Can Best Buy’s latest quarter finally prove that electronics demand is stronger than Wall Street feared?

Why are Best Buy Earnings moving shares?

Best Buy Earnings landed well ahead of cautious expectations. The company reported first-quarter revenue of $8.94 billion, topping consensus estimates near $8.8 billion, while adjusted earnings per share came in at $1.28. On a GAAP basis, diluted EPS rose 38% to $1.31. Comparable sales increased 2.0%, a key metric for a retailer that had been under pressure from soft discretionary demand and uneven replacement cycles.

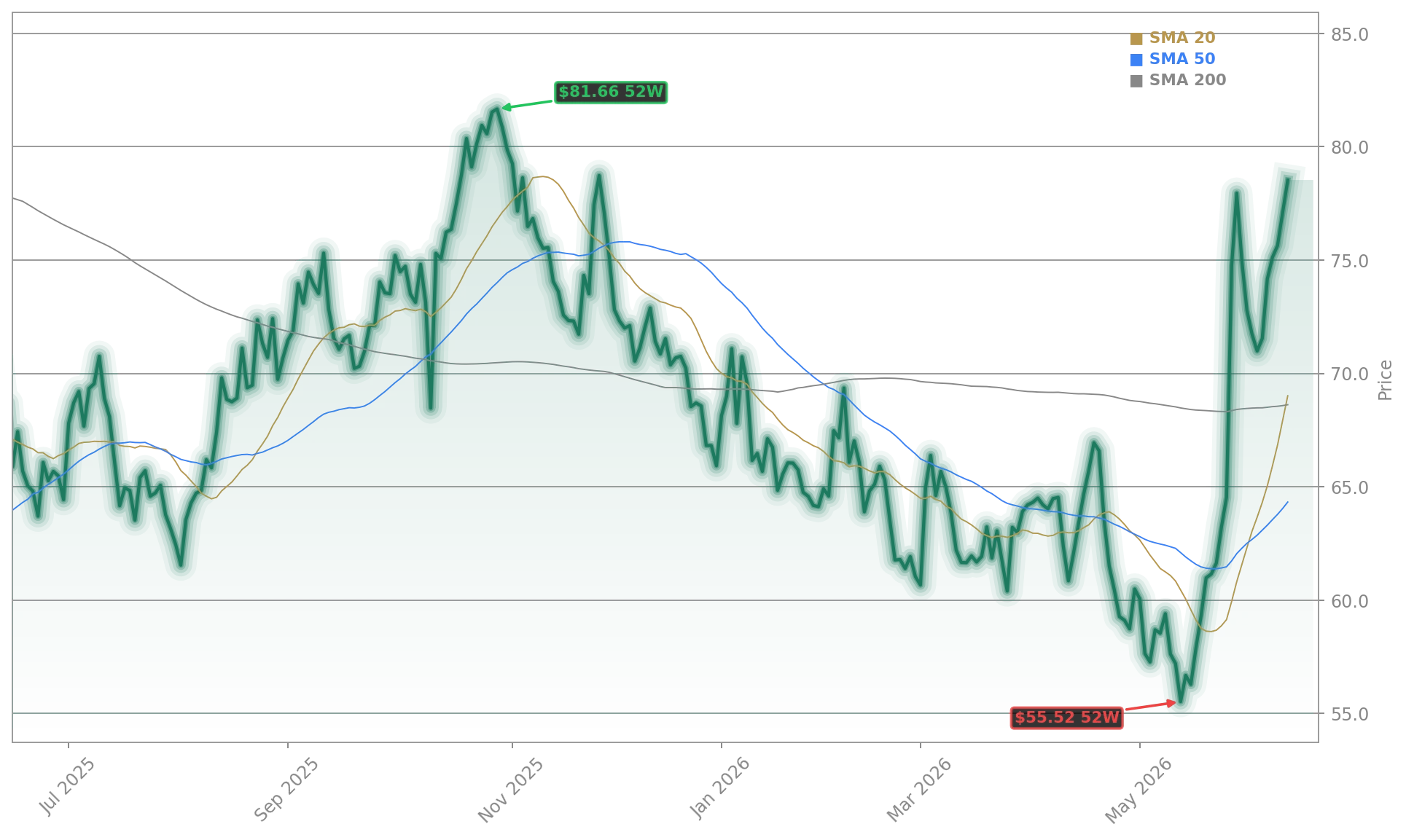

The market reaction has been decisive. BBY jumped to $76.72 versus a previous close of $65.31, an intraday gain of 18.87%. That move reflects not just an earnings beat, but relief that consumer electronics demand is holding up better than feared. Management also lifted the quarterly dividend to $0.96 per share, reinforcing confidence in cash flow and capital returns.

Importantly, the stock is rallying even though it remains below the levels implied by prior 52-week highs cited by market commentators. For investors, this is a sharp repricing of sentiment rather than a breakout to a new high.

What did Best Buy say about demand?

The strongest categories were gaming, computing, and mobile phones, while appliances stayed weaker. That mix matters because it suggests consumers are still willing to spend when products offer visible utility, upgrade value, or ecosystem benefits. AI-enabled devices are part of that story, especially as shoppers compare new hardware tied to services and software from companies like Apple and NVIDIA.

Executives also pointed to broad-based sales improvement and a solid start to May, though some investors remain cautious about tougher comparisons later in the year. There is also attention on product-cycle catalysts, including major console launches and higher interest in connected devices. The company has been leaning into categories such as Xbox, PlayStation 5, wearables, and new AI-oriented hardware, where shopper engagement appears healthier than in traditional big-ticket lines.

That backdrop helps explain why Best Buy Earnings resonated beyond one quarter. Investors were looking for evidence that the U.S. consumer is not simply trading down, but selectively spending where innovation still matters.

How important is the outlook from Best Buy?

Guidance may have been just as important as the quarter itself. Best Buy reiterated its fiscal 2027 outlook for revenue of $41.2 billion to $42.1 billion and adjusted diluted EPS of $6.30 to $6.60. In the current retail environment, maintaining full-year targets after a strong quarter is a meaningful signal that management sees momentum continuing, even if month-to-month volatility remains likely.

There was also a leadership update. CEO Corie Barry plans to step down later this year, and Jason Bonfig is set to take over on November 1, 2026. The transition had previously weighed on sentiment, but the latest report shifts attention back to execution. For now, investors appear more focused on improving margins, better comp trends, and evidence that replacement demand is returning.

Analyst sentiment had been fairly restrained heading into the print. MarketBeat data showed Wall Street’s consensus rating around Hold, with an average price target near $70.25. That makes today’s move notable: shares are now trading above that level, suggesting analysts at firms such as Citigroup, RBC Capital, Goldman Sachs, and Morgan Stanley may need to revisit assumptions if demand trends hold.

Related Coverage: Investors following the management transition may also want to revisit StockNewsroom’s earlier report on Best Buy’s CEO change and the stock plunge. That piece examined whether Jason Bonfig could help reset sentiment as AI-linked hardware demand started to build. Today’s numbers suggest the operating story may be improving faster than the market expected, especially as Best Buy competes across ecosystems influenced by Apple, Tesla, and NVIDIA.

Best Buy Earnings delivered exactly what bullish investors needed: a clear beat, positive comparable sales, firmer margins, and an unchanged outlook. For Wall Street, the report suggests the consumer electronics cycle may be stabilizing sooner than expected. If May demand trends and higher-value upgrade activity continue, Best Buy Earnings could mark the start of a broader rerating in BBY shares.

Fazit folgt.