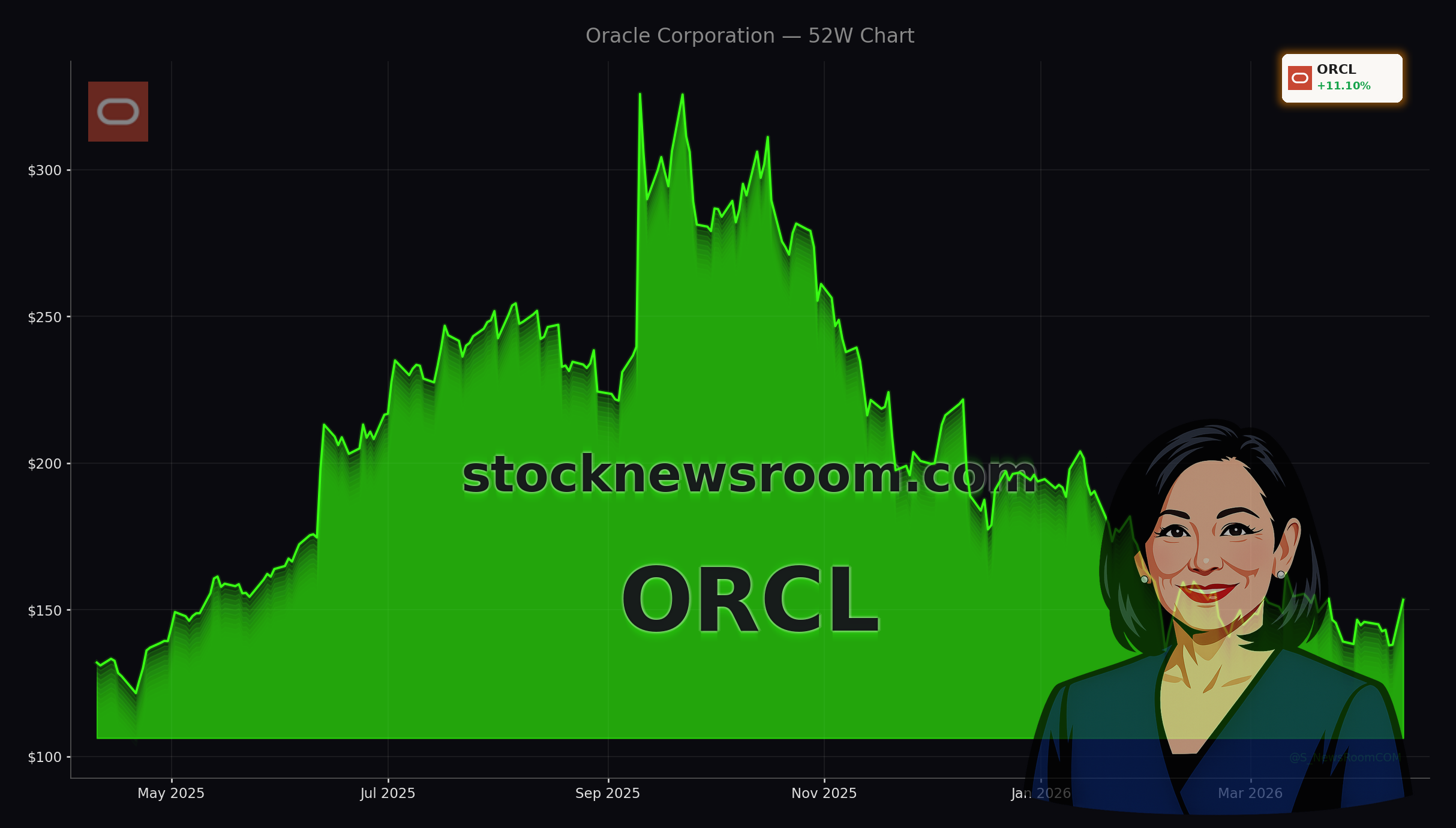

Oracle shares rallied from $138.25 at Friday’s close to $153.47 in heavy NYSE trading, a gain of more than 11% and a rare bright spot in a software sector that has lagged the S&P 500 in 2026. The stock remains down sharply year to date and sits well below its late‑2025 peak, but Monday’s bounce suggests that some investors see the sell-off as overdone in light of the Oracle AI Strategy and accelerating cloud growth.

The move followed Oracle’s launch of new AI-powered upgrades to its Utilities Industry Suite and Aconex construction platform, plus the opening of a new public cloud region in Morocco. These announcements highlight that the Oracle AI Strategy is no longer abstract; it is increasingly tied to domain-specific products aimed at regulated, long-cycle verticals like power, water, and infrastructure management.

