Can ASML Terafab turn ASML’s EUV dominance into an even wider moat as AI chip demand accelerates?

What does ASML Terafab mean for NASDAQ tech?

ASML Terafab isn’t just another fab announcement — it’s the first fully private, U.S.-based, AI-dedicated semiconductor megaproject with binding technology dependencies on ASML’s EUV lithography. Unlike legacy foundries, Terafab’s architecture assumes EUV as non-negotiable infrastructure, locking in multi-billion-dollar system orders. This directly benefits ASML’s revenue trajectory, already turbocharged by Q1 2026 results: €8.8 billion ($10.3B) in revenue, €7.15 EPS ($8.37), and gross margin at 53.0% — the high end of guidance. The $36B–$40B full-year 2026 net sales outlook now incorporates Terafab-related order acceleration, per CEO Christophe Fouquet’s confirmation of ‘ongoing conversations’ with the consortium.

How does ASML Terafab change the competitive landscape?

While xLight — the CHIPS Act–backed startup targeting free-electron EUV alternatives — remains in lab-stage development with first silicon not expected before 2028, ASML Terafab cements the near-term monopoly. ASML demonstrated a 1,000-watt EUV source and lifted the NXE:3800F throughput to 260 wafers/hour, cutting process steps from 100 to 10. That widening technical gap has Wall Street doubling down: Goldman Sachs maintains its ‘Buy’ rating and raised its 12-month price target to $1,915, while Bank of America projects ASML’s 2030 revenue at €73 billion — fueled by AI fab buildouts like Terafab. RBC Capital Markets upgraded ASML to ‘Outperform’, citing ‘unmatched execution in High-NA deployment’ and ‘structural under-supply of EUV capacity through 2027’.

Is ASML’s valuation justified amid ASML Terafab momentum?

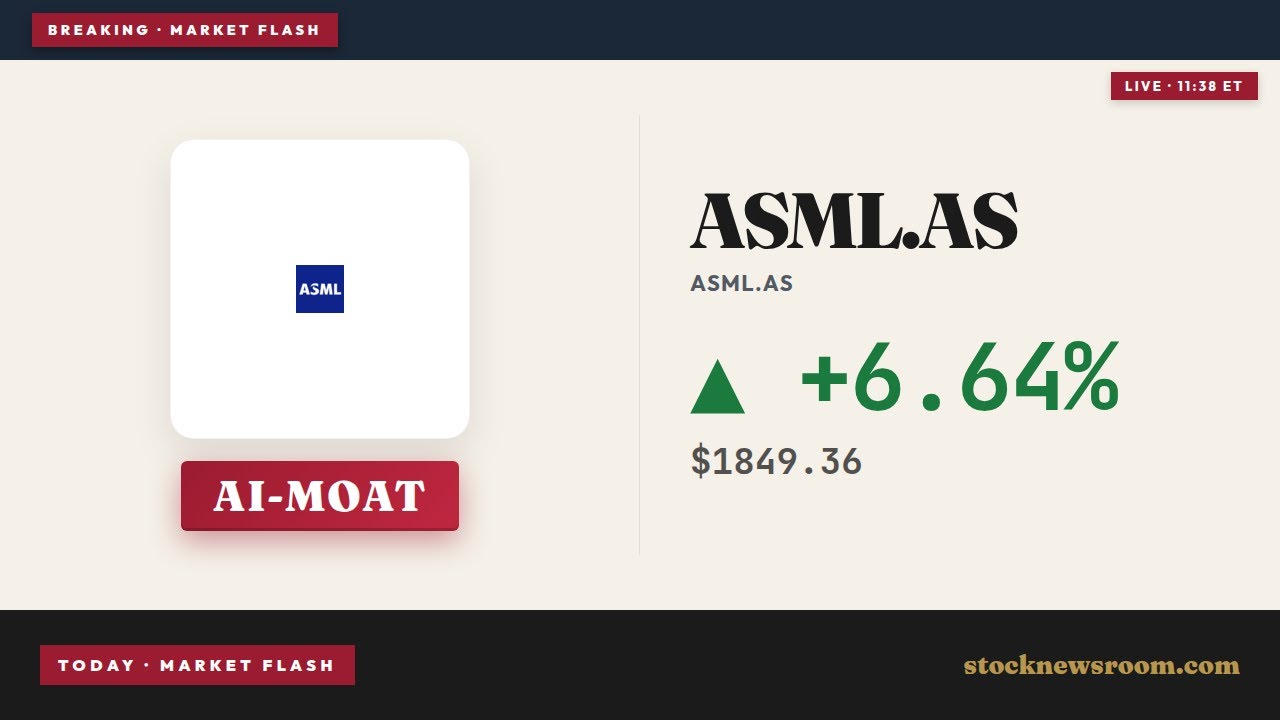

At $1,836.83 in pre-market trading on June 12 — down 3.30% from its $1,899.48 close but still up 5.92% from the prior day’s $1,734.19 close — ASML trades at a forward P/E of 48 and a trailing P/E of 60. That’s rich, yes — but not irrational given its order backlog of €38.80 billion ($45.06B), Q4 2025 net orders of €13.16 billion ($15.28B), and a newly announced €12 billion buyback through 2028. Citigroup notes the valuation ‘discounts a 30% compound annual growth rate in EUV system shipments through 2029’, a pace now validated by Terafab’s $55B initial capex and Intel’s confirmed licensing of its 14A process for the site. Crucially, ASML’s China exposure — expected to decline ‘significantly’ in 2026 — is now more than offset by U.S. and EU onshoring tailwinds.

Which U.S. chipmakers gain most from ASML Terafab?

Intel’s participation as a foundry and process licensor for Terafab positions it as the primary U.S. beneficiary — a direct counterweight to NVIDIA’s AI chip dominance and Tesla’s vertical integration ambitions. Meanwhile, Apple’s upcoming AI silicon roadmap hinges on advanced packaging and 2nm logic — both requiring ASML’s tools and now potentially accelerated by Terafab’s ecosystem. Hanmi Semiconductor’s $32.9 million investment in SpaceX — securing a 7.24% equity stake and a role in chip packaging for Terafab — signals how deeply the supply chain is reorganizing around ASML’s technology stack. The Philadelphia Semiconductor Index’s 7.9% surge on June 11 reflects broad-based confidence: from equipment makers to foundry partners, ASML Terafab has become the anchor for AI hardware capex.

What’s next for ASML Terafab and Wall Street?

With the SpaceX IPO (SPCX) scheduled for June 12 on the NASDAQ at a $1.77 trillion valuation, Terafab transitions from concept to capital-markets reality. ASML’s next catalyst is its Q2 2026 earnings preview in mid-July, where management is expected to confirm firm Terafab system orders and update on High-NA ramp timelines. Analysts at Morgan Stanley highlight ‘early-stage discussions with three additional U.S. hyperscalers’ about EUV-enabled AI chip co-development — a direct spillover from the Terafab blueprint. For U.S. investors, ASML Terafab is no longer about potential — it’s about pipeline, pricing, and portfolio positioning in the AI infrastructure wave.

The semiconductor industry’s growth outlook continues to solidify, driven by ongoing AI-related infrastructure investments. Demand for chips is outpacing supply.— Christophe Fouquet, CEO of ASML

Related Coverage: Can ASML Terafab turn today’s AI chip excitement into a lasting earnings boom, or is Wall Street already pricing in perfection? ASML Terafab +6%: EUV Demand Surge Lifts AI Chip Outlook.