Can Palo Alto Networks justify its premium valuation after a sharp sell-off and a major Wall Street price-target reset?

Why Did Evercore ISI Cut the Price Target?

Evercore ISI Group analyst Peter Levine maintained an Outperform rating on Palo Alto Networks, Inc. but reduced its price target from $375 to $320 — a 14.7% downward revision. The move reflects growing concerns about valuation stretch and near-term profit-taking after PANW’s 74% year-to-date rally, which pushed its market cap above $260 billion. While the firm acknowledges robust execution — including a raised full-year revenue and EPS forecast — it cautions that multiple expansion has outpaced near-term earnings delivery. The $320 target implies just 0.5% upside from current levels, signaling a shift from momentum-driven optimism to earnings discipline.

Is the Palo Alto Networks Forecast Still Credible?

Yes — and that’s why the rating wasn’t downgraded. Palo Alto Networks, Inc. recently raised its fiscal 2026 outlook on strong platform adoption: its AI-native security operating platform now serves roughly 2,280 fully platformized customers, with a best-in-class 120% net retention rate. Management called AI a ‘watershed moment for cybersecurity,’ citing structural demand from AI agents expanding attack surfaces. That narrative is resonating: PANW’s Q2 2026 results — reported June 3 — delivered $3 billion in revenue and raised forward guidance, reinforcing confidence in the Palo Alto Networks Forecast. Notably, Needham countered Evercore’s move just one day earlier, lifting its target to $425 from $350, citing stronger-than-expected cloud and AI-native product adoption.

How Does PANW Compare to Peers on Risk and Return?

Over five years, Palo Alto Networks, Inc. delivered a 40.9% annualized return — more than triple the S&P 500’s 13.4%. Crucially, its correlation to the broader market remains low at 0.49, meaning it offers genuine diversification for U.S. portfolios. Its Sharpe ratio of 0.94 also beats the S&P 500’s 0.61, confirming superior risk-adjusted returns. That profile contrasts sharply with more cyclical tech names like NVIDIA, whose correlation to the NASDAQ exceeds 0.85, or Tesla, where volatility is less asymmetrically rewarded. For institutional investors rebalancing post-Fed pivot, PANW’s blend of AI tailwinds and platform stickiness remains distinct — even as valuation scrutiny intensifies.

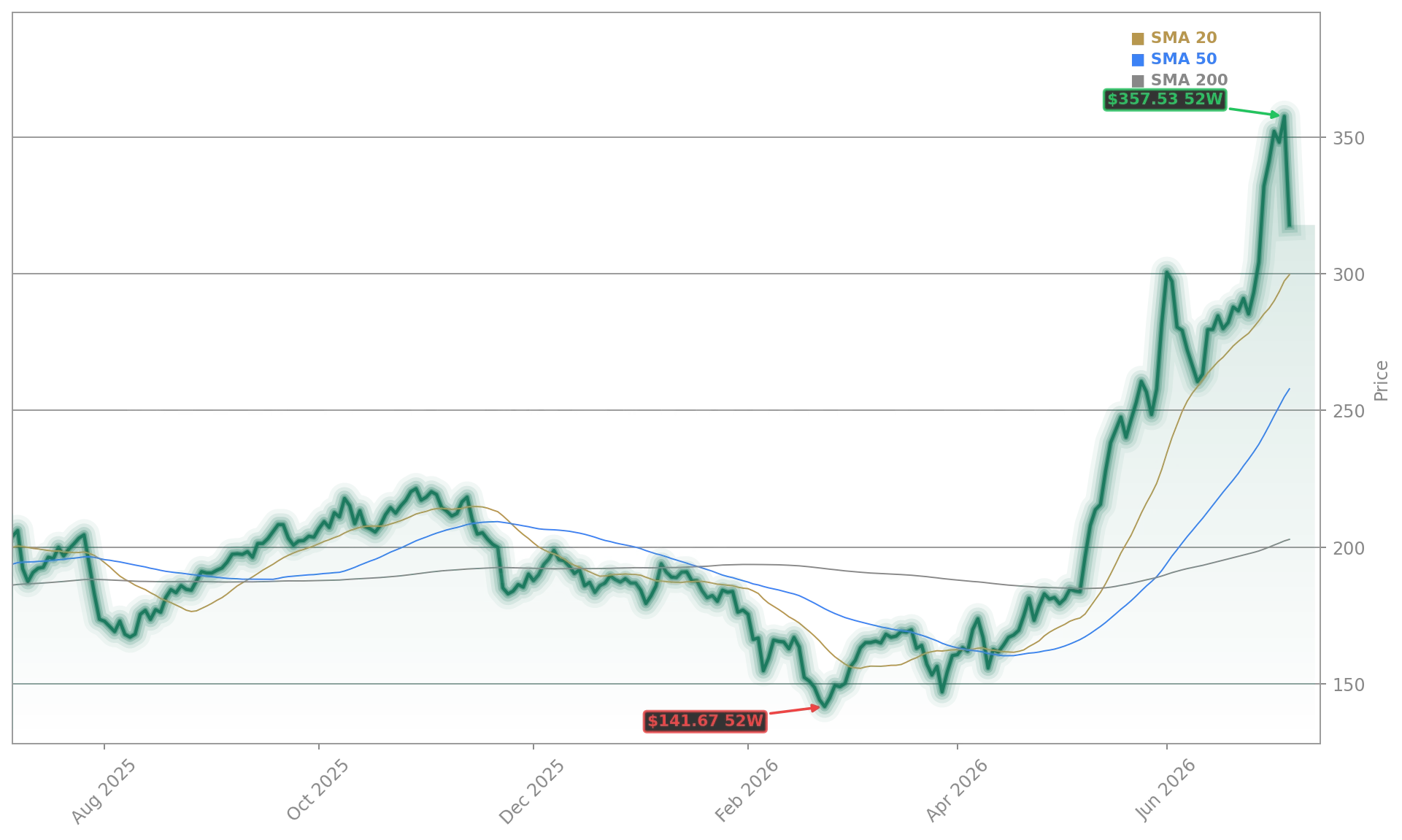

What Do Technicals Say About the Pullback?

Despite Wednesday’s 5.5% decline, PANW’s chart remains fundamentally bullish. The stock holds well above its 200-day simple moving average ($203.49) — up 57.5% — and sits just above key intermediate support near $307 (1-month EMA). Momentum indicators are resilient: the MACD remains above its signal line with a positive histogram, suggesting downside pressure is easing. Traders are watching $297.46 as the next major support level — near the 20-day SMA — and $358.10 as resistance, aligned with the prior 52-week high. Importantly, the ‘golden cross’ (50-day SMA above 200-day SMA) formed in May remains intact, reinforcing the longer-term uptrend. This technical resilience supports the view that the Palo Alto Networks Forecast remains viable — even if near-term gains pause.

What’s Driving the Valuation Debate?

Two forces are colliding: AI-driven growth confidence and acquisition-fueled skepticism. PANW’s planned $25 billion acquisition of CyberArk aims to dominate identity and ‘agentic’ AI security — a strategic bet that’s resonating with long-term investors. Yet critics point to stretched multiples: its Benzinga Edge Value score sits at just 3.47, signaling extreme premium pricing. Meanwhile, growth is rated neutral (60.38), reflecting market awareness that not all expansion is organic. With Wall Street increasingly scrutinizing AI monetization — as seen in recent upgrades for ServiceNow and Apple — PANW must prove its Palo Alto Networks Forecast rests on scalable, profitable platform adoption, not just deal momentum.

AI is a watershed moment for cybersecurity — it’s not just about defending systems, but securing the agents that operate them.— Palo Alto Networks CEO Nikesh Arora

Related coverage: Palo Alto Networks Earnings: $3B Revenue, Outlook Raised details how the company’s Q2 results validated AI platform traction and supported its raised guidance. Meanwhile, ServiceNow Upgrade +2.4% as Wall Street AI Fears Fade highlights how enterprise software peers are benefiting from the same AI infrastructure tailwind — reinforcing the sector’s strength beyond just cybersecurity.