Oracle’s short interest, around 27 million shares on a free float of roughly 1.71 billion, leaves limited fuel for a classic short squeeze, but the stock had been technically oversold after a drop of about 28% year to date. Regaining the 50-day simple moving average just above $150 is being watched as a potential trend inflection by technical traders.

How does Oracle reshape utilities with AI?

The centerpiece of Monday’s rally is Oracle’s new AI toolkit for utilities, designed to cut operating costs, reduce outages, and modernize aging grids with predictive analytics and automation. Large regulated utilities like Exelon have already been showcasing their use of Oracle’s financial and customer systems, underscoring that this is an extension of an existing franchise rather than a speculative new venture.

For U.S. investors, the utilities angle matters because it targets a sector that traditionally grows slowly but values reliability, regulatory compliance, and total cost of ownership. By embedding AI directly into billing, maintenance, and field service workflows, Oracle is positioning itself as a critical infrastructure partner at a time when grid investments and electrification are rising. That gives the Oracle AI Strategy a clearer monetization path than some more experimental AI narratives on Wall Street.

At the same time, Oracle continues to lean into horizontal AI capabilities, including being named a Leader in Gartner’s 2025 Magic Quadrant for Talent Acquisition Suites with top scores for extended AI innovations. That recognition helps Oracle compete for AI budgets against hyperscalers and enterprise rivals like Microsoft and SAP as large customers rationalize vendors.

Can Oracle’s balance sheet handle its AI bet?

The other side of the Oracle AI Strategy is its enormous capital intensity. Infrastructure‑as‑a‑Service revenue jumped 84% year over year to $4.89 billion in the latest reported quarter, driving total cloud revenue up 44% to $8.91 billion. Remaining Performance Obligations exploded to $553 billion, up more than 300% year over year, reflecting multi‑year AI and cloud contracts.

To support that growth, Oracle has shifted from an asset‑light software model into a data center builder, driving trailing four‑quarter capital expenditures to roughly $48.25 billion and plunging free cash flow to about -$24.7 billion. Non‑current debt has swelled to around $124.7 billion, putting Oracle at the center of a broader trend of tech companies tapping credit markets to finance AI infrastructure.

The human cost has been severe: up to 30,000 layoffs globally, including hundreds of roles in California, as Oracle reallocates resources to AI and cloud. At the same time, the company is pressing ahead with long‑term projects like its planned multibillion‑dollar East Bank campus in Nashville, which is now slated to become Oracle’s global headquarters, signaling confidence that the AI build‑out will ultimately pay off.

Wall Street remains split. Evercore ISI’s Kirk Materne keeps a Buy rating and a $220 price target on Oracle, betting that 20%+ organic revenue and EPS growth in fiscal Q3 2026 and the $90 billion fiscal 2027 revenue ambition will outweigh near‑term leverage risk. Other investors worry that long lead times on data center projects and heavily concentrated AI partnerships could delay cash returns just as interest costs rise.

How does Oracle stack up against AI peers?

For U.S. portfolios heavily exposed to AI leaders like NVIDIA or cloud titans such as Amazon and Microsoft, Oracle offers a different risk‑reward profile. Its AI story is less about consumer‑facing innovation and more about enterprise workloads—databases, HR, utilities, and infrastructure—running on a vertically integrated cloud stack that aims to minimize so‑called technology debt.

Unlike Apple or other mega‑caps with net cash positions, Oracle is leaning hard on debt markets, making it more sensitive to credit conditions but also potentially more leveraged to upside if its locked‑in AI contracts ramp as planned. The next major checkpoint will be the company’s June earnings report, where investors will focus on IaaS growth, free cash flow trajectory, and early returns from the utilities AI rollout.

Related Coverage

For a deeper dive into the risks and rewards behind the Oracle AI Strategy after the stock’s recent downturn, readers can explore Oracle AI Strategy -3.9% Plunge: Boom or Bust Ahead?, which examines whether the sell-off created a long-term entry point or signaled structural problems. To place Oracle’s infrastructure spending in the broader AI supply chain context, Taiwan Semiconductor Earnings Record as AI Boom Intensifies looks at how surging chip demand underpins the data center arms race.

In the end, the Oracle AI Strategy combines sector‑specific AI products, especially in utilities, with one of the most aggressive cloud infrastructure build‑outs on Wall Street. For investors, the trade‑off is clear: elevated leverage and headline risk versus rare organic growth rates and a $90 billion revenue target that, if met, could re‑rate the stock meaningfully higher. The coming quarters will reveal whether Oracle’s capital‑heavy approach delivers the durable AI cash flows its bold strategy is betting on.