Can ASML’s AI monopoly keep powering the chip boom as Wall Street starts valuing lithography like critical infrastructure?

How Does ASML AI Strategy Fuel S&P 500 Tech Exposure?

ASML Holding N.V. doesn’t design chips — it builds the only machines capable of printing them at 2nm and below. That monopoly in Extreme Ultraviolet (EUV) lithography makes ASML the silent backbone of the AI boom. While investors chase headlines from NVIDIA or Tesla, ASML quietly captures value across the entire stack: TSMC’s Arizona fab, Intel’s 18A-P rollout, and Samsung’s Texas expansion all depend on ASML’s systems. Its Q1 2026 results showed €7.2 billion in net sales (+24% YoY) and €2.8 billion in net income, with gross margin holding at 54.3% — a testament to pricing power and structural scarcity. The company shipped 14 EUV systems in Q1, up from 11 a year ago, and booked €9.1 billion in new orders, including multiple High-NA tools destined for AI-optimized fabs.

What Do Analysts Say About ASML’s AI Moat?

RBC Capital Markets recently upgraded ASML to ‘Outperform’ with a $1,850 price target, citing ‘unmatched leverage to AI-driven capex cycles and accelerating High-NA adoption.’ Citigroup raised its 12-month target to $1,790, emphasizing that ‘no competitor has a credible path to challenge ASML’s EUV leadership before 2030.’ ODDO BHF lifted its target from €1,600 to €2,000 — the highest among European peers — while maintaining a ‘Buy’ rating. These moves reflect a broader shift: ASML is no longer priced solely on semiconductor cyclicality but as a quasi-infrastructure play akin to cloud data center builders. Its forward P/E of 51x may seem stretched versus its 15-year average of 34x, yet it trades at a 7x discount to SpaceX’s implied valuation — a comparison increasingly cited by institutional buyers seeking exposure to AI hardware scalability.

Why Is the SpaceX IPO a Tailwind for ASML?

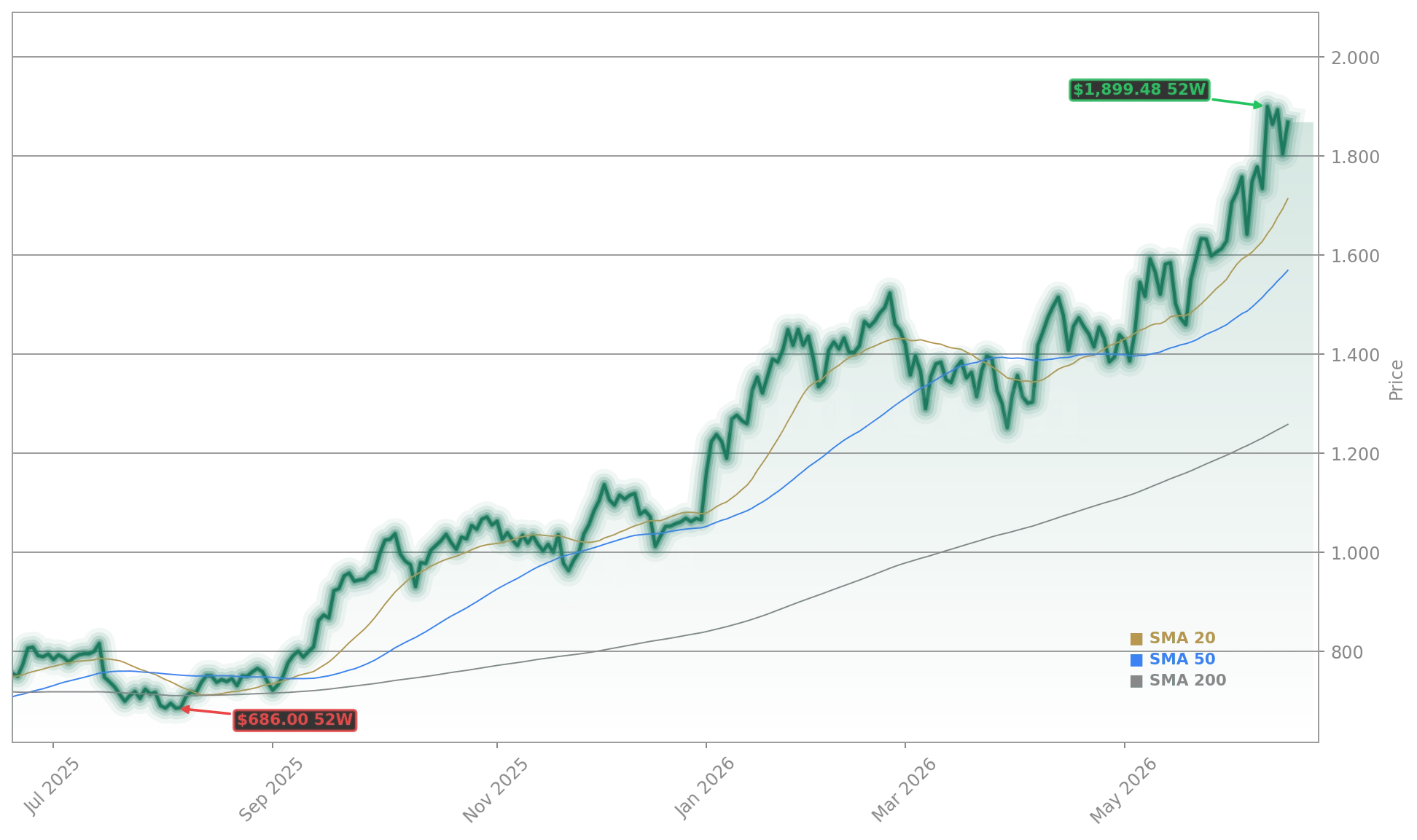

The pending SpaceX IPO isn’t just about rockets — it’s about AI compute. Lynx Capital analysts note that SpaceX’s Starlink Gen3 and Starshield AI initiatives will require massive inference chip deployments, driving demand for custom silicon from partners like Intel and TSMC. Those foundries, in turn, must invest in next-gen lithography — meaning more ASML orders. ASML’s ASML AI Strategy directly benefits from this chain: every $1 billion SpaceX spends on AI infrastructure could trigger $120–$150 million in ASML system purchases over 18–24 months. That linkage helped lift ASML shares +6.1% through 11:25 a.m. ET on Wednesday — outpacing the NASDAQ’s +1.8% gain and widening its YTD lead to +42%.

How Does ASML Compare to Broader Tech and AI Stocks?

Unlike Adobe — whose AI strategy recently triggered a 5% stock plunge amid enterprise adoption doubts — ASML’s ASML AI Strategy delivers tangible, contracted revenue growth. While Adobe (ADBE) struggles to convert AI features into recurring ARR, ASML ships multi-year, multi-hundred-million-dollar systems backed by firm customer commitments. Its top five customers — TSMC, Samsung, Intel, SK Hynix, and Micron — collectively account for 87% of its bookings. That concentration is a risk, yet also a moat: switching costs are near-zero for customers, but near-infinite for competitors. Against the S&P 500’s 12% YTD return, ASML’s performance underscores how AI infrastructure plays now drive index-level tech leadership — not just software narratives.

What’s Next for ASML’s ASML AI Strategy?

ASML’s next inflection point arrives with High-NA EUV volume shipments in late 2026. These tools enable sub-1nm patterning and are essential for chips powering frontier AI models. Brown Advisory Global Leaders Strategy highlighted in its Q1 2026 letter that ‘ASML’s monopoly position in High-NA remains unchallenged, with no viable alternative expected before 2032.’ Meanwhile, U.S. CHIPS Act funding is accelerating domestic lithography investments — further validating ASML’s ASML AI Strategy as both global and geopolitically aligned. With $42.3 billion in backlog and 95% of 2026 revenue already secured, the question isn’t whether demand slows — it’s how fast ASML can scale output to meet it.

ASML’s monopoly position in High-NA remains unchallenged, with no viable alternative expected before 2032.— Brown Advisory Global Leaders Strategy, Q1 2026 Investor Letter

Related Coverage: For deeper analysis on how ASML Terafab could widen ASML’s competitive edge amid AI chip shortages, read ASML Terafab +5.9% as Wall Street Reprices AI Chip Supply. Meanwhile, contrasting execution risks in AI strategies are evident in Adobe AI Strategy: Stock Drops 5% as AI Push Faces Doubts, underscoring why hardware enablers like ASML offer more predictable leverage to the AI wave.