Has Take-Two finally removed the biggest risk hanging over GTA 6, or is the real test only beginning now?

Why does the Take-Two GTA 6 Launch matter now?

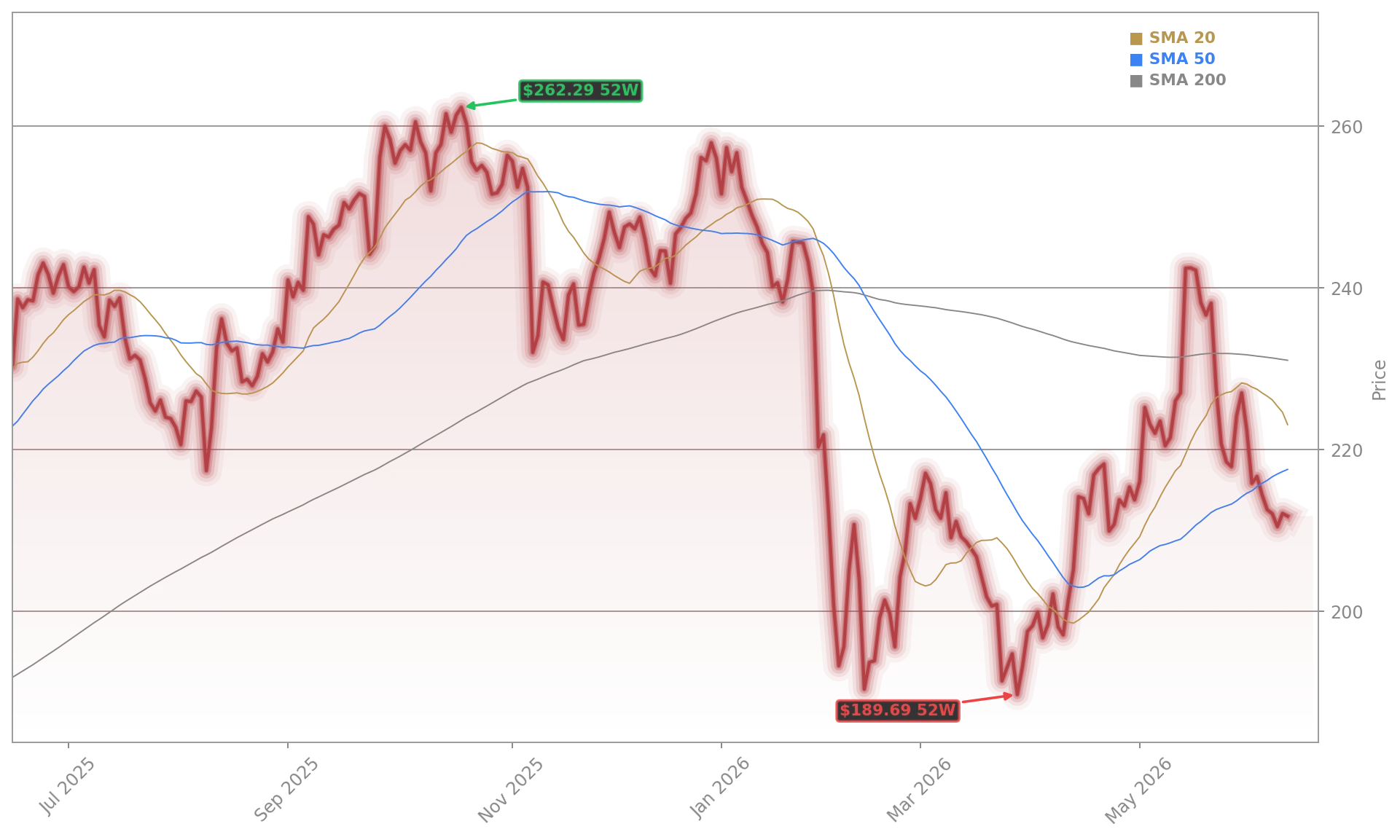

Take-Two Interactive Software, Inc. gave investors the one data point they wanted most: a firm release date for GTA 6. The company said the title will launch on November 19, easing fears of another delay after years of development and repeated schedule questions. That was enough to send TTWO to $250.63 in pre-market trading, up 5.27%, after a prior close of $254.00 and a last quoted price of $238.08.

The reaction makes sense. GTA is one of the most successful entertainment franchises ever created, and GTA V has already sold roughly 225 million copies across platforms. Analysts now expect the sequel to become one of the decade’s biggest media launches, with Oppenheimer’s Martin Yang modeling 40 million unit sales at launch and a meaningful earnings contribution in fiscal 2027.

How strong were Take-Two’s latest numbers?

Quarterly performance was solid even before the release-date catalyst. Revenue came in at about $1.58 billion to $1.68 billion, depending on the reporting framework cited, and exceeded expectations. GAAP net loss narrowed to $59.5 million, or -$0.32 per share, a better outcome than many investors had feared. For fiscal 2026, Take-Two posted $6.66 billion in revenue, showing that its broader portfolio is still working while the company prepares for its biggest launch in years.

Management highlighted continued engagement from GTA Online and Red Dead Redemption, while sports and catalog titles also helped. Mobile is becoming especially important, accounting for 52% of net bookings in the quarter. That mix gives Take-Two more diversification than a pure console-cycle story and matters for investors comparing the company with wider interactive entertainment and platform names like Apple and NVIDIA.

Can Take-Two sustain momentum after GTA 6?

The company’s fiscal 2027 outlook points to a major step-up. Management guided for revenue of roughly $7.9 billion to $8.1 billion, with EBITDA around $1.035 billion at the midpoint and net income of $105 million to $141 million. Some on Wall Street wanted even more, but the market clearly focused on the combination of confirmed timing and a sharply larger revenue base.

That is why the Take-Two GTA 6 Launch narrative now dominates the stock. TradingView data show the 12-month analyst price target rising to $284.24, implying notable upside from recent levels. BMO Capital kept its Buy rating with a $280 target, while broader analyst sentiment remains firmly constructive. At the same time, investors should remember TTWO is still below its prior peak near $265, so this is not yet a new high.

The bigger question is how long the monetization curve lasts. If GTA 6 builds a major online ecosystem like its predecessor, recurring spending could extend the earnings tail for years and create read-throughs for partners across gaming hardware and retail, including Tesla-style high-expectation growth comparisons, Apple platform economics, and chip suppliers such as NVIDIA.

What should investors watch next at Take-Two?

Near term, investors will watch whether management maintains its launch window without disruption and how marketing ramps over the summer. They will also track first-quarter revenue guidance of $1.45 billion to $1.50 billion, plus whether preorders and platform partnerships begin to shape expectations further. The Take-Two GTA 6 Launch thesis now rests less on hope and more on execution.

Related Coverage: Earlier this month, stocknewsroom.com looked at whether the rally was already pricing in a gaming super-cycle. That piece, Take-Two GTA 6 Launch Sends TTWO on +6.8% Record Rally, examined how a confirmed timeline could shift sentiment from speculation toward earnings leverage and broader portfolio relevance for growth investors.

The bottom line is straightforward: the Take-Two GTA 6 Launch has turned a delay-risk story into an execution story. With pre-market buyers returning, stronger guidance on the table, and Wall Street targets from firms including Oppenheimer and BMO Capital staying supportive, TTWO looks positioned for another active stretch as November approaches.