Can Accenture Earnings still justify investor confidence after a sharp sell-off and a weaker revenue outlook?

Did Accenture Earnings Beat or Miss?

Accenture Earnings for Q3 fiscal 2026 showed resilience on profitability but vulnerability on growth momentum. The company reported $3.80 in adjusted EPS — beating the $3.69 consensus — yet revenue landed at $18.72 billion, just shy of the $18.75 billion estimate. That $30 million shortfall, combined with a 2% year-over-year dip in new bookings to $19.32 billion, triggered immediate skepticism. While operating margin expanded 20 basis points to 17.0%, investors focused on the deceleration: consulting revenue grew only 1% in local currency, and the company cited ‘cautious corporate IT spending’ despite strong AI demand — a red flag for the broader tech services ecosystem.

Why Did Accenture Cut Its Revenue Outlook?

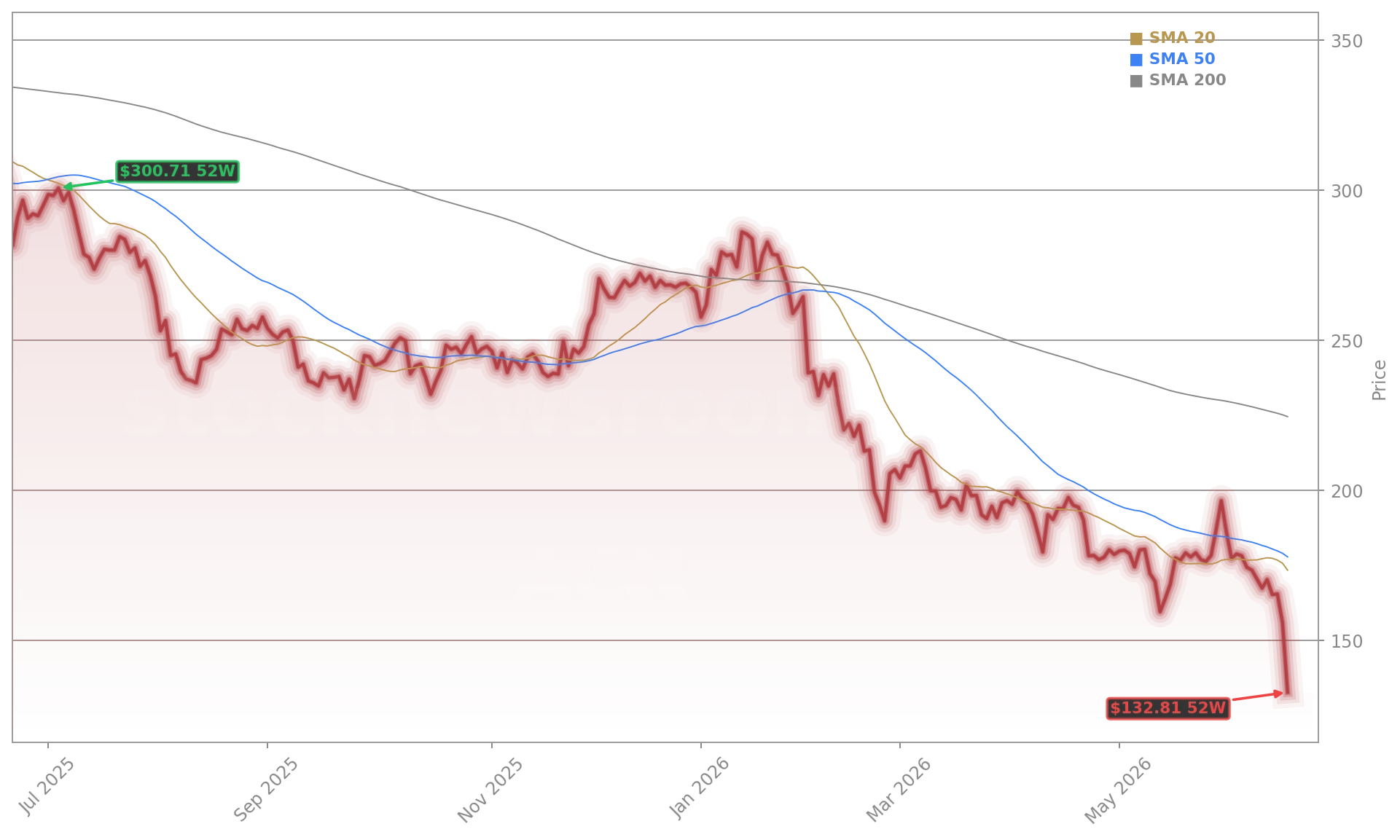

Accenture slashed its FY26 revenue growth forecast to 3–4% in local currency — down from 4–6% — and narrowed its full-year revenue range to $71.76 billion–$72.46 billion, well below the $74.01 billion analyst consensus. The revision reflects mounting headwinds: higher-for-longer interest rates squeezing client budgets, softness in its U.S. federal business (a 1% drag), and slower-than-expected adoption of transformational engagements. Morgan Stanley recently downgraded Accenture PLC, arguing ‘AI enthusiasm hasn’t yet translated into meaningful consulting spend’, a sentiment echoed in Thursday’s price action. The stock’s 52% year-to-date decline — now at a 52-week low — underscores how severely Wall Street has repriced growth expectations for large-cap IT services firms.

What Does the $4.2B Cybersecurity Push Signal?

Accenture PLC announced a $4.175 billion acquisition spree — taking majority control of Dragos and full ownership of runZero and NetRise — to dominate operational technology (OT) and software supply chain security. Collectively, these firms generate $208 million in annual recurring revenue (53% YoY growth), positioning Accenture to capture demand from utilities, manufacturing, and critical infrastructure. But investors reacted skeptically: the timing raised concerns about strategic overreach amid slowing organic growth. While Citigroup affirmed its ‘Neutral’ rating, it trimmed its price target to $142 from $148, citing ‘valuation compression and execution risk in the integration phase’. RBC Capital Markets, meanwhile, maintained its ‘Outperform’ rating but emphasized that ‘the acquisitions must deliver cross-sell leverage — not just cost synergies — to justify the premium.’

How Does This Impact the S&P 500 and Tech Portfolios?

As a top-30 S&P 500 constituent and the largest pure-play IT services firm, Accenture PLC’s stumble carries outsized weight. Its 17% intraday drop dragged down peers: Cognizant (CTSH) fell 3.1%, while Infosys (INFY) slid 2.4%. The episode highlights a broader inflection: AI-driven hype is no longer enough to sustain premium valuations without measurable revenue acceleration. For U.S. investors holding diversified tech portfolios, this reinforces the need to scrutinize exposure to ‘AI beneficiaries’ with weak near-term execution — especially when names like NVIDIA trade at 35x forward P/E while Accenture PLC trades at just 16x. With the NASDAQ down 1.3% on Thursday and rate-sensitive tech stocks broadly under pressure, Accenture’s earnings serve as a cautionary data point for Q2 earnings season.

What’s Next for Accenture Earnings and Shareholder Returns?

AI enthusiasm hasn’t yet translated into meaningful consulting spend.— Morgan Stanley

Despite the guidance cut, Accenture PLC boosted its FY26 adjusted EPS outlook to $13.78–$13.90 and raised its capital return commitment to at least $9.5 billion — up from $9.3 billion — including a 10% dividend hike to $1.63 per share. Free cash flow remained robust at $3.6 billion for the quarter, and the company ended with $10.2 billion in liquidity. With $3.2 billion still available under its share repurchase program, buyback execution could provide near-term support. However, the key inflection will come in Q4: management expects revenue of $17.75–$18.40 billion, still below the $18.47 billion consensus. If Q4 bookings rebound — especially in AI and cloud transformation — the narrative could shift quickly. Until then, investor focus remains razor-sharp on execution, not ambition.