Can PepsiCo’s $10 billion buyback outweigh slowing North America demand and revive confidence in the PepsiCo Forecast?

What’s Driving the PepsiCo Forecast?

Wall Street’s renewed conviction stems from three structural catalysts: accelerating international growth, disciplined capital allocation, and margin resilience. EMEA revenue surged 18% in Q1 2026, Latin America Foods rose 16%, and Asia Pacific Foods climbed 11% — collectively offsetting modest 2% growth in North America Foods. Operating margin expanded 210 basis points to 16.5%, powered by supply chain efficiencies and pricing discipline. With core EPS at $1.61 — 4.26% above consensus — and revenue at $19.443 billion (2.75% above estimates), the PepsiCo Forecast is grounded in demonstrable execution, not speculation.

How Does PepsiCo Compare to Coca-Cola and Kraft Heinz?

While Coca-Cola (KO) continues to leverage brand strength — achieving 20 consecutive quarters of value share gains and launching exclusive Fanta flavors at Wingstop — PepsiCo’s portfolio diversification across snacks and beverages provides unique leverage in inflationary environments. Kraft Heinz’s recent 100% renewable electricity milestone in Europe highlights sector-wide ESG momentum, but PepsiCo’s $10 billion buyback dwarfs peers’ capital return commitments. Notably, PepsiCo’s 4.08% dividend yield now exceeds Coca-Cola’s 3.1%, and its 54-year dividend growth streak — earning Dividend King status — outpaces Kraft Heinz’s 12-year streak. Analysts at Morgan Stanley highlight this yield-plus-growth profile as increasingly attractive amid rising Treasury yields.

Is the $10B Buyback Enough to Anchor EPS?

Absolutely — and it’s already priced for impact. The new $10 billion authorization, extending through February 2030, complements $8.9 billion in total fiscal 2026 shareholder returns. With PepsiCo targeting high-single-digit EPS growth, the buyback provides a critical floor: even under a bear-case scenario where North America volumes stagnate, EMEA’s 29% core operating profit growth and LatAm’s double-digit expansion ensure EPS stability. RBC Capital Markets notes that repurchases will absorb ~2.5% of outstanding shares annually, directly boosting per-share metrics regardless of top-line velocity.

What Risks Could Derail the PepsiCo Forecast?

The primary headwind remains North America consumer affordability. Core PCE inflation sits near a 12-month high at 130.082, constraining price realization and pressuring low-end demand. JPMorgan’s 2026 outlook explicitly warns that traditional value sectors like consumer staples face continued pressure from deteriorating low-income sentiment. Additionally, PepsiCo faces a Supreme Court review of its ‘MTN Dew Rise’ trademark — a legal overhang that could impact brand rollout timing. Still, the bear-case target of $152.61 (10% upside) from Citigroup underscores the stock’s inherent downside protection — a floor anchored by cash flow, not just sentiment.

Why Is Wall Street Still Cautious?

PepsiCo’s international engine is accelerating — EMEA and LatAm Foods are running double-digit growth, and the $10 billion buyback creates a hard floor under EPS regardless of North America weakness.— 24/7 Wall St. Analyst Team

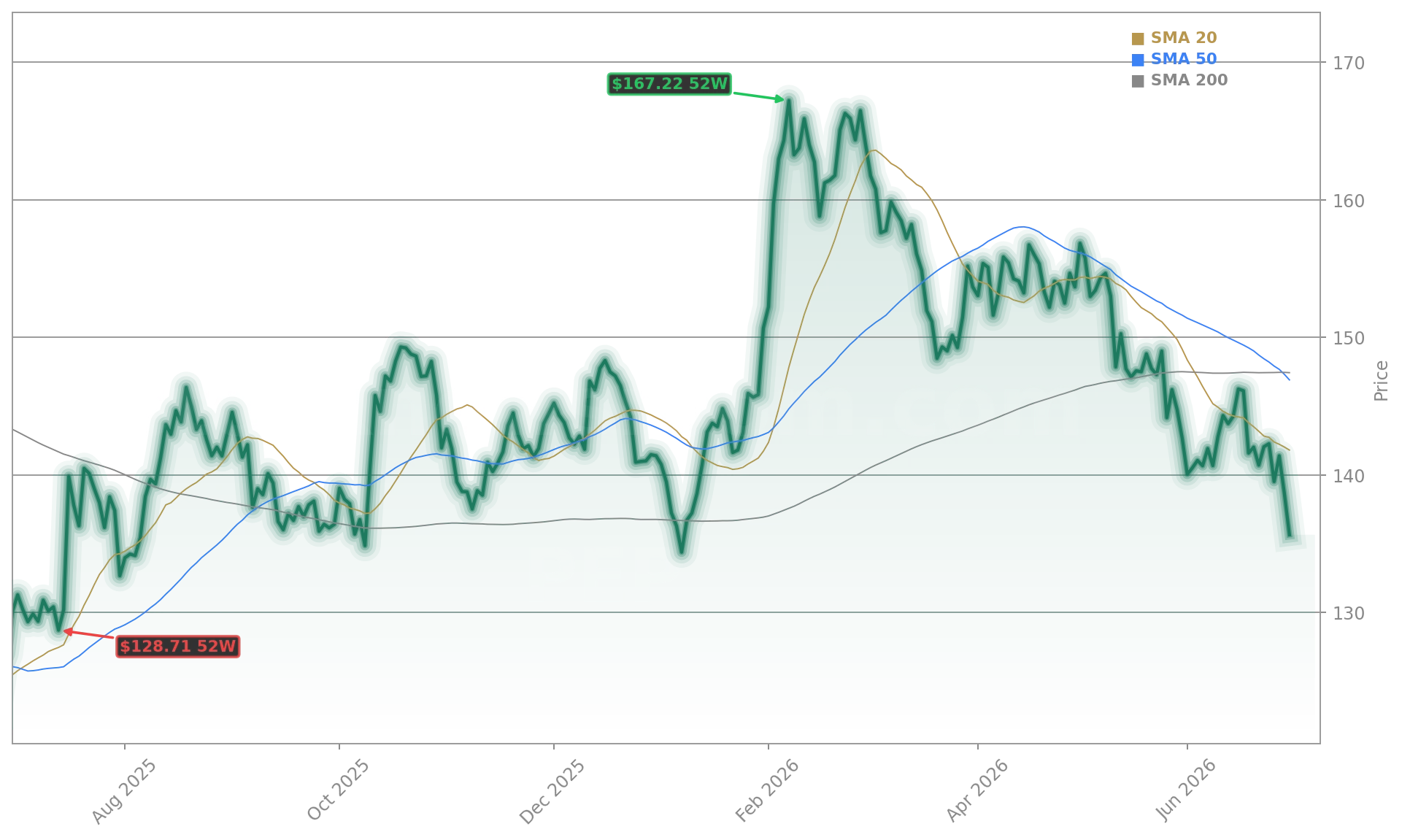

Despite the strong Q1 beat, analyst sentiment remains mixed: the consensus rating is ‘Hold’, with an average price target of $166.85 — just below 24/7 Wall St.’s $168.86. TIKR.com attributes this to a ‘holds-heavy’ distribution and Wall Street’s underappreciation of Q1’s structural cost inflection. Matrix Asset Advisors Inc. NY recently increased its stake by 17.9%, making PepsiCo its 8th largest position — a signal that institutional conviction is building. With shares trading 19% below their $168.19 52-week high, the valuation gap reflects skepticism, not weakness — setting up a compelling opportunity for long-term investors seeking yield, stability, and upside